TOSI Excluded Shares: 10/10 Rule for Spousal Dividends

If you incorporated your business and put your spouse on the share register so you could split dividends, the question that decides whether the plan still works is whether the shares your spouse holds are excluded shares under the Tax on Split Income (TOSI) rules. Get the structure right and dividends to your spouse are taxed at their marginal rate. Get it wrong and the same dividend lands at the top marginal rate, regardless of what your spouse actually earns.

Key takeaways

TOSI applies the top combined marginal rate to "split income" received by a specified individual from a related business, erasing the tax benefit the split was designed to create.

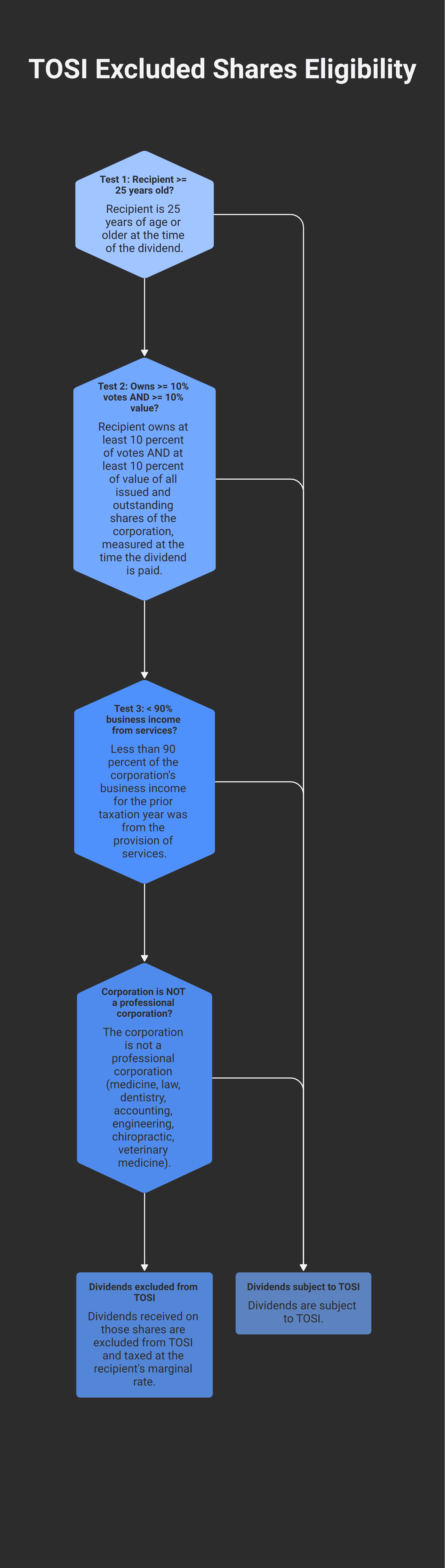

The excluded shares carve-out in subsection 120.4(1) exempts dividends only if three tests all pass: the recipient is 25 or older, owns 10% of votes and 10% of value, and under 90% of corporate income is from services.

Professional corporations (medicine, law, dentistry, accounting) are explicitly carved out of the excluded shares relief, regardless of whether the three tests are otherwise met.

The 10%/10% ownership test is measured at the moment the dividend is paid, not at year-end — shares issued or pruned days around the dividend date can flip eligibility.

The Tax on Split Income rules in section 120.4 of the Income Tax Act sit on top of almost every owner-managed corporation in Canada. They were rewritten in 2018 to extend beyond minor children to any adult family member receiving income from a related business. The "excluded shares" carve-out — the rule almost no one knows by name — is what keeps the most common income-splitting structures legal. This post is about how that carve-out actually works.

The rule, in one sentence

Under subsection 120.4(2), every dollar of "split income" received by a "specified individual" — which after 2018 means essentially any adult family member receiving dividends or interest from a corporation in which a related person works or holds significant influence — is taxed at the highest combined federal and provincial marginal rate, unless the income falls into one of the statutory carve-outs in subsection 120.4(1). The excluded shares carve-out is the most-used of those.

In practical terms: if your spouse, adult child, parent, or sibling holds shares in your corporation and receives dividends, the default assumption is TOSI. The carve-outs are the affirmative defence.

Who is a "specified individual"

A specified individual under section 120.4 is essentially any Canadian-resident family member who is related to a person who either works in the business, owns at least 10% of the corporation's shares, or has significant influence over it. Spouses (including common-law), parents, adult children, siblings, and their spouses are all in scope. The rule reaches outside the nuclear family — uncles, nieces, in-laws — wherever there is a relationship under the Income Tax Act's broad "related persons" definitions.

The expansion in 2018 was the change everyone felt. Before 2018, TOSI applied mainly to minor children. After 2018, the entire adult family is in scope, and the carve-outs become the planning lever.

What "split income" actually catches

Split income includes:

Dividends on shares of a private corporation

Interest from a debt obligation of a private corporation, partnership, or trust

Income from a partnership or trust derived from a related business

Capital gains from disposing of shares of a private corp where the related business test is met (specific anti-avoidance)

Salary and wages are not split income. A spouse paid a salary for actual work in the business sidesteps TOSI entirely — but salary then has to meet the "reasonable" test under section 67, which the CRA scrutinises separately.

The classic income split that TOSI was written for is the dividend sprinkle: an incorporated owner-manager declares dividends on a spouse's shares or adult child's shares, redistributing corporate income across multiple low-tax-bracket family members. The excluded shares carve-out is what determines whether that sprinkle still works after 2018.

The excluded shares carve-out — three tests, all must pass

Read literally from subsection 120.4(1), an "excluded share" is a share of a corporation owned by a specified individual where, at the time:

Age — The individual is 25 years old or older.

10%/10% — The shares owned by the individual represent at least 10% of the votes that could be cast at a meeting of shareholders, AND at least 10% of the fair market value of all issued and outstanding shares of the corporation.

<90% services — Less than 90% of the corporation's business income for the last taxation year was from the provision of services.

And independently of the three tests:

Not a professional corporation — The corporation is not carrying on a professional practice (medicine, law, dentistry, accounting, chiropractic, or veterinary medicine).

<10% of income from a related business — Substantially all (effectively, 90%+) of the corporation's income for the last year is from sources other than another related business.

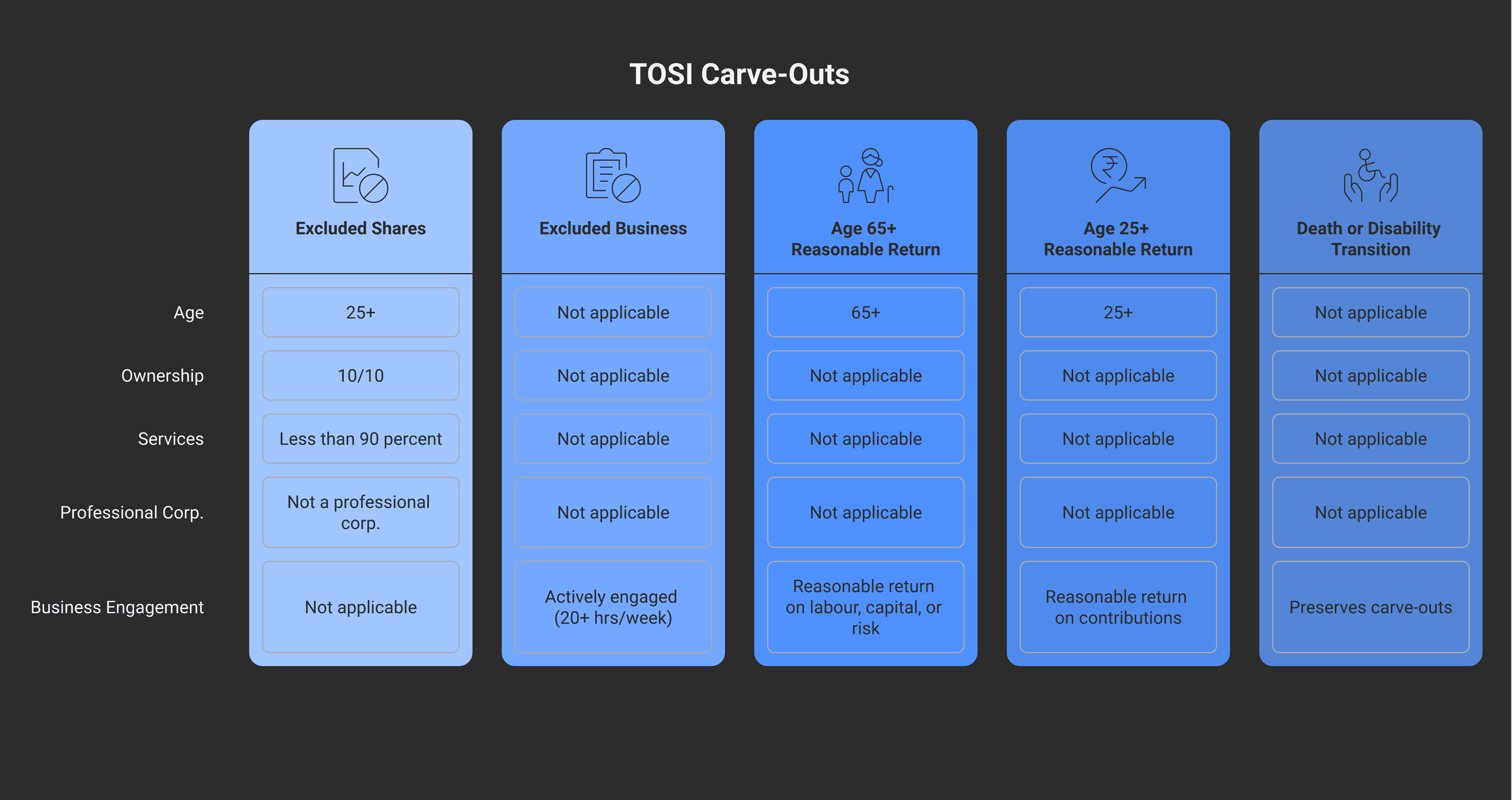

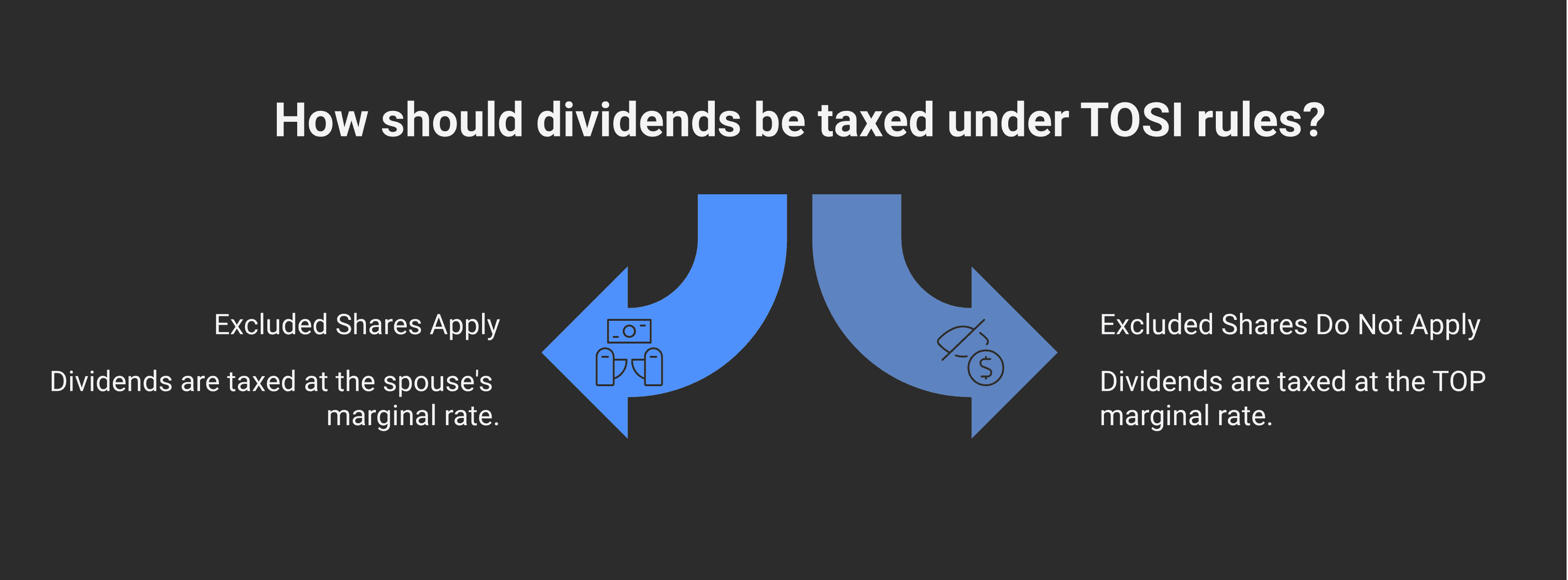

If any one of these fails, the shares are not excluded shares, and dividends paid on them fall under TOSI by default. The other carve-outs (excluded business, reasonable return, age-65+ retirement) may still rescue specific situations — but the excluded shares carve-out is the cleanest and most-used, because it applies regardless of whether the recipient actually works in the business.

The services test — the trip-up

Test 3 is where most professional-services households fail. "Provision of services" is read broadly. Almost any consulting, advisory, technical, or trades-services business derives 90%+ of its revenue from services and fails the test.

The corporations that pass test 3 are typically:

Retail and wholesale businesses (income is from sale of goods, not services)

Construction and renovation contractors (where materials are a meaningful share of revenue — the work is mixed goods + services)

Manufacturing

Real estate holding (rental income is typically not "services")

Restaurants (sale of meals, not pure service)

Mixed businesses where the services component is meaningfully under 90% of total revenue

The corporations that fail test 3:

Pure consulting firms (management, IT, marketing, engineering consulting)

Single-trade subcontractors invoicing labour with negligible materials

Pure professional practices (and these are independently disqualified by the professional corporation rule anyway)

Personal services businesses (which face additional rules under section 18(1)(p))

A contractor whose corporation buys $40,000 of materials per year against $200,000 of total revenue is at 80% services / 20% materials — passes test 3. A contractor whose corporation invoices only labour and bills materials separately to the GC fails test 3.

The other TOSI carve-outs

The excluded shares carve-out is one of five — the others rescue different situations:

Excluded business

If the specified individual is actively engaged on a regular, continuous, and substantial basis in the business, the income is not split income. "Actively engaged" is generally read as averaging 20 or more hours per week in the current year, OR in any five prior taxation years (cumulative, not necessarily consecutive).

The five-year lookback is the critical clause. A spouse who worked 20+ hours/week alongside the owner from 2014 to 2018, then stepped back to raise children from 2019 forward, can still receive dividends free of TOSI because of the historical engagement. The hour records have to survive an audit — which means time logs, calendar entries, email evidence, or contemporary employment records.

Age 65+ reasonable return

Once the recipient is 65 or older, the test loosens. Any income that represents a "reasonable return" on the recipient's contributions — work, capital, or risk — is exempt. The reasonableness test is broader and softer than the under-65 standard, and the rule was a deliberate concession to keep retirement-stage income splitting workable.

Age 25+ reasonable return

For recipients 25 or older but under 65, a reasonable return carve-out still exists — but the standard is stricter. The amount must reflect contributions actually made (labour, capital, financial guarantees, risk borne). The CRA's published guidance for this carve-out is narrower than for the over-65 version.

Death and disability transitions

If a related person who would have qualified for a carve-out dies or becomes disabled, certain provisions in section 120.4 preserve the carve-out for the surviving family. The mechanics are intricate; the rule is meant to prevent TOSI from creating cliff-edge tax consequences in estate situations. (Modern Axis's Why Family Trusts Still Matter covers the broader estate-planning interaction.)

Worked structural example: spouse holding shares in an incorporated business

Take a typical owner-managed corporation in BC where the operator works full-time, the spouse holds shares but does not work in the business, and the dividends are being declared. Three scenarios:

In Scenario A, the structure works. The spouse can receive dividends on the 25% shareholding at her own marginal rate. If she earns nothing else, a $50,000 dividend is taxed at a low effective rate. The combined family tax bill is much lower than if the same $50,000 stayed inside the corp and was eventually paid out to the operating spouse at the top rate.

In Scenario B, the 10%/10% test fails. Even though the corporation is structured correctly (passes the services test), the spouse holds too few shares. The dividend is taxed under TOSI at the top marginal rate. The income split delivers no tax saving.

In Scenario C, the services test fails. Even though the spouse holds 25% — well above the 10%/10% threshold — the corporation is a pure services business. Excluded shares does not apply. The dividend is taxed under TOSI at the top marginal rate.

If you're not sure whether your structure passes, book a consultation — testing this once is dramatically cheaper than discovering it failed when the CRA reassesses three years of dividends.

What this means for incorporation decisions

The TOSI rules are a major reason the decision to incorporate a Canadian business cannot be evaluated on tax integration alone. Two structurally identical owner-managers — both at $200K of business income, both in BC — can have wildly different optimal structures depending on whether the corporation's revenue is services-heavy (TOSI risk) or goods-heavy (excluded shares available).

For a retail, manufacturing, or mixed business, dividend sprinkling to a spouse who owns 10%+ of votes and value is generally clean. For a pure consulting practice, dividend sprinkling is largely off-limits unless the spouse has genuine active engagement (the 20+ hours/week test) or fits the 65+ reasonable return rule.

The corporate structure has to be designed around this. Common levers:

Re-issue shares to give the spouse 10%+ of votes and value if they currently hold less. Section 86 reorganisations and freezes are the usual mechanic.

Pay the spouse a reasonable salary for actual work performed instead of dividends. Salary sidesteps TOSI but creates CPP exposure on both sides and requires documented work.

Use a family trust to hold shares (the Family Trusts post covers when this still works post-TOSI).

Hold capital outside the operating corp in a holdco where the income mix is different — investment income flowing through a holdco may also avoid TOSI through different carve-outs.

These structural choices are usually best made at incorporation, but can be retrofitted later through reorganisations.

When the TOSI question lands on Modern Axis

Modern Axis CPA reviews TOSI exposure as part of every annual planning engagement for incorporated owner-managers — structural assessment, share-class review, excluded-shares positioning, and where carve-outs aren't available, designing the salary/dividend mix accordingly. The Tax Planning & Compliance service covers the annual review; restructuring (share re-issues, holdco insertions, family trust mechanics) is its own engagement scope. For owners considering whether incorporation still makes sense given a services-heavy revenue mix, the broader should you incorporate framework applies first.

Frequently asked questions

What is TOSI under section 120.4 of the Income Tax Act?

Tax on Split Income — section 120.4 of the Income Tax Act. Since 2018, it applies the top combined marginal tax rate to split income (dividends, interest, certain partnership and trust income) received by adult family members from a related private business, unless a statutory carve-out applies. The purpose is to eliminate the tax benefit of distributing corporate income across multiple low-bracket family members through family share structures.

What are excluded shares under TOSI?

Excluded shares are a TOSI carve-out in subsection 120.4(1). Three tests must all pass: the recipient is 25 or older; they own at least 10% of votes AND 10% of value of all shares of the corporation; and less than 90% of the corporation's business income is from services. Independently, the corporation must not be a professional corporation. If all conditions are met, dividends on those shares are taxed at the recipient's marginal rate, not the top rate.

Does TOSI apply to professional corporations?

Yes — and the excluded shares carve-out is explicitly unavailable. Section 120.4(1) lists professional corporations as a category for which excluded shares cannot apply. Medical, dental, legal, accounting, chiropractic, and veterinary professional corporations cannot use this carve-out. The other carve-outs (excluded business, reasonable return, age 65+) may still apply if the facts support them.

Can a non-working spouse receive dividends without triggering TOSI?

Yes, but only if the shares qualify as excluded shares (10%/10%, age 25+, non-services corporation), or if the spouse is 65 or older and the dividend is a reasonable return, or under specific death or disability transitions. The active engagement carve-out requires actual work history of 20-plus hours per week, current or in any five prior years. A passive spousal shareholder who never worked in the business relies entirely on the excluded shares test.

What happens if I fail the excluded shares test under TOSI?

TOSI applies — the dividend is taxed at the top combined federal and provincial marginal rate (approximately 53.5% in BC for the highest bracket). The benefit of splitting income to a lower-tax-bracket family member is eliminated. Any other available carve-out (excluded business, reasonable return) might still apply on the facts, but excluded shares is the cleanest and most common path; failing it usually means the split structure was not effective.

How is the 10%/10% ownership test measured for TOSI excluded shares?

At the time the dividend is paid, the specified individual must hold shares representing at least 10% of votes and at least 10% of fair market value of all issued and outstanding shares. The test runs on issued shares, not authorised. Shares freshly issued or retired around the dividend date affect eligibility — planning the share structure ahead of a dividend declaration matters, since the test is a snapshot, not a year-long average.