Section 84.1: The Anti-Surplus-Stripping Rule Owner-Managers Hit

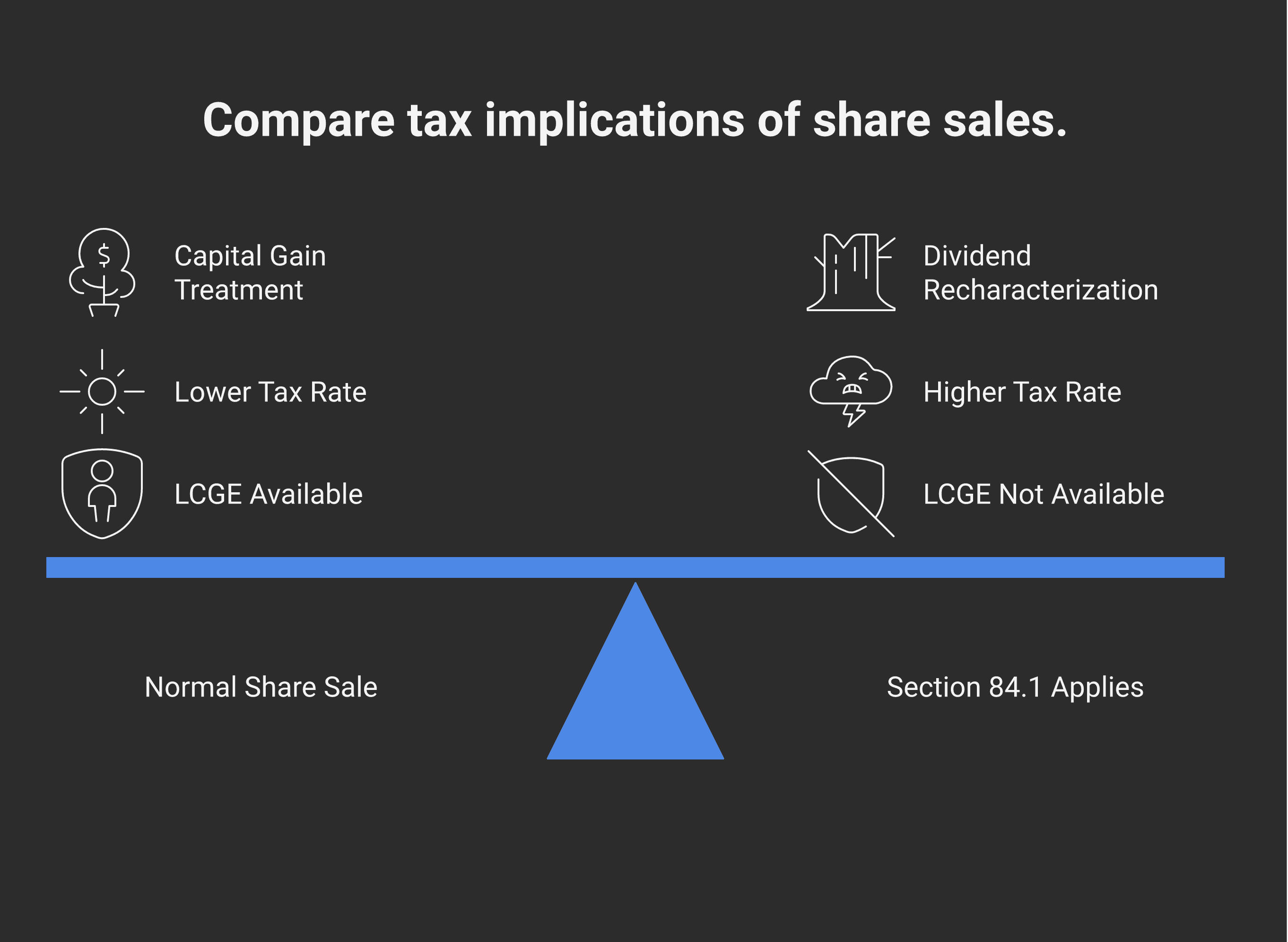

Section 84.1 of the Income Tax Act is the anti-avoidance rule every Canadian owner-manager eventually encounters, usually at the worst possible time — when planning an exit. It prevents what tax practitioners call "surplus stripping" — converting what would be a taxable dividend into a more lightly-taxed capital gain by selling shares to a non-arm's-length corporation. The mechanic is simple to describe but consequential in effect: if you trip section 84.1, your capital gain is recharacterised as a deemed dividend, you lose access to the LCGE, and your tax bill can jump by 20+ percentage points.

This guide walks through what section 84.1 does, the historic carve-out under Bill C-208 (2021), the tightened rules under Bill C-59 effective January 1, 2024, the pipeline-transaction implications post-mortem, and the typical owner-manager scenarios where the rule bites.

Key takeaways

Section 84.1 of the Income Tax Act treats a sale of shares to a non-arm's-length corporation as a deemed dividend rather than a capital gain — eliminating LCGE access and increasing the seller's tax burden.

The rule was designed to stop transactions where a parent "sells" company shares to their own holding corporation, converting accumulated corporate surplus into a more lightly-taxed capital gain. The carve-out for genuine intergenerational business transfers was introduced by Bill C-208 in 2021 and tightened by Bill C-59 effective January 1, 2024.

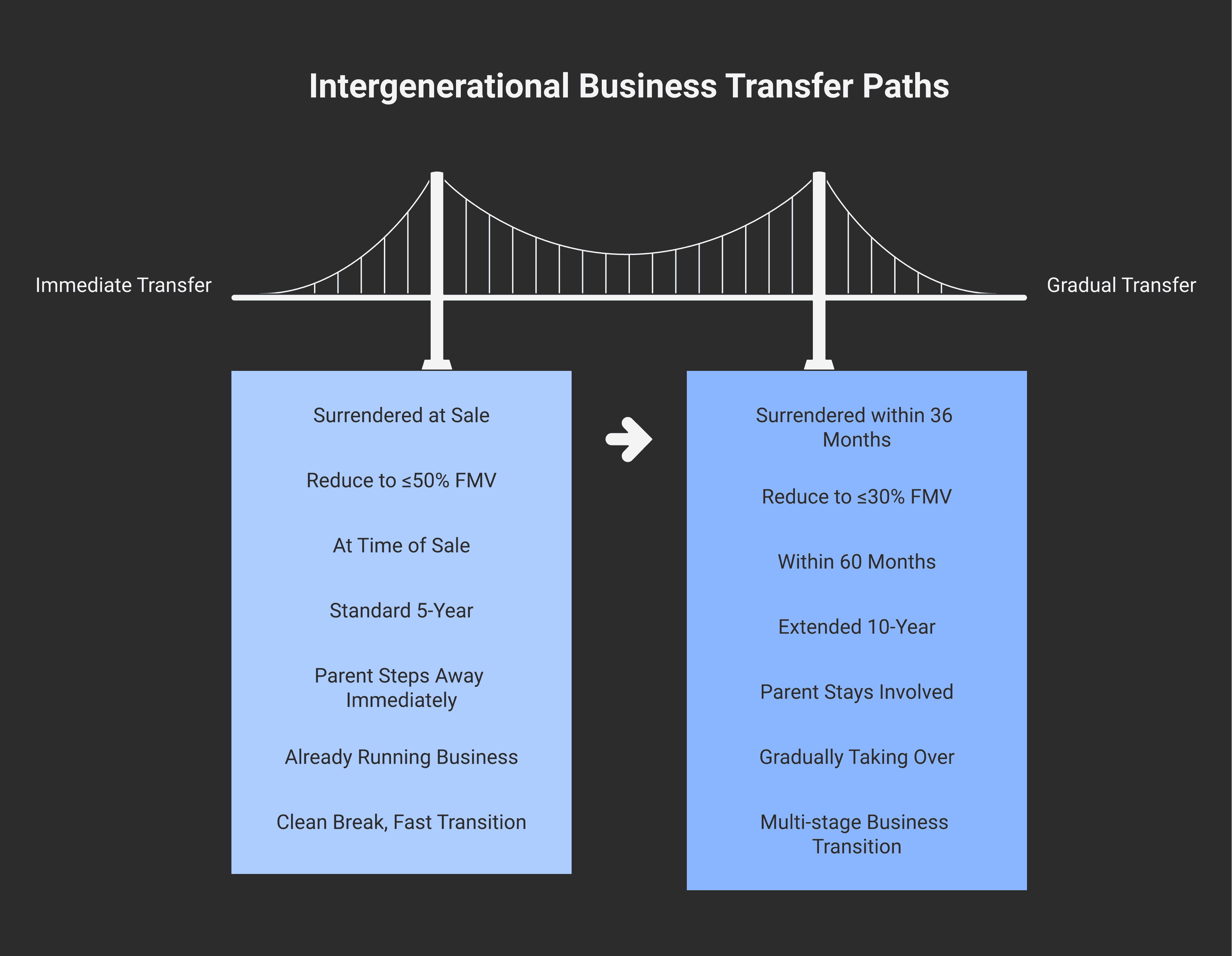

Under the 2024 amended rules, two paths qualify for the carve-out: the Immediate Transfer (3-year compliance window) and the Gradual Transfer (5-10 year window). Both require strict parent-control-surrender and adult-child-active-involvement conditions.

Pipeline transactions post-mortem — where an estate sells shares of a deceased's holdco to a new corporation owned by beneficiaries — interact with section 84.1 in technical ways. Estate planning must account for the rule, especially where the deceased used the LCGE before death.

Joint liability under Bill C-59: if CRA later determines that an intergenerational transfer was not genuine, both the parent and the child are jointly liable for the additional tax (capital gains treatment denied + section 84.1 deemed dividend applied).

What section 84.1 actually does

The mechanic in plain terms:

A taxpayer owns shares of Corp A (an operating company)

The taxpayer sells those shares to Corp B (typically a corporation they or a related person controls)

The transaction would naturally be a share sale generating a capital gain — taxed at 50% inclusion + (potentially) LCGE

Section 84.1 intervenes: it reduces the "paid-up capital" (PUC) of the shares received from Corp B by an amount tied to the difference between FMV and the lower of the seller's ACB and the original PUC

The seller is deemed to receive a dividend equal to the excess of the proceeds over the lower of the original ACB and the (now-reduced) PUC

The practical effect: instead of receiving capital gain treatment with LCGE access, the seller receives dividend treatment — taxed at full personal dividend rates (eligible or non-eligible depending on the source corporation's pool balances) with no LCGE access.

The tax differential is significant. For a top-bracket Ontario filer in 2026:

Capital gain with LCGE: substantially sheltered + 26.76% on excess

Non-eligible dividend: ~47.74% effective

A $5M sale that would have produced a capital gain (with LCGE) can become a $5M deemed dividend taxed at 45%+ — a tax differential of $1M-$1.5M.

Why section 84.1 exists

Without an anti-stripping rule, the abuse would be obvious. An owner accumulates corporate surplus over many years (paying corporate tax at the SBD rate of 9-12% combined). When ready to extract that surplus, instead of taking it as a dividend (paying 42-48% personal tax on top), the owner "sells" the company shares to their own holdco for cash equal to the corporate surplus. The structure produces:

Capital gain to the owner (50% inclusion, top combined ~26.76%, plus possibly LCGE shelter)

Holdco now owns the operating co with reduced PUC

The accumulated surplus has been converted from "dividend to come" into "capital gain already realised"

Section 84.1 was enacted to block this exact maneuver. The rule has been on the books since 1990s and has been amended multiple times.

The Bill C-208 carve-out (2021)

In June 2021, Bill C-208 introduced an intergenerational business transfer exception to section 84.1. The original Bill C-208:

Excepted from section 84.1 the sale of QSBC or FFFC shares to a corporation controlled by the seller's adult child or grandchild

Required the purchaser corporation to not dispose of the shares within 60 months

Was widely criticised as too loose — it could be used for non-genuine transfers (i.e., the child immediately receives back the shares from the holdco, or the parent retains effective control)

Bill C-208 came into force June 29, 2021. Transactions completed under the original rules between then and the 2024 tightening enjoyed a relatively permissive carve-out.

Bill C-59 amendments (effective January 1, 2024)

Bill C-59 (Fall Economic Statement Implementation Act, 2023) replaced the original Bill C-208 carve-out with a more structured regime effective January 1, 2024. The new rules split the carve-out into two structured paths:

Immediate Intergenerational Business Transfer

Condition | Requirement |

|---|---|

Eligible transferee | Adult child, grandchild, niece, nephew, grandniece, grandnephew |

Eligible property | QSBC or qualifying farm/fishing corporation shares |

Parent's control | Must surrender legal control immediately at the time of sale |

Parent's economic interest | Must not own 50% or more of any class of shares (other than non-voting preferred) immediately after the sale, and must dispose of the entire remaining balance of common/voting equity within 36 months |

Child's active involvement | Must be actively involved in the business at the time of sale |

Compliance window | All conditions met within 3 years |

Capital gains reserve | Standard 5-year reserve available |

Gradual Intergenerational Business Transfer

Condition | Requirement |

|---|---|

Eligible transferee | Same as Immediate |

Eligible property | Same as Immediate |

Parent's control | Must surrender legal control within 36 months |

Parent's economic interest | Must reduce to ≤30% of FMV within 10 years |

Child's active involvement | Must be actively involved within 60 months |

Compliance window | 5-10 years |

Capital gains reserve | Extended 10-year reserve available |

Both paths require joint election by the parent and the adult child purchaser corporation. The election is filed with the parent's tax return for the year of sale.

Joint liability. Both parent and child are jointly liable for the additional tax if CRA later determines that the transfer was not a genuine intergenerational business transfer (i.e., section 84.1 deemed dividend treatment retroactively applied).

Pipeline transactions post-mortem

A pipeline transaction is a common post-mortem strategy where an estate sells the deceased's shares of a holdco to a new corporation owned by the estate's beneficiaries — converting the embedded gain into a tax-efficient distribution chain.

The mechanic:

Deceased dies owning shares of Holdco A

Estate inherits the shares with FMV cost base (via subsection 70(5) deemed disposition at death)

Estate sells those shares to a new corporation (Newco) owned by the beneficiaries

Newco pays for the purchase via promissory note (or equivalent)

Holdco A wound up or merged with Newco; assets distributed to Newco

Newco repays the promissory note to the estate using the underlying assets

The result: the estate's cost-base equals the FMV at death (no gain to estate), and the underlying corporate assets flow up to the beneficiaries with no additional tax. Beneficiaries inherit the assets effectively net of the deceased's terminal-return tax bill.

Section 84.1 implications. Without specific drafting, the pipeline could be caught by section 84.1 — the estate's sale of shares to Newco (related party) could trigger deemed dividend treatment. The pipeline mechanic includes specific structuring (CRA-approved sequences and timing) to avoid the section 84.1 issue. CRA's administrative position (in technical interpretations) generally accepts the pipeline where:

There is no immediate distribution to beneficiaries (typically a 12-month delay between the share sale to Newco and the asset distribution)

The assets remain in the corporate structure for a reasonable period

The transaction follows specific documentation

For an inherited business situation, the pipeline is often the most tax-efficient path to extract corporate value — but the section 84.1 risk is real if the structure is rushed.

Common owner-manager scenarios

Scenario 1: Parent selling QSBC shares to a corporation owned by their adult child. The textbook intergenerational transfer. Bill C-208 / Bill C-59 carve-out applies if the conditions are met. Capital gains treatment preserved; LCGE accessible. Joint liability if CRA later challenges genuineness.

Scenario 2: Owner-manager selling operating co shares to their own holding company. Classic surplus-stripping target. Section 84.1 fully applies; no carve-out available. Capital gain recharacterised as deemed dividend.

Scenario 3: Owner sells operating co shares to a non-arm's-length brother's holding company. Section 84.1 applies (non-arm's-length corporation purchaser). No intergenerational transfer carve-out (sibling not eligible — only descendants and post-2024 nieces/nephews). Deemed dividend treatment.

Scenario 4: Pipeline transaction after parent's death. Beneficiary-owned Newco buys shares from estate; properly structured, section 84.1 does not bite. CRA accepts the mechanic where documentation and timing follow established practice.

Scenario 5: Parent gifts shares to adult child (no sale). Section 84.1 does not apply (no sale to a corporation). Section 69 may apply (deemed FMV proceeds). For most family situations, gifting is straightforward but doesn't access LCGE.

Scenario 6: Parent sells QSBC shares to a corporation owned by an adult niece who is actively involved in the business. Post-January 1, 2024, the niece qualifies as an eligible transferee under Bill C-59. Carve-out applies if conditions met. Pre-2024, niece transfer was not eligible.

Practical planning

Document the genuineness of the transfer. Bill C-59's joint-liability mechanic puts both parent and child on the hook if CRA determines the transfer was not genuine. Documentation matters — corporate minutes showing the child's active involvement, evidence of the parent's control surrender, evidence of arm's-length-equivalent purchase price.

Choose Immediate or Gradual based on operational reality. The Immediate Transfer (3-year window) suits situations where the child is already running the business and the parent is genuinely stepping away. The Gradual Transfer (10-year window with 10-year reserve) suits situations where the parent will be involved for several more years.

For pipeline transactions, follow established structure carefully. CRA's administrative position allows the pipeline but requires specific documentation and timing. Rushing the structure can trigger section 84.1.

Avoid surplus-stripping schemes that don't meet the carve-out. Various promoter schemes have proposed structures that claim to access capital gains treatment without meeting the genuine-transfer conditions. CRA has consistently challenged these — and the GAAR (General Anti-Avoidance Rule) under section 245 of the Income Tax Act provides a backstop even where the technical section 84.1 mechanics are escaped.

Coordinate with estate freeze timing. Many freeze transactions involve a section 85 rollover that itself doesn't trigger section 84.1 (different mechanic). But subsequent freeze refreezes or sales of frozen preferred shares can implicate section 84.1.

For Modern Axis client engagements on owner-manager exits, section 84.1 is the single most important provision to manage. Get it right and the family business transfers efficiently with LCGE access. Get it wrong and the tax bill can swing by 20+ percentage points.

Frequently asked questions

What is section 84.1 of the Income Tax Act?

Section 84.1 of the Income Tax Act is an anti-surplus-stripping rule that treats a sale of corporate shares to a non-arm's-length corporation as a deemed dividend rather than a capital gain. The rule prevents owners from converting accumulated corporate surplus into a more lightly-taxed capital gain by "selling" their shares to their own holdco. Without an exception, the seller's gain is recharacterised — eliminating LCGE access and resulting in a much higher personal tax bill.

What does it mean to "trip" section 84.1?

Tripping section 84.1 means the rule applies to recharacterise the seller's capital gain as a deemed dividend. The seller had expected to pay capital gains tax (50% inclusion + LCGE access if applicable); instead, the seller is taxed on the proceeds as a dividend (with the dividend gross-up and tax credit applying, but at the higher dividend marginal rate). The tax differential can be 20+ percentage points for top-bracket filers — converting a $1M gain from ~$268K of tax (with LCGE shelter) to potentially $477K (deemed dividend).

What is the Bill C-208 / Bill C-59 carve-out from section 84.1?

The intergenerational business transfer exception to section 84.1 allows a parent to sell QSBC or FFFC shares to a corporation controlled by their adult child (grandchild, or — post-January 1, 2024 — adult niece/nephew/grandniece/grandnephew) while still accessing capital gains treatment and the LCGE. Originally introduced by Bill C-208 in 2021 with relatively permissive conditions, the carve-out was tightened by Bill C-59 effective January 1, 2024 into two structured paths: an Immediate Transfer (3-year window) and a Gradual Transfer (5-10 year window) with specific parent-control-surrender and child-active-involvement conditions.

What's the difference between the Immediate and Gradual transfer paths?

The Immediate Transfer path requires the parent to surrender legal control at the time of sale, not own 50% or more of any class of shares (other than non-voting preferred) immediately after the sale and dispose of the entire remaining balance of common/voting equity within 36 months, and the adult child to be actively involved at the time of sale. All conditions met within 3 years; standard 5-year capital gains reserve applies. The Gradual Transfer path allows the parent to surrender control within 36 months, reduce economic interest to 30% or less within 10 years, and the child to be actively involved within 60 months. Extended 10-year capital gains reserve available.

What is a pipeline transaction and how does section 84.1 affect it?

A pipeline transaction is a post-mortem strategy where an estate sells the deceased's shares of a holdco to a new corporation owned by the estate's beneficiaries — converting the embedded gain into a tax-efficient distribution chain. The estate's cost base equals the FMV at death (deemed disposition under subsection 70(5)). Properly structured (typically with a 12+ month delay between the share sale and the asset distribution to beneficiaries), the pipeline avoids section 84.1's deemed dividend treatment. Rushed or improperly documented pipelines can trigger section 84.1.

What happens if CRA determines my intergenerational transfer wasn't genuine?

Both parent and child are jointly liable for the additional tax under Bill C-59. The transaction is retroactively recharacterised: section 84.1 deemed dividend treatment applies instead of capital gains treatment; the LCGE access is denied; and the seller's tax bill increases by the difference. This joint liability is one of the most important practical features of the 2024 amendments — both parties have an interest in ensuring the transfer is genuine.

Can I gift my company shares to my children to avoid section 84.1?

Yes, gifting (no sale, no proceeds) is not subject to section 84.1. However, section 69 of the Income Tax Act treats the gift as a deemed sale at FMV — so you still report a capital gain (50% inclusion at your marginal rate), with LCGE available if the shares are QSBC. Gifting doesn't access the Bill C-208 / Bill C-59 carve-out (which is for arm's-length-style sales). For many family situations, gifting is straightforward, but it doesn't generate the structure or future-cost-base benefits that a properly-structured sale to a child's holdco does.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA