Spousal and Child Support Tax in Canada (2026)

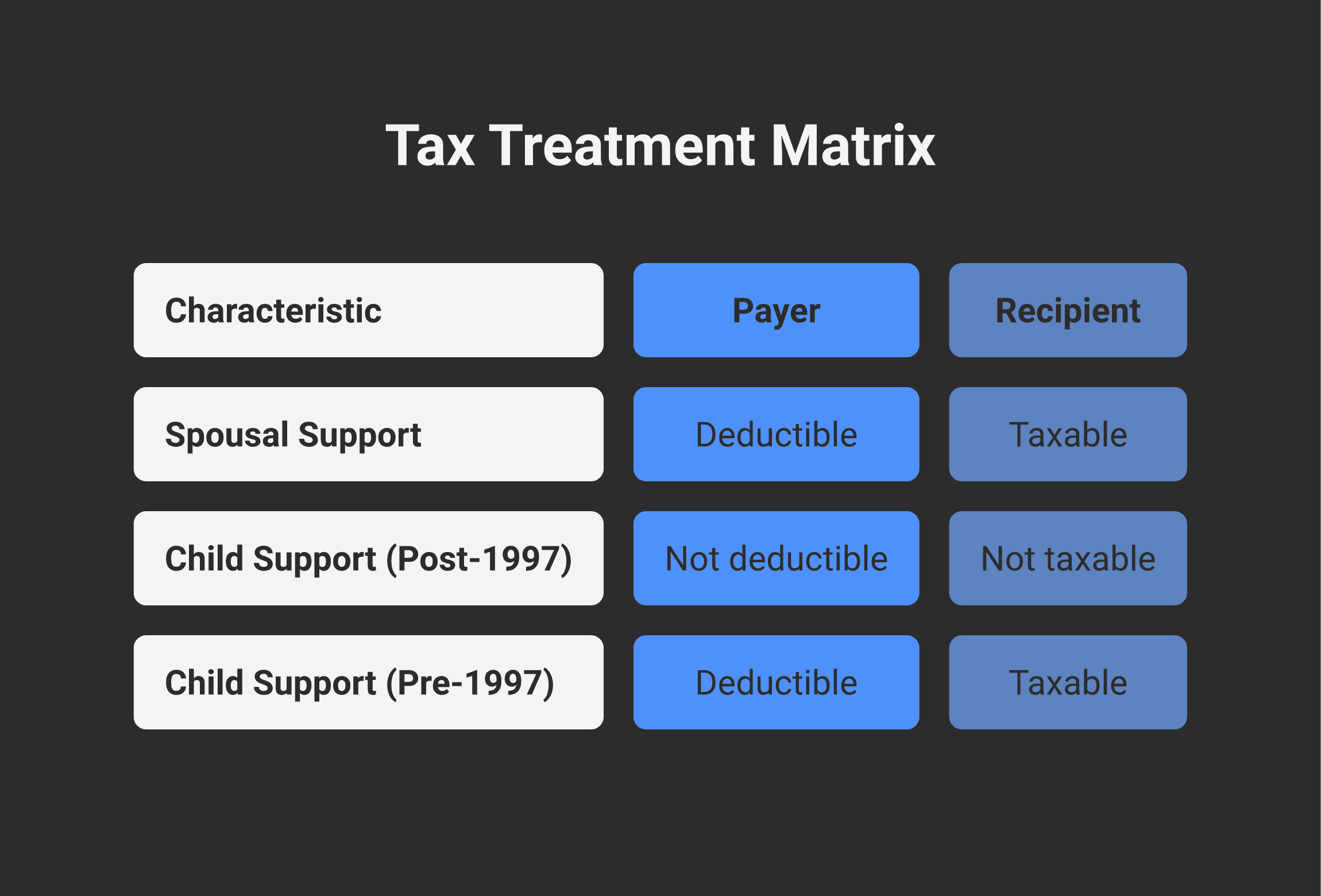

The tax treatment of support payments after a separation or divorce is one of the cleanest binaries in Canadian tax law: spousal support is taxable to the recipient and deductible to the payer; child support is neither. That two-line rule, set in subsections 56.1, 56(1)(b), and 60(b) of the Income Tax Act, drives the entire framework.

What turns a simple binary into actual complexity is everything around it. The payment has to come from a court order or a written agreement that meets statutory tests. Periodic payments are treated differently from lump-sum payments. Pre-1997 child support orders are grandfathered into the old (taxable/deductible) regime. Legal fees have their own deductibility rules. The supporting spouse and child amounts on a tax return interact with whether support is being paid. And the Canada Child Benefit allocation between separated parents depends on shared custody arrangements that don't always match what the court order says on paper.

This guide walks through how spousal and child support are taxed under sections 56.1, 56(1)(b), 60(b), and 60.1 of the Income Tax Act, the periodic-vs-lump-sum allocation rules, the pre-1997 grandfathering of child support orders, when legal fees are deductible, and the CCB and credit allocation between separated parents.

Key takeaways

Spousal support is taxable to the recipient and deductible to the payer when paid periodically (typically monthly) under a court order or written separation agreement, under subsection 56(1)(b) and paragraph 60(b) of the Income Tax Act.

Child support is neither taxable nor deductible for any order or written agreement dated May 1, 1997 or later. Orders predating May 1, 1997 follow the old regime (taxable/deductible) unless the parties have elected into the current rules.

Lump-sum payments are not deductible as periodic spousal support. CRA's allocation rules under Income Tax Folio S1-F3-C3 treat amounts paid as lump sums as capital settlements rather than periodic support.

Legal fees incurred to enforce or establish spousal support entitlement (for the recipient) are deductible. Legal fees incurred to defend or pay support are generally not. Legal fees to negotiate a settlement that mixes support with property division are partially deductible.

CCB allocation between separated parents in shared-custody arrangements is split based on the residency periods documented to CRA on Form RC65 or RC66 — not necessarily 50/50 even when custody is 50/50.

The two-line rule

For any court order or written separation agreement dated May 1, 1997 or later:

Type of support | Payer treatment | Recipient treatment |

|---|---|---|

Spousal support (periodic) | Deductible from income under paragraph 60(b) | Taxable as income under paragraph 56(1)(b) |

Child support | Not deductible | Not taxable |

The May 1, 1997 cutoff date is statutory. Federal Bill C-92 amended the Income Tax Act to remove the taxable/deductible treatment of child support for orders and written agreements made after April 30, 1997 (commonly known as the "1997 child support reforms"). Pre-1997 orders continue to follow the old regime unless the parties have signed an election to move to the current rules.

What counts as "spousal support"

The legal definition. To qualify for the deductible/taxable treatment as spousal support, the payments must:

Be made under a court order or a written separation agreement (an oral or implicit arrangement does not qualify)

Be paid to a spouse or former spouse or common-law partner (the parties must have been spouses or common-law partners at some point)

Be paid periodically (typically monthly) — not as a lump sum

Be in respect of the maintenance of the recipient (their personal support, including housing, food, transportation), not specific items like the children's school fees or medical expenses

The distinction between spousal support and other transfers between separated spouses matters a lot in practice. A court order that says "$X per month to the recipient until further order" — that's spousal support. A clause that says "the payer will cover the children's hockey costs" — that's not periodic spousal support, even if it's regular and recurring; it's a directed payment for specific items that CRA treats as a property settlement.

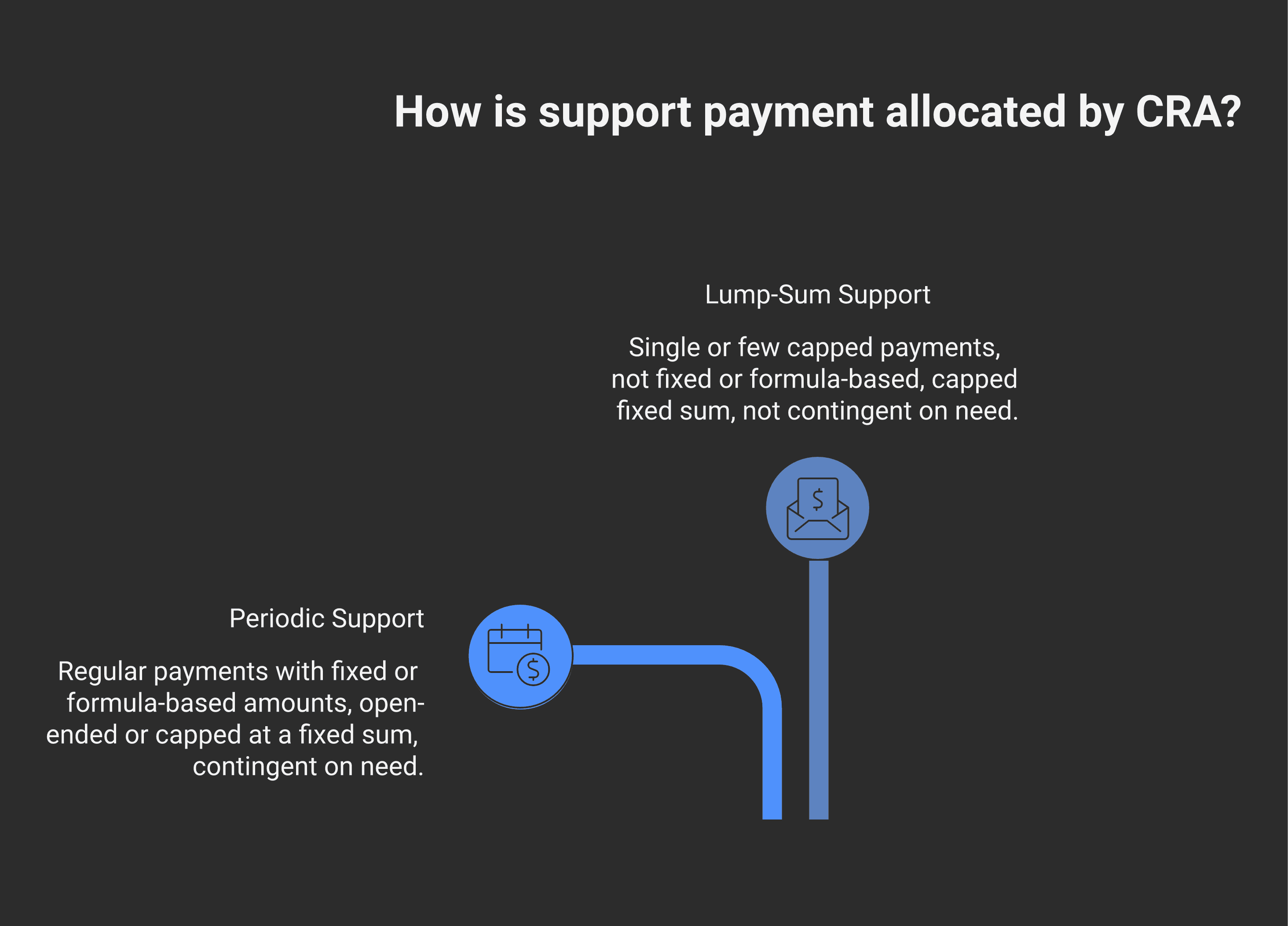

Periodic vs lump-sum allocation

The most common practical fight with CRA on support tax treatment is whether a payment is periodic (deductible/taxable) or lump-sum (not deductible/not taxable). CRA's Income Tax Folio S1-F3-C3 lays out the criteria.

Periodic characteristics:

Paid at regular intervals (monthly is typical; quarterly is acceptable)

The amount is fixed per interval or determined by a formula

The right to receive each payment arises only when the interval is reached

The total amount over the period is not capped at a fixed sum (though it may be capped at a yearly or monthly maximum)

Lump-sum characteristics:

A single payment or a small number of payments

Each payment represents a definite portion of an overall settlement

The total is capped at a fixed sum

The payments are not contingent on the recipient's continued need for support

Practical examples that CRA treats as lump-sum (not deductible):

$50,000 paid at separation as a "settlement of all matrimonial claims"

Three annual payments of $25,000 each

A monthly payment that decreases on a schedule until reaching zero, where the total is a fixed amount

Practical examples that CRA treats as periodic (deductible/taxable):

$4,000 per month indefinitely

$3,500 per month for five years subject to review

A monthly amount tied to the payer's earnings (with a formula)

A common trap: a court order that calls a payment "lump-sum spousal support" or "lump-sum support" — CRA looks past the label to the substance. If the underlying mechanic is a single payment in settlement, it is not deductible. The label does not control.

Retroactive periodic payments. A specific exception: if a court orders an arrears amount payable on a specific date that catches up periodic support that was unpaid, the arrears qualify as periodic and remain deductible/taxable to the appropriate parties. The recipient can spread the income across multiple years using the retroactive lump-sum payment averaging mechanic in section 110.2 if the arrears cover more than one year.

Pre-1997 child support orders — grandfathered

Court orders or written agreements dated April 30, 1997 or earlier that specified child support continue to follow the old regime: child support is deductible to the payer and taxable to the recipient.

This is increasingly rare in practice — most pre-1997 orders have been varied or replaced, putting the parties into the current regime. But the grandfathering remains alive for orders where the original obligation continues unchanged.

Three triggers that move a pre-1997 order into the current regime:

The parties signed Form T1158 (Registration of Family Support Payments) electing into the current regime

A varying order changed the amount of child support after April 30, 1997 — the variation moves the entire child support obligation into the current regime

A new agreement replaced the old one — substantive replacement moves to current regime

A varying order that only changes spousal support but leaves child support unchanged generally does not trigger the move. Subtle but consequential — a 1996 order varied in 2003 just on spousal support means the child support component remains pre-1997 (deductible/taxable).

Legal fees — when they're deductible

Legal fees incurred in family law matters are treated differently depending on who incurred them and for what purpose:

Deductible to the recipient:

Legal fees to establish, enforce, or collect spousal support

Legal fees to establish, enforce, or collect child support (post-1997 too, even though the support itself is not taxable)

Legal fees to establish entitlement to retroactive periodic support

Legal fees to defend against a reduction in support

Not deductible to the payer:

Legal fees to negotiate down or defend against support obligations

Legal fees for property division, custody, or access disputes (these are personal-capital expenses)

Partially deductible: Fees for an agreement that mixes support entitlement with other elements (property division, custody) can be deducted to the extent reasonably allocable to the support component. The lawyer's invoice should ideally break out time by issue to support an allocation.

For divorce itself: Legal fees solely for obtaining a divorce are not deductible by either party. The divorce itself is a personal proceeding.

CRA's Income Tax Folio S1-F3-C3 paragraph 3.78 et seq sets out the analysis. The recipient claims deductible legal fees on Line 22100 of the T1 return.

Spousal and child amounts on the return

A few credit lines interact with support arrangements:

Eligible dependant amount (formerly equivalent-to-spouse). Under paragraph 118(1)(b), a separated parent who is single and supports a child can claim the eligible dependant amount ($16,452 for 2026, the same maximum as the basic personal amount) for one of their children. Combined with the Canada caregiver credit for an infirm dependant, this is a meaningful credit. Only one parent can claim it per child; in shared custody arrangements the parents must agree which one claims.

Canada caregiver credit. Available for a spouse or dependant with a marked impairment. After separation, neither parent can claim the caregiver credit for a former spouse — they are no longer "spouses" for tax purposes. The credit can still be claimed for a dependent child or other family member with a marked impairment, under either parent's return as agreed. The mechanics intersect with the DTC stack where the dependant has an approved Form T2201.

Spousal credit. The spousal credit (line 30300, up to $16,452 for 2026) is only available if you supported a spouse or common-law partner during the year. The mechanics for supporting a non-resident spouse are stricter — Canadian residency is not required, but the support has to actually be provided and documented. After legal separation, the spousal credit is no longer available — even though support is being paid.

CCB allocation between separated parents

The Canada Child Benefit is allocated based on the "primarily responsible" parent determination, and after separation can be split or alternated depending on custody arrangements.

Full custody (one parent). The parent with primary residency receives 100% of the CCB for that child.

Shared custody (40-60% with each parent). Under section 122.6, each parent receives 50% of the CCB amount they would receive if they had full custody — and the two amounts are based on each parent's income separately. So a high-income parent receives less of their 50% and a lower-income parent receives more of their 50% — the total household CCB after separation typically exceeds the household CCB before, because the formula uses individual rather than family income.

Variable custody arrangements. Where the time split is not roughly equal, CRA allocates the CCB based on which parent is "primarily responsible" — typically the one with the majority of nights. The supporting parent reports their share on their own benefit application.

To trigger the CCB split, separated parents must file Form RC65 (Marital Status Change) and Form RC66 (Canada Child Benefit Application) confirming the custody arrangement.

Common mistakes

Treating a lump-sum settlement as deductible spousal support. The biggest single error. The payer deducts the lump sum on their return; CRA reassesses; the recipient (who also reported the amount as taxable income) has to file a T1-ADJ to back out the income reported. Net effect: payer loses the deduction, recipient gets their tax back, but the legal and accounting costs of resolving the reassessment can run to thousands.

Forgetting to update the marital status with CRA. Separated parents who don't notify CRA continue to receive credits and benefits based on the pre-separation family unit. Once CRA catches the discrepancy (often 2-3 years later via the random-audit pool), reassessment of the under-reported income or over-paid benefits is straightforward — and stressful.

Not deducting legal fees that qualify. Recipients often pay $5,000-$15,000 in legal fees to establish or collect support and don't claim the deduction. The fee is allocable on Line 22100. Even modest amounts add up over a multi-year separation process.

Pre-1997 child support assumed to be the new regime. Older clients with orders predating May 1, 1997 sometimes assume the new "no deduction, no income" rule applies. It doesn't, unless they signed T1158 or had a varying order. The income side of the equation can be material.

CCB split assumed to be 50/50 in shared custody. It usually isn't, because the formula uses individual income, not family income. Two parents with very different earnings produce very different individual CCB amounts even when custody is exactly 50/50.

Planning around separation

A few practical moves for a separating couple from a tax perspective:

Capture the support obligation in writing. Without a written agreement or court order, support is not deductible. Even when the relationship is amicable, a written separation agreement protects the payer's deduction.

Allocate carefully between spousal and child components. In high-income separations where one party is in a much higher bracket, weighting more of the payment toward spousal support (deductible to the payer, taxable to the recipient at a typically lower marginal rate) can produce meaningful family-wide tax savings. Run the math against the actual 2026 bracket schedule rather than guessing — the difference between top-bracket and middle-bracket combined rates is the size of the available saving. The recipient should also be brought into the planning conversation since they bear the tax cost.

Time the marital status change. CRA recognises separated status when there is a 90-day separation. Filing as separated for the year affects credits, benefits, and the eligible dependant amount. The change typically takes effect for the year in which the 90 days are met.

For child support owing to other parties: If the recipient parent owes child support to a third party (e.g., from a prior relationship), the structure of the new family's CCB allocation matters. The owed amount typically gets garnisheed from family allowances if not paid voluntarily.

Consider the registered pension plan and RRSP allocation as part of the matrimonial property settlement. Property settlements between former spouses can include a tax-deferred transfer of RRSPs under paragraph 146(16)(b) of the Income Tax Act, filed on Form T2220 — the parties must be living separate and apart, and the transfer must be made pursuant to a written separation agreement or court order relating to a division of property in settlement of rights arising out of the breakdown. The transfer does not trigger income on either party. Pension splits work under the Pension Benefits Standards Act and provincial equivalents.

If you're navigating a separation, the tax decisions matter alongside the legal ones. Property and trust planning during a separation often touches the family trust framework too, and the broader income-splitting toolkit gets reshuffled when a couple becomes two separate tax units. The team at Modern Axis works alongside the family law team on the support-payment structuring, the marital status filing changes, and the CCB allocation calculations to make sure the tax mechanics line up with what was negotiated legally.

Frequently asked questions

Is spousal support taxable in Canada?

Yes. Spousal support paid periodically under a court order or written separation agreement is fully taxable as income to the recipient under paragraph 56(1)(b) of the Income Tax Act, and fully deductible to the payer under paragraph 60(b). The payments must be made periodically (typically monthly) rather than as a single lump sum, and they must be paid in respect of the maintenance of the recipient.

Is child support tax deductible in Canada?

No, for any court order or written agreement dated May 1, 1997 or later. Child support is neither deductible to the payer nor taxable to the recipient under the current regime. Pre-1997 orders (or earlier) that have not been varied or replaced remain in the old regime — child support is deductible/taxable under those orders unless the parties have elected to move to the current rules via Form T1158.

Can I deduct a lump-sum spousal support payment?

Generally no. CRA treats lump-sum payments as capital settlements rather than periodic support, and the deduction under paragraph 60(b) requires the payment be periodic. The label in the court order or agreement does not control — CRA looks to the underlying substance (whether the payment is a single settlement amount or a stream of periodic payments). The same rule applies to the recipient's side: a lump sum is not taxable income.

When are legal fees for a separation deductible?

Legal fees incurred to establish, enforce, or collect spousal or child support are deductible to the recipient on Line 22100 of the T1 return, even though child support itself is not taxable. Legal fees incurred by the payer to negotiate down or defend against support obligations are generally not deductible. Fees for property division, custody disputes, or the divorce itself are not deductible by either party.

How is the Canada Child Benefit split between separated parents?

In shared-custody arrangements (40-60% with each parent), each parent receives 50% of the CCB they would receive if they had full custody, calculated using each parent's individual income. Total household CCB after separation typically exceeds pre-separation household CCB because the formula uses individual rather than family income. Both parents must file Forms RC65 and RC66 with CRA confirming the shared-custody arrangement.

Can I claim the spousal credit if I am separated?

No. The spousal credit on Line 30300 is only available for a spouse or common-law partner you supported during the year. Once legal separation occurs (typically a 90-day separation), the spousal credit is no longer available — even if you continue to pay spousal support. The eligible dependant amount (formerly equivalent-to-spouse) may be available for a child you support if you are single and not living with a common-law partner.

Do support payments affect the Canada Child Benefit?

Spousal support received is included in net income, which can affect the recipient's CCB calculation (the CCB phases out at higher income). Child support received does not affect the recipient's net income because it is not taxable. Support paid is not deducted from net income for benefit calculations of the payer either — even though it is deductible for tax purposes — because most benefit calculations use a "net income before deductions" concept.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA