T1134 Foreign Affiliate Reporting: A Plain-English Guide

T1134 is one of the most demanding compliance forms Canadian residents and corporations ever encounter — and it catches owners of fairly modest cross-border structures every year. If you hold 10% or more of any class of shares of a non-resident corporation, you have a T1134 reporting obligation. A Canadian-resident owner of a single-member US LLC, a snowbird with a small US "C-corp" rental holding, a small business owner whose foreign sales subsidiary just crossed 10% — all in scope.

The form is information-only — it does not assess tax. But the penalty structure for missing it is severe (up to $12,000 per affiliate under gross negligence, plus a 5% cost-of-shares penalty after 24 months), and the filing deadline is unusual: 10 months after the taxation year-end for tax years starting after December 31, 2020 — much earlier than the standard T1 or T2 deadline.

This guide walks through the T1134 obligation under section 233.4 of the Income Tax Act, the difference between a foreign affiliate (FA) and a controlled foreign affiliate (CFA), the dormant-affiliate exemption, the Summary versus Supplement split, the penalty ladder, and the typical cross-border-owner scenarios.

Key takeaways

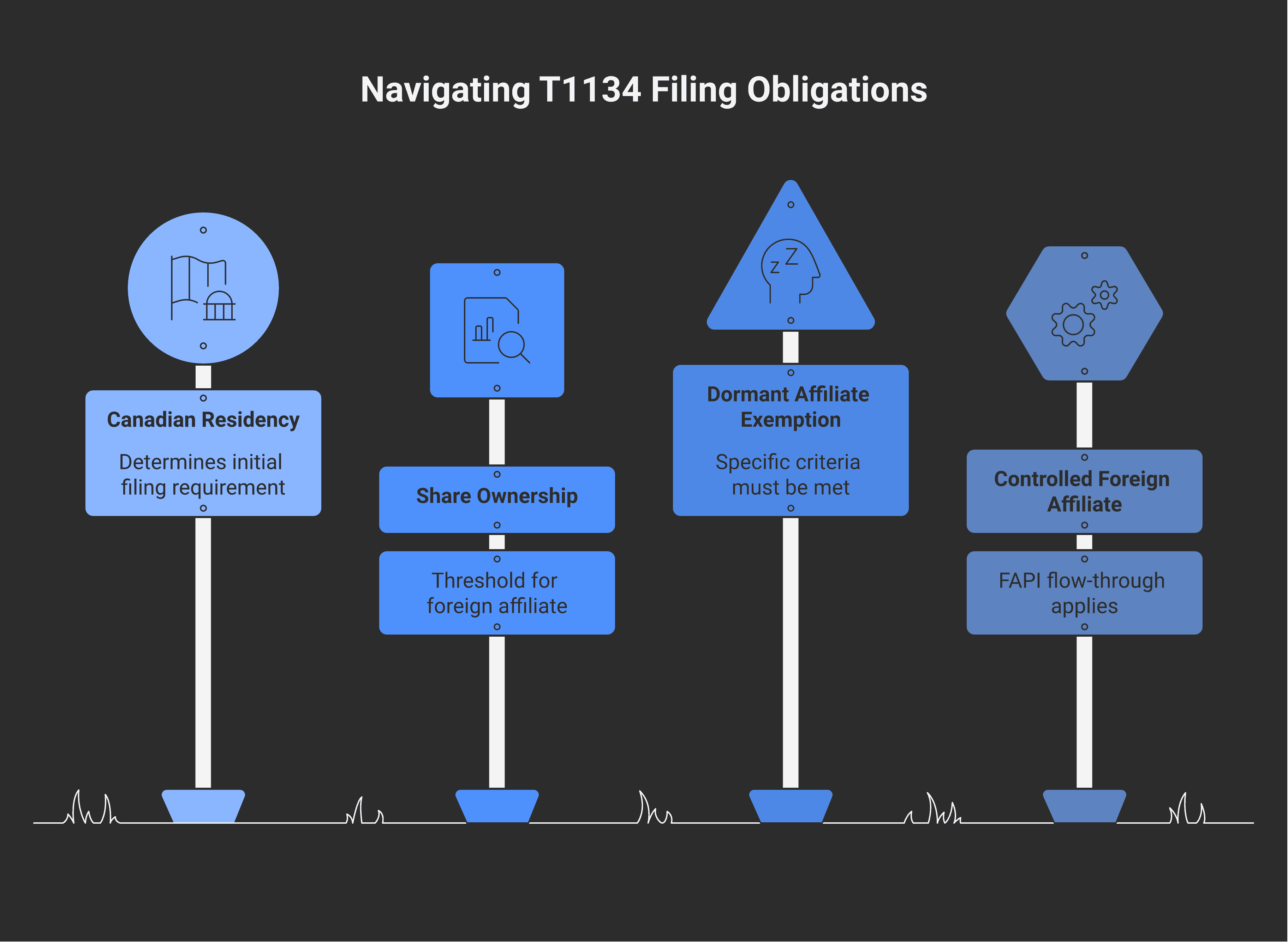

A Canadian-resident individual, corporation, trust, or qualifying partnership must file Form T1134 for any year in which they had a foreign affiliate under subsection 233.4 of the Income Tax Act. A foreign affiliate is a non-resident corporation in which the Canadian taxpayer holds an equity percentage of 10% or more of any class of shares (per the definitions in section 95(1) of the ITA, modified for T1134 purposes by section 233.4).

A controlled foreign affiliate (CFA) is a foreign affiliate that is controlled by the Canadian taxpayer alone, by the Canadian taxpayer plus related parties, or by combinations of up to four arm's-length Canadian residents and their related parties. CFAs face the FAPI (foreign accrual property income) regime in addition to T1134.

Filing deadline is 10 months after taxation year-end — for tax years starting after December 31, 2020 — much earlier than the T2 corporate return (six months) or T1 personal return (April 30). For prior years the deadline was 12 months (2020) or 15 months (pre-2020).

The dormant affiliate exemption: no T1134 Supplement is required for a foreign affiliate where the Canadian taxpayer's cost amount in the affiliate was under CAD $100,000 at all times in the year AND the affiliate had under CAD $100,000 of gross receipts AND under CAD $1,000,000 of FMV assets.

Late filing penalties mirror T1135: $25 per day to $2,500 maximum under subsection 162(7), escalating to $500 per month for 24 months ($12,000) for gross negligence under subsection 162(10), plus a 5% cost-of-shares penalty after 24 months of non-compliance.

What is a "foreign affiliate"?

The definition is at section 95(1) of the Income Tax Act, modified for T1134 purposes by subsection 233.4(2). In plain terms:

A Canadian-resident taxpayer has a foreign affiliate if all three of these are true:

The taxpayer holds an equity percentage of at least 1% in a non-resident corporation directly, and

The taxpayer (together with related persons) holds an equity percentage of at least 10% of any class of shares of that non-resident corporation.

"Equity percentage" is the higher of the percentage of voting shares and the percentage of fair-market-value participation. The 1% direct + 10% with related is the technical floor — but in practical terms what most people care about is whether the Canadian taxpayer (alone or with related persons) holds 10% or more.

Examples:

A Canadian holding 100% of a single-member US LLC → foreign affiliate (LLC is classified as a corporation under Canadian law) ✓

A Canadian holding 15% of a Cayman Islands holding company → foreign affiliate ✓

A Canadian holding 8% of a US C-corp, where their spouse holds another 5% → foreign affiliate (related-party aggregation = 13%) ✓

A Canadian holding 4% of a foreign public company → not a foreign affiliate (below the 10% threshold)

A Canadian beneficiary of a non-resident trust → reportable on T1141 or T1142, not T1134 (different regime)

Controlled foreign affiliate (CFA) — the deeper layer

A foreign affiliate is a CFA — a "controlled foreign affiliate" — if any of the following control tests is met:

Wholly controlled by the Canadian taxpayer (single Canadian holds majority equity/voting)

Controlled by the Canadian taxpayer alone or with related parties

Controlled by the Canadian taxpayer plus up to four arm's-length Canadian residents and their related parties (joint Canadian-owned blocks count toward control)

The CFA designation matters beyond T1134: a CFA's foreign accrual property income (FAPI) — passive income earned inside the foreign corporation — is deemed to flow through to the Canadian shareholder annually, even if not distributed. This is the Canadian equivalent of US Subpart F / GILTI. Tax planning around FAPI is the reason many cross-border structures specifically avoid the CFA designation, sometimes at the cost of efficiency in other areas.

For T1134 purposes specifically, a CFA requires the full Supplement information disclosure. A non-controlled foreign affiliate (often called a "mere FA") has a slightly less demanding reporting burden, but still requires the Supplement unless dormant.

The dormant affiliate exemption

The most common relief from T1134 reporting is the dormant-affiliate exemption. No T1134 Supplement is required for a foreign affiliate where all three of these conditions are met for the affiliate's taxation year ending in the reporting year:

The Canadian taxpayer's cost amount in the foreign affiliate was less than CAD $100,000 at all times in the year (this is "below threshold" — usually a small, modest-size FA)

The foreign affiliate's gross receipts (including proceeds from the disposition of property) were less than CAD $100,000 in the year

The foreign affiliate's assets had a fair market value of less than CAD $1,000,000 at all times in the year

A truly dormant US LLC with no activity in the year, owned at low cost, easily meets all three. But a US LLC with even modest rental income or property holdings can blow through the $100K gross receipts or $1M FMV test quickly.

When the exemption applies, the Canadian taxpayer must still file the T1134 Summary (basic identification of the affiliate), but does not need to file the per-affiliate Supplement (the detailed financial information).

Summary vs Supplement

The T1134 form has two main parts:

T1134 Summary — one Summary per reporting entity per year. Lists each foreign affiliate, basic identification (name, country, share class held, ownership percentage), and whether each is a CFA or non-CFA.

T1134 Supplement — one Supplement per foreign affiliate (except those qualifying for the dormancy exemption). Includes:

Financial statements of the foreign affiliate (or summary financial data)

Surplus account balances (exempt surplus, taxable surplus, hybrid surplus, pre-acquisition surplus — these tax pools drive the dividend integration math)

FAPI calculation (for CFAs)

Inter-corporate transactions between the Canadian taxpayer and the affiliate

Loans or advances to/from the Canadian taxpayer

The Supplement is where the bulk of the work happens. For a single Canadian holding two foreign affiliates, that's potentially two Supplements plus one Summary in a single filing.

The 10-month deadline

For taxation years starting after December 31, 2020, the T1134 must be filed within 10 months of the year-end. For a December 31, 2025 year-end, that's October 31, 2026.

Historical deadlines:

Tax years starting before January 1, 2020: 15 months

Tax years starting in 2020: 12 months

Tax years starting after December 31, 2020 (current): 10 months

This is much shorter than the T2 corporate return deadline (6 months) or the T1 personal deadline (April 30 of the following year, June 15 for self-employed). For a December 31, 2025 corporate year-end, the T2 is due June 30, 2026 but the T1134 is due October 31, 2026 — so the T1134 typically follows the T2 by a few months. The mismatch catches a lot of preparers, especially in the first year a new foreign affiliate is added.

There is no separate extension for the T1134. Where any of the underlying financial information from the foreign affiliate is genuinely unavailable by the deadline, filing with reasonable estimates is preferable to missing the deadline.

Penalties

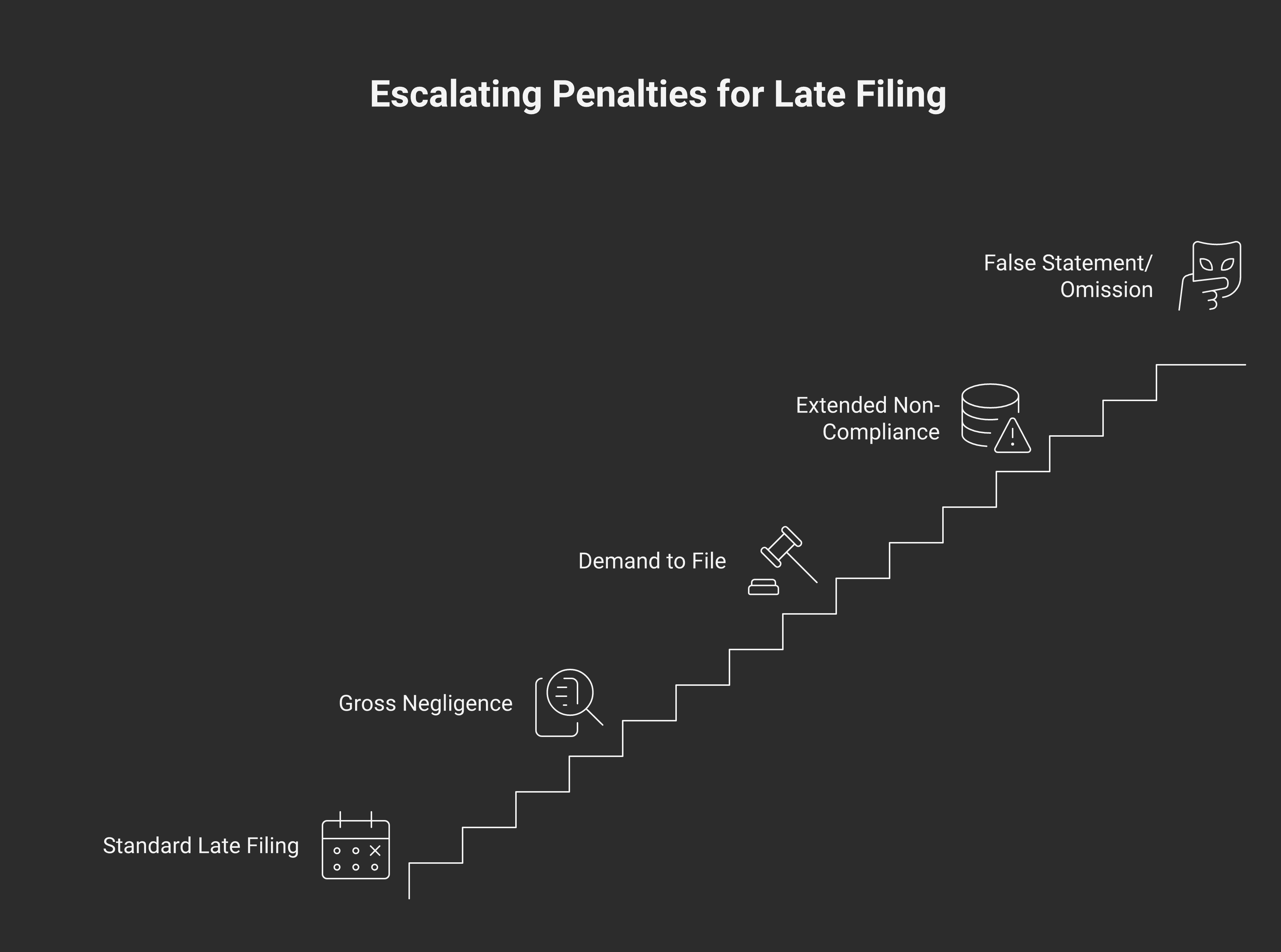

Standard late-filing penalty (subsection 162(7) of the Income Tax Act):

$25 per day, starting day after due date

Minimum: $100

Maximum: $2,500 per Supplement (per foreign affiliate)

For a Canadian holding three foreign affiliates that all miss the deadline, the total exposure is up to $7,500.

Gross negligence penalty (subsection 162(10)):

If CRA determines the failure was knowing or grossly negligent

$500 per month for up to 24 months

Maximum: $12,000 per affiliate

If CRA issued a "demand to file" before the failure: doubles to $24,000

Extended non-compliance penalty (after 24 months):

5% of the cost amount of the Canadian taxpayer's interest in the foreign affiliate (shares + indebtedness)

This is the penalty that scales with the size of the structure — a $500K FA face value triggers a $25,000 penalty

False statement / omission penalty (subsection 163(2.4)):

Greater of $24,000 and 5% of the cost amount of the unreported interest

The cumulative effect for a high-value foreign affiliate filed late and inaccurately can easily reach six figures of penalties on a return that imposes no tax of its own.

Common owner scenarios

Canadian holding a single-member US LLC. US LLCs are classified as corporations for Canadian tax purposes (this is the standard Canadian-CRA classification — different from the US "disregarded entity" treatment). The Canadian owner has a foreign affiliate from year one. If the LLC has any meaningful activity (rental property income, an active small business), the dormant exemption likely doesn't apply, and a full Supplement is required. The owner often coordinates the Canadian T1134 with their US Form 5471 (if a US person) — different forms, similar concepts, both required.

Canadian holding a US C-corp. Standard corporation-to-corporation reporting. The C-corp is a foreign affiliate; if the Canadian holds majority equity it's also a CFA. FAPI implications apply to any passive income (interest, rents, royalties) earned inside the C-corp.

Small Canadian operating corporation with a foreign sales subsidiary. A common structure where the Canadian parent operates in Canada and sets up a foreign sales arm (commonly in the US or a low-tax jurisdiction) to handle international sales. The subsidiary is a CFA. The parent files the T1134 — not the subsidiary itself, which is a non-resident. Sales income earned by the CFA is generally active business income, not FAPI, so the FAPI flow-through doesn't bite — but the T1134 reporting still applies.

Canadian estate or trust with a foreign holding company. Trusts and estates are reporting entities for T1134 purposes. The 10-month deadline runs from the trust's year-end. For graduated rate estates (GREs) with December 31 year-ends, that's October 31 — same as a calendar-year corporation. We cover the trust dimension in our family trusts post.

Canadian-resident US citizen owning US private investments. Triple-form coordination: US Form 5471 (US side), Canadian T1134 (Canadian side), T1135 for any non-affiliate foreign property (Canadian side), and possibly FBAR if foreign account balances exceed US$10K. All four are information returns, none of which assess tax directly, but each carries its own penalty regime.

Practical planning

Run the 10% test annually. Equity percentages change with new issuances, redemptions, transfers. A position that was 8% last year may have crossed to 11% this year through a redemption-driven concentration. The T1134 obligation can appear suddenly with no operational change.

Track surplus account balances year-round. Foreign affiliate surplus accounts (exempt surplus, taxable surplus, hybrid surplus, pre-acquisition surplus) drive the integration of dividends paid from the affiliate back to the Canadian shareholder. Bringing these up to date only at filing time is how preparation slips and Supplement disclosures get incomplete.

Coordinate with US Form 5471 (where applicable). If the Canadian taxpayer is also a US person and the foreign affiliate is a foreign corporation in US-tax terms, both the Canadian T1134 and US Form 5471 typically apply. The financial information overlaps; the form structures don't. Plan the year-end close around feeding both.

Re-examine the dormant exemption each year. A foreign affiliate that qualified for the exemption last year may not this year. The $100K cost / $100K gross receipts / $1M FMV thresholds are tested each year — small changes in the affiliate's operations or asset base can flip the test.

Don't miss the deadline by relying on the T2 deadline. Canadian preparers default to the T2 corporate deadline (six months after year-end) as the "internal" deadline for finalising the year. The T1134 is four months later. A workflow that finalises the T2 by the deadline but leaves the T1134 for "later" runs into the late-filing penalty in October.

For cross-border owner-managers at Modern Axis, the T1134 is part of an annual recurring engagement — coordinated with Canadian T1/T2 prep, US Form 5471/8865/8858 (depending on entity classification), T1135 foreign property reporting, and FBAR where applicable. The cost of getting it right is small relative to the penalties for getting it wrong.

Frequently asked questions

Who has to file Form T1134?

Any Canadian-resident individual, corporation, trust, or qualifying partnership that had a foreign affiliate at any time in the taxation year must file Form T1134, under section 233.4 of the Income Tax Act. A foreign affiliate is a non-resident corporation in which the Canadian taxpayer (alone or with related persons) holds an equity percentage of at least 10% of any class of shares.

What is the difference between a foreign affiliate and a controlled foreign affiliate?

A foreign affiliate (FA) is a non-resident corporation in which the Canadian taxpayer holds at least 10% equity of any class of shares. A controlled foreign affiliate (CFA) is a foreign affiliate that is controlled by the Canadian taxpayer alone, by the Canadian taxpayer plus related parties, or by combinations of up to four arm's-length Canadian residents and their related parties. CFA status triggers the foreign accrual property income (FAPI) regime — passive income earned inside the CFA is deemed to flow through to the Canadian shareholder annually, even if not distributed.

When is the T1134 due?

For taxation years starting after December 31, 2020, the T1134 is due 10 months after the taxation year-end. For a December 31, 2025 year-end, that's October 31, 2026. Historical deadlines were 12 months for tax years starting in 2020 and 15 months for years starting before 2020. The deadline is much earlier than the T1 (April 30) and T2 (six months after year-end) deadlines.

What is the dormant foreign affiliate exemption?

A foreign affiliate qualifies for the dormancy exemption — meaning no T1134 Supplement is required — when all three of the following conditions are met for the affiliate's taxation year: (1) the Canadian taxpayer's cost amount in the affiliate was under CAD $100,000 at all times in the year; (2) the affiliate's gross receipts were under CAD $100,000 in the year; (3) the affiliate's assets had a fair market value under CAD $1,000,000 at all times in the year. The taxpayer must still file the T1134 Summary identifying the affiliate.

What is the difference between T1135 and T1134?

T1135 reports specified foreign property held by a Canadian resident (foreign bank accounts, US shares in Canadian brokerage, foreign rental property) where the total cost exceeds CAD $100,000 — see our T1135 guide. T1134 reports a Canadian's ownership of foreign affiliates (10%+ of any class of shares of a non-resident corporation). Foreign-affiliate shares are specifically excluded from T1135 — they go on T1134 instead.

What are the penalties for filing T1134 late?

Standard late-filing penalty is $25 per day, $100 minimum, $2,500 maximum per Supplement under subsection 162(7). Gross negligence escalates to $500 per month for up to 24 months ($12,000 maximum) under subsection 162(10). If CRA issued a "demand to file" before the failure, the gross negligence penalty doubles to $24,000. After 24 months of non-compliance, a 5% penalty on the cost amount of the Canadian taxpayer's interest applies. False statement or omission penalty is the greater of $24,000 and 5% of the cost amount of the unreported interest.

Do I have to file T1134 for a US LLC I own as a Canadian?

Yes. A US LLC — even a single-member US LLC — is classified as a corporation for Canadian tax purposes (the CRA does not respect the US "disregarded entity" treatment). A Canadian owning 10% or more of a US LLC has a foreign affiliate and a T1134 filing obligation. If the Canadian is also a US person (citizen or green card holder), they additionally have US Form 5471 reporting obligations from the US side.

Cross-border tax is fact-specific by nature — citizenship, residency, treaty positions, entity classifications, and prior filings can flip the analysis entirely. This post lays out general principles, not advice for your situation, and it cannot cover every angle that might apply to you. Speak with a Canadian and/or US tax professional who can review your full picture before relying on anything you've read here.

Alex Ataman, CPA

Founder

Modern Axis CPA