Real Estate Tax Implications

1. Principal Residence Exemption (PRE)

Global Scope: The PRE is not limited to Canadian real estate. It can apply to a vacation home in Mexico or a condo in Florida, provided the taxpayer is a Canadian resident for tax purposes and "ordinarily inhabits" it at some point during the year.

Key takeaways

The Principal Residence Exemption (PRE) generally covers the housing unit plus 0.5 hectares (about 1.24 acres) of land — excess land is exempt only if proven necessary for the use and enjoyment of the home.

Claiming Capital Cost Allowance (CCA) on a rental property is a one-way door: it permanently disqualifies the property from the PRE and blocks both 45(2) and 45(3) change-in-use elections.

The federal 12-month anti-flipping rule (section 12 ITA) deems profits on residential property held under 365 days as fully taxable business income, not capital gain — and disqualifies the PRE entirely on those properties.

BC's Speculation and Vacancy Tax, the federal Underused Housing Tax (UHT), and short-term rental GST self-supply rules under section 191 of the Excise Tax Act all operate independently — a property can trigger all three in the same year.

Lot Size Limits (The 0.5 Hectare Rule): The PRE generally only applies to the housing unit and up to 0.5 hectares (approx. 1.24 acres) of land.

Excess Land: If the lot is larger than 0.5 hectares, the excess is only exempt if the taxpayer can prove the additional land was necessary for the use and enjoyment of the home.

Pro-Rating: If the excess land is not "necessary," the gain must be pro-rated and taxed as a capital gain.

The "+1 Rule": The formula for calculating the exempt portion of a capital gain is:

Exempt Gain = (1 + Years Designated as Principal Residence) / Years Owned × Total Capital Gain

The additional “+1” year is intended to allow a tax-free transition between properties in the year of a move. It ensures that a taxpayer who sells one home and buys another in the same year does not lose one year of exemption simply because they owned two properties during that calendar year. The +1 is generally only available if the taxpayer was resident in Canada during the years designated.

Allocation Strategy: Designation happens upon sale. Owners of multiple properties should "cherry-pick" years for the property with the highest average annual gain.

The CCA "Deal-Breaker": Claiming CCA disqualifies it from the PRE and prevents the use of 45(2)/45(3) elections.

Change in Use Elections (Sec. 45-2 & 45-3)

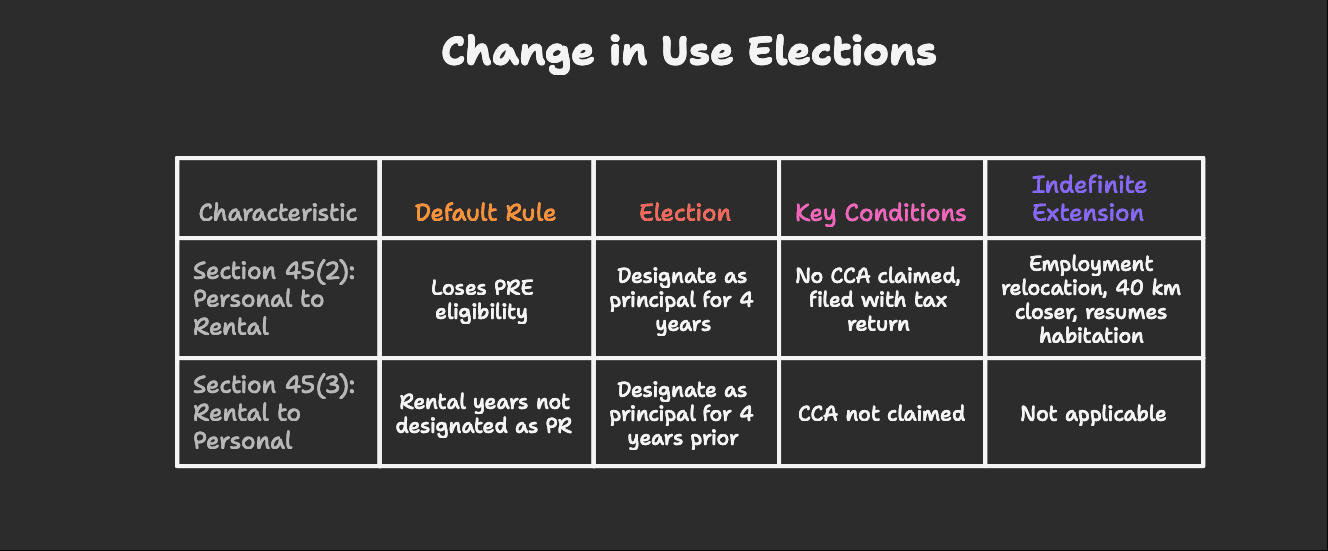

Section 45(2): Personal to Rental

Default Rule (Without Election): When a principal residence is converted to a rental property, it loses its PRE eligibility. When property is eventually sold, rental years cannot be allocated as principle residence.

Election Under 45(2): This election allows the taxpayer to designate property as a principle for 4 additional years while it is being rented, given no other property is designated as principal residence.

• Key Conditions:

· No CCA can be claimed on the property during the rental period.

· The election must be filed with the tax return in the tax year that the change occurs (late filing relief may be available in limited cases).

Example – Standard 4-Year Rule: Alex buys a home in 2018 and lives in it until 2024. In 2024, he moves and begins renting it. If he sells in 2027, he may designate the property as his principal residence from 2018–2027 (up to 4 rental years), preserving the PRE.

The Indefinite Extension (Employment Relocation): Under Section 54.1, the 4-year limit may be waived if:

· The move is required for employment,

· The new residence is at least 40 km closer to the new workplace, and

· The taxpayer eventually resumes ordinary habitation of the property.

Example – Employment Move: Sarah moves from Victoria to Calgary for work (over 40 km). She rents out her Victoria home for 7 years. If she moves back in later, she may still designate those rental years as principal residence years under the extended rule.

Section 45(3): Rental to Personal

Default Rule (Without Election): When a rental property is converted to personal use, rental years may not be designated as principal residence when reporting the eventual sale of the property.

Election Under 45(3): The taxpayer may elect to designate the property as a principal residence for up to 4 years prior to moving in.

Key Limitation: The election is not available if CCA was ever claimed on the property.

Example – Rental to PR: Maria purchases a rental property in 2016. By 2026, it has appreciated significantly. She moves into the property in 2026. With the election, she may designate up to 4 prior rental years as principal residence years (subject to overall PRE planning).

Planning Insight: Claiming CCA can permanently eliminate access to 45(2) and 45(3). Tax deferral from depreciation must be weighed against long-term PRE flexibility.

2. Capital Cost Allowance (CCA)

Capital Cost Allowance (CCA) is the tax mechanism that allows taxpayers to deduct depreciation on income-producing property over time. It is not mandatory in Canada, but it significantly affects both annual taxable income and the ultimate capital gain calculation on sale.

How CCA Works

Tax Deferral Mechanism: CCA reduces net rental income by allowing a deduction for depreciation. This lowers current-year tax but does not eliminate tax permanently.

Building vs. Land: Only the building component is depreciable. Land is not eligible for CCA.

Class 1 (Standard Rental Property): Generally, 4% declining balance rate.

Recapture Risk: When the property is sold, any CCA previously claimed likely to be "recaptured" and taxed as ordinary income to the extent proceeds exceed the undepreciated capital cost (UCC).

Example – Basic Rental Scenario

Jordan purchases a rental property for $800,000 in 2026, allocated as:

· Land: $300,000

· Building: $500,000

If he claims CCA at 4% on the building (subject to the half-year rule in year one), his taxable rental income decreases annually.

If he later sells the property for $900,000 and the building’s UCC has been reduced significantly due to CCA claims, the difference between the sale proceeds (allocated to building) and UCC will be recaptured and taxed at full marginal rates before any capital gain is calculated.

Strategic Considerations

CCA on Buildings Cannot Create or Increase a Rental Loss: CCA on buildings cannot be used to create or increase a rental loss (it is limited to net rental income before CCA).

Impact on Principal Residence Planning: Claiming CCA on a former principal residence permanently restricts access to the 45(2) and 45(3) elections.

New Build Incentive: Budget 2024 introduced an accelerated 10% CCA rate for new purpose-built rental housing (subject to qualifying conditions).

The Cross-Border Nuance (US Persons)

"Allowed or Allowable" Rule (U.S. Tax Law): For U.S. citizens and green card holders, depreciation is considered claimed whether or not it was actually deducted.

Mismatch Risk: If a U.S. person does not claim CCA in Canada but is required to reduce U.S. basis for depreciation, this creates a permanent basis mismatch.

Planning Insight: For U.S. persons resident in Canada, declining to claim CCA may not prevent U.S. depreciation recapture. Cross-border modelling is essential before deciding whether to claim CCA.

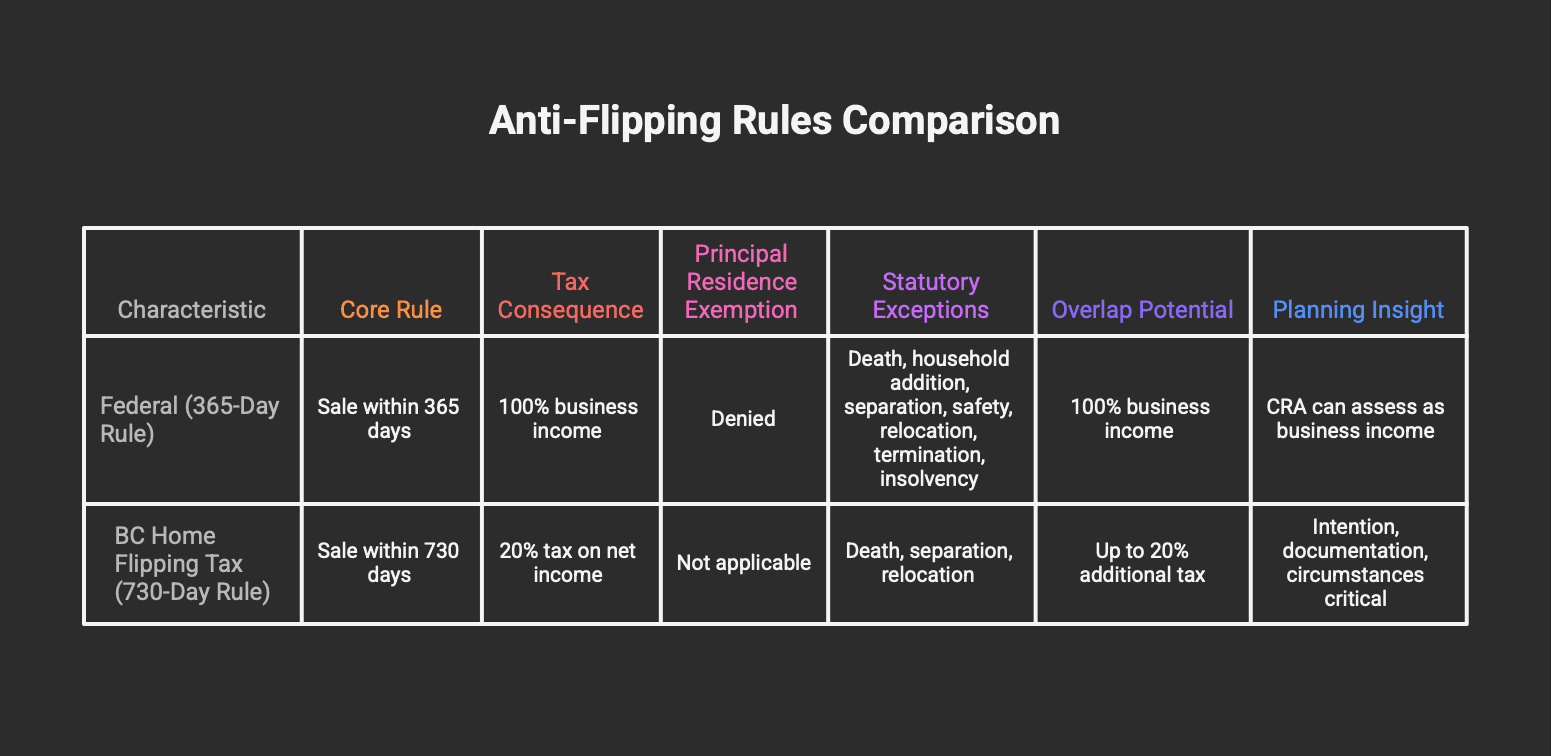

3. Anti-Flipping Rules (The "Double" Layer)

BC now has two overlapping anti-flipping regimes — a federal income tax rule and a separate BC provincial tax. A transaction may be caught by one or both.

Federal (The 365-Day Rule)

Core Rule: If a residential property is sold within 365 days of acquisition, the gain is deemed to be business income — not a capital gain — and the Principal Residence Exemption is denied.

Tax Consequence: 100% of the gain is fully taxable at marginal rates. No 50% capital gains inclusion. No PRE.

Statutory Exceptions (Life Events): The rule does not apply if the sale occurs due to one of the following qualifying events:

· Death: Of the taxpayer or a related person.

· Household Addition: Birth or adoption of a child.

· Separation or Divorce: Breakdown of a marriage or common-law partnership.

· Personal Safety: Threats to personal safety (e.g., domestic violence).

· Employment Relocation: The taxpayer or spouse moves at least 40 km closer to a new place of employment.

· Involuntary Termination: Layoff or loss of employment.

· Insolvency: Bankruptcy or other serious financial distress.

Important: The exceptions must be genuine and documented. CRA may challenge transactions that appear structured to fit within an exception.

Planning Insight: Even if the 365-day rule does not apply, CRA can still assess the gain as business income under traditional intention-based analysis (secondary intention doctrine).

BC Home Flipping Tax (The 730-Day Rule)

Core Rule: Applies to profits from the sale of residential property owned for less than 730 days (2 years).

Rate Structure:

· 20% tax on net taxable income from property sold within the first 365 days.

· The rate gradually tapers between day 366 and day 730.

· After 730 days, the BC flipping tax does not apply.

Separate From Income Tax: This is an additional provincial tax. It can apply even if the federal 365-day rule does not.

Potential Overlap: A property sold within 12 months could face:

· 100% business income treatment federally, and

· Up to 20% additional BC flipping tax provincially.

Exemptions: Similar life-event exemptions exist (e.g., death, separation, relocation), but the BC rules are administered separately and require their own analysis.

Planning Insight: Holding period alone is not sufficient protection. Intention, documentation, and factual circumstances remain critical in defending a transaction.

4. Short-Term vs. Long-Term Conversion (The GST Trap)

The GST treatment of residential property depends entirely on how the property is used. A property that would otherwise qualify as an exempt "used residential complex" can lose that status if it is operated primarily as a short-term rental (STR). The financial exposure can be significant.

4.1 Residential Complex vs. Commercial Use

Under the Excise Tax Act, the sale of a used residential complex is generally exempt from GST. However, property used primarily for short-term accommodation (similar to a hotel or Airbnb operation) is treated as commercial real property.

Long-Term Rental (LTR): Leases exceeding one month are generally exempt supplies. Sale is typically GST-exempt. Short-Term Rental (STR): Stays under one month are taxable supplies. Property may be considered commercial.

4.2 The “Primarily” Test (More Than 50%)

CRA looks at whether the property is used "primarily" (more than 50%) for short-term accommodation. This may be assessed based on:

Time (number of rental days) Space (portion of property used for STR) Revenue or overall commercial use

If more than 50% of the property is used for STR purposes, the entire property may be treated as commercial.

If less than 50%, GST may apply on a pro-rata basis depending on how the property is structured and used.

4.3 Sale of a Short-Term Rental Property

If a property is classified as commercial at the time of sale:

• The sale becomes a taxable supply. • 5% GST applies in BC (or applicable HST in other provinces). • The seller must collect and remit GST unless specific commercial purchaser rules apply.

Example:

A condo operated exclusively as an Airbnb is sold for $900,000. If considered commercial, GST of $45,000 may apply on closing.

This is in addition to income tax on the gain.

4.4 ITCs and Commercial Status

If the owner registers for GST and claims Input Tax Credits (ITCs) on; purchase price, renovations, or operating expenses, this strengthens the characterization of the property as commercial.

Once the property is pulled into the commercial GST stream, exiting that stream can trigger additional tax consequences.

4.5 Change of Use – The Self-Supply Rule

A major trap occurs when a property shifts from taxable STR use to exempt use (long-term rental or personal use).

This triggers a deemed disposition at fair market value for GST purposes — even though no sale occurred.

This is known as the self-supply rule.

Consequences:

The owner is deemed to have sold the property at FMV. 5% GST must be remitted on FMV. This is payable out-of-pocket.

Example:

An STR cabin worth $800,000 is converted to long-term rental. The owner may owe $40,000 in GST at the time of conversion.

No cash is received — but GST is still payable.

4.6 Strategic Planning Considerations

· Consider GST implications before registering for STR operations.

· Model conversion tax before switching from STR to LTR.

· Analyze holding period and planned sale timing.

· Ensure purchase agreements properly address GST responsibility.

· Evaluate whether incorporation or structuring changes risk profile.

This area combines GST law, income tax law, and factual characterization risk — and errors can result in five-p unexpected tax liabilities.

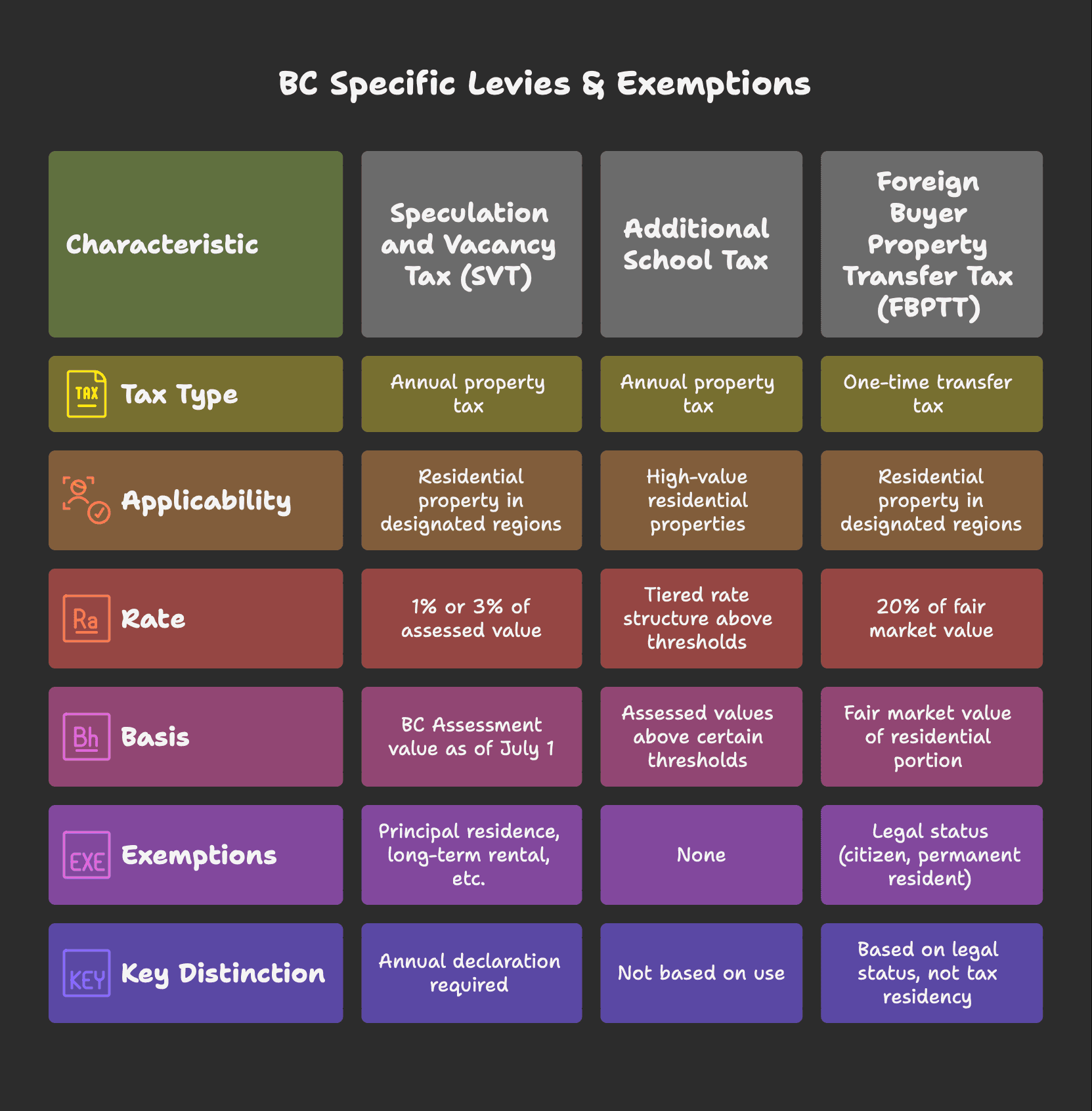

5. BC Specific Levies & Exemptions

British Columbia imposes several property-based taxes that operate independently from federal income tax rules. These taxes can apply even when no income tax is triggered.

5.1 Speculation and Vacancy Tax (SVT)

The Speculation and Vacancy Tax applies annually to residential property located in designated taxable regions of BC (including Metro Vancouver, the Capital Regional District, Kelowna, Nanaimo, etc.).

2026 Rates

• 3% of assessed value – Foreign owners and satellite families. • 1% of assessed value – Canadian citizens and permanent residents who do not meet exemption criteria.

The tax is calculated on BC Assessment value as of July 1 of the prior year.

Core Exemptions

Principal Residence Exemption: If the property is the owner’s principal residence for the year.

Qualifying Long-Term Rental: Rented for at least 6 months of the year in periods of at least 30 consecutive days.

Separation or Divorce: Property cannot be occupied due to marital breakdown.

Medical Exemption: Owner is in long-term care or hospitalized.

Death of Owner: Applies in the year of death and sometimes the following year.

Construction or Major Renovation: Property is undergoing substantial construction or renovation and cannot reasonably be occupied.

Strata Rental Restriction (Transitional): Where legal restrictions limit rental ability (subject to evolving provincial housing reforms).

Failure to file the annual SVT declaration can result in automatic assessment of tax even if an exemption applies.

5.2 Additional School Tax (Luxury Home Tax)

Separate from SVT, BC levies an additional annual school tax on high-value residential properties.

Applies to assessed values above certain thresholds (e.g., over $3 million). Tiered rate structure applies.

This tax is not based on use — it applies regardless of occupancy or rental status.

5.3 Foreign Buyer Property Transfer Tax (FBPTT)

The Foreign Buyer Property Transfer Tax is a one-time transfer tax payable on acquisition of residential property in designated regions.

• Rate: 20% of the fair market value of the residential portion. • Applies in Metro Vancouver, Capital Regional District, Fraser Valley, Kelowna, Nanaimo, and other designated areas.

This is in addition to the regular BC Property Transfer Tax (PTT).

Key Distinction – Legal Status vs. Tax Residency

FBPTT is based on legal immigration status (citizen, permanent resident, foreign national). It is not based on CRA income tax residency.

A person could be a Canadian tax resident but still subject to FBPTT if they are not a citizen or permanent resident at the time of purchase.

Certain foreign nationals who become permanent residents within a specified timeframe may qualify for a refund. Nominee program participants may qualify for exemptions.

Corporate and trust ownership structures require separate analysis; foreign control rules can trigger tax even if a minority foreign interest exists.

5.4 Interaction Risks

A property may be exempt from federal anti-flipping rules but still subject to SVT.

A property used for short-term rental may trigger GST consequences and still be subject to SVT if not qualifying as a long-term rental.

Immigration status changes can affect FBPTT exposure on acquisition but do not retroactively remove tax unless refund conditions are met.

BC property taxation is layered. Each tax must be analyzed independently based on ownership, use, location, and status.

6. International & Cross-Border Considerations

Cross-border real estate ownership introduces an entirely separate layer of compliance, withholding, and reporting obligations. These rules apply whether the property is located in Canada or abroad, and whether the owner is immigrating to or emigrating from Canada.

6.1 Non-Resident Rental Income (Canadian Property Owned by Non-Residents)

When a non-resident owns Canadian rental property, special withholding rules apply.

Default Rule – Section 212 Withholding

• 25% withholding tax on gross rental income. • The Canadian tenant or property manager is required to withhold and remit monthly. • No expense deductions are allowed under the default method.

Section 216 Election – Tax on Net Income

Non-residents may elect under Section 216 to file a Canadian return and be taxed on net rental income instead of gross.

• Requires filing an annual Section 216 return. • Often coordinated with Form NR6 to reduce withholding during the year. • With NR6 approval, withholding is based on estimated net rental income instead of gross.

Failure to file the 216 return on time can eliminate access to the net-income treatment.

6.2 Immigration to Canada (Becoming a Canadian Tax Resident)

When an individual becomes a Canadian tax resident:

Most foreign capital property receives a "step-up" in adjusted cost base to fair market value on the date of arrival. This limits Canadian tax exposure to post-immigration appreciation.

Canadian real estate does not receive a step-up (because it was already taxable Canadian property). U.S. citizens remain taxable in the United States regardless of residency. Foreign reporting forms (e.g., T1135) may become required for non-Canadian property exceeding reporting thresholds.

6.3 Emigration from Canada (Departure Tax)

When an individual ceases Canadian tax residency:

Canada imposes a deemed disposition on most capital property at fair market value ("departure tax").

Canadian real estate is Taxable Canadian Property (TCP) and is generally excluded from departure tax. The property remains subject to Canadian tax upon actual sale. This creates deferral — not elimination — of Canadian tax on real property.

Security or elections may be required if other assets trigger departure tax.

6.4 Non-Resident Sellers – Section 116 Clearance

When a non-resident sells Canadian real estate, strict withholding rules apply.

• Buyer must withhold 25% of the gross purchase price. • Withholding can increase to 50% if the property is inventory or depreciable commercial property.

To reduce withholding:

• Seller must apply for a Certificate of Compliance under Section 116. • Application must be filed within prescribed timelines. • Withholding is reduced to 25% of the estimated capital gain (not gross price) once clearance is issued.

6.5 Treaty and U.S. Interaction Considerations

For U.S. persons:

• Rental income and capital gains remain taxable in the United States. • Foreign tax credits may offset double taxation. • Depreciation differences ("allowed or allowable") can create permanent basis mismatches. • U.S. estate tax exposure may arise for U.S. situs property.

For Canadians owning U.S. real estate:

• FIRPTA withholding may apply on sale. • U.S. federal and state tax returns may be required. • Treaty tie-breaker rules may affect residency determinations.

Cross-border real estate ownership often requires dual filings, currency adjustments, and coordinated modelling.

6.6 Practical Planning Considerations

• Determine residency status before buying or selling property. • Model departure tax exposure prior to leaving Canada. • Coordinate Section 116 filings early in a transaction. • Analyze treaty relief and foreign tax credits. • Consider ownership structures (corporation vs. personal vs. trust) in light of cross-border rules.

International real estate planning is not simply an extension of domestic rules — it is a separate compliance framework layered on top of income tax, GST, and provincial property taxes.

7. TOSI and Attribution Rules (Income Splitting)

The Myth of Arbitrary Allocation

Consistency is Key: Taxpayers cannot arbitrarily decide who "owns" the income each year based on who is in a lower tax bracket. Ownership vs. Taxation: Income must follow legal and beneficial ownership. You cannot switch from 100% Spouse A to 100% Spouse B year-to-year without a legal transfer of the property (which triggers PTT and deemed dispositions).

Income Attribution Rules

The Core Rule: If you gift or loan funds to a spouse or minor child to buy an investment property, the rental income (and often the capital gain) is attributed back to you and taxed at your marginal rate. Exceptions: o Fair Market Value Sales: Property is sold to a spouse at FMV using "clean" funds (not a gift). o Prescribed Rate Loans: Loaning funds to a spouse at the CRA prescribed rate.

Tax on Split Income (TOSI)

Corporate Ownership: If real estate is held within a corporation, dividends paid to "inactive" family members are taxed at the highest marginal rate, regardless of their actual income. Excluded Business: To escape TOSI, the family member must be "actively engaged" in the business on a regular, continuous, and substantial basis (generally 20 hours per week). Age 65 Exception: If the primary business owner is 65+, they can generally split income with a spouse without triggering TOSI.

Capital Gains Advantage

Growth vs. Income: While rental income is subject to strict attribution/TOSI rules, capital gains on the eventual sale of a property are often easier to split if the initial ownership was structured correctly (e.g., through a family trust or legitimate joint ownership from day one).

Conclusion

Real estate is often viewed as a straightforward investment, but the Canadian tax rules surrounding property ownership are anything but simple. Between the Principal Residence Exemption, change-in-use elections, capital cost allowance recapture, federal and provincial anti-flipping rules, GST exposure for short-term rentals, and various BC-specific levies, a single property can fall under multiple overlapping tax regimes.

Add cross-border ownership, immigration or emigration, non-resident rules, or family ownership structures, and the complexity increases significantly. Many of the most costly mistakes occur not when the property is sold, but years earlier — when decisions are made about claiming CCA, converting a property to rental use, structuring ownership between family members, or operating a property as a short-term rental.

In many cases, a small decision made early on can permanently eliminate access to key planning opportunities, such as the Principal Residence Exemption or change-in-use elections. Similarly, misunderstanding GST rules around short-term rentals can create unexpected tax liabilities that are not covered by the sale proceeds of the property.

Real estate tax planning is therefore not just about reporting the sale correctly — it is about structuring ownership, documenting intent, and planning transitions long before a transaction occurs.

How Modern Axis CPA Can Help

At Modern Axis CPA, we work with property owners, investors, and cross-border clients to navigate the increasingly complex tax landscape surrounding real estate. Our focus is not just compliance, but proactive planning that helps prevent costly surprises.

Our real estate tax advisory services include:

• Principal Residence planning and PRE optimization across multiple properties

• Change-in-use elections (45(2) and 45(3)) and rental conversion strategies

• CCA planning and modelling of recapture risk

• Short-term rental tax analysis, including GST exposure and self-supply risks

• Anti-flipping rule analysis for both federal and BC regimes

• BC-specific tax planning, including Speculation and Vacancy Tax considerations

• Cross-border real estate tax planning, including U.S. property ownership, FIRPTA withholding, and foreign tax credit coordination

• Non-resident compliance, including Section 216 filings and Section 116 clearance certificates

• Ownership structuring, including corporate ownership, trusts, and family planning

Real estate transactions often involve large dollar amounts and multiple layers of taxation. Careful planning can significantly reduce tax exposure, preserve exemptions, and avoid compliance issues.

If you own real estate, are considering converting a property to rental use, operating a short-term rental, or dealing with cross-border property ownership, professional advice early in the process can make a substantial difference.

You can learn more about our services or schedule a consultation at Modern Axis CPA.

Frequently asked questions

Does the Principal Residence Exemption apply to foreign property?

Yes, the PRE is not limited to Canadian real estate. A vacation home in Mexico or a condo in Florida can qualify, provided the taxpayer is a Canadian resident for tax purposes during the designated years and "ordinarily inhabits" the property at some point in each year designated. The PRE is residency-based, not location-based. Foreign property still has to be reported on Form T1135 if cost exceeds $100,000 CAD, even when it's PRE-eligible.

What is the 0.5 hectare rule for the Principal Residence Exemption?

The PRE generally covers the housing unit plus 0.5 hectares (approximately 1.24 acres) of land. Anything above that is exempt only if the taxpayer can prove the additional land was necessary for the use and enjoyment of the home — typically because of municipal zoning minimums or physical layout (driveway access, septic field). If the excess land is not necessary, the gain on that portion is pro-rated and taxed as a capital gain.

What happens to my PRE when I convert my home to a rental property?

By default, a change in use from personal to rental triggers a deemed disposition at fair market value, which can crystallize a capital gain. Section 45(2) of the Income Tax Act lets the taxpayer elect to defer that deemed disposition and designate the property as a principal residence for up to four additional rental years — but only if no CCA is claimed during the rental period and no other property is designated as the principal residence in those years.

Why is claiming CCA on a rental property risky?

Claiming CCA on a rental property is the single most consequential election in Canadian real estate tax. It disqualifies the property from the Principal Residence Exemption permanently, blocks the use of section 45(2) and 45(3) change-in-use elections, and triggers recapture (taxed as ordinary income) when the property is sold. CCA reduces current-year rental income but transfers a much larger tax bill to disposition — usually a bad trade for owner-occupiers.

Does the new anti-flipping rule apply to all home sales?

The federal anti-flipping rule under section 12 of the Income Tax Act deems profits on residential property held less than 365 days to be fully taxable business income, not a capital gain, and removes the Principal Residence Exemption entirely. Limited life-event exceptions apply — death, divorce, job relocation of more than 40 km, serious illness, household additions, involuntary disposition. BC also runs its own provincial flipping tax with different rules, so cross-jurisdiction analysis is mandatory.

What taxes apply to short-term rentals in BC?

Short-term rentals in BC face the BC Short-Term Rental Accommodations Act (limits most non-principal-residence STRs in qualifying municipalities), the BC Speculation and Vacancy Tax (if not principal residence and not long-term rented), the federal Underused Housing Tax for non-resident or corporate owners, and GST self-supply rules under the Excise Tax Act when a long-term rental converts to short-term — which can deem the property sold at fair market value for GST purposes.

Alex Ataman, CPA

Founder

Modern Axis CPA