RDTOH and ERDTOH: CCPC Investment Income Guide (2026)

The RDTOH (Refundable Dividend Tax on Hand) mechanic is one of the most opaque pieces of the Canadian corporate tax system — but understanding it is critical for any owner-manager whose CCPC holds investments. The system imposes a heavy corporate tax on passive investment income inside the CCPC (38.67% federal), but refunds part of that tax to the corporation when dividends are paid to shareholders. The mechanism preserves integration between corporate-level and personal-level taxation of investment income.

Since 2019, the RDTOH system has been split into two pools: Eligible RDTOH (ERDTOH) and Non-Eligible RDTOH (NERDTOH). Each pool is unlocked by different dividend types, with different consequences for owner-manager planning.

This guide walks through how RDTOH and ERDTOH actually work, the pre-2019 and post-2019 mechanics, the integration math, and the $50K passive income claw-back interaction with the small business deduction.

Key takeaways

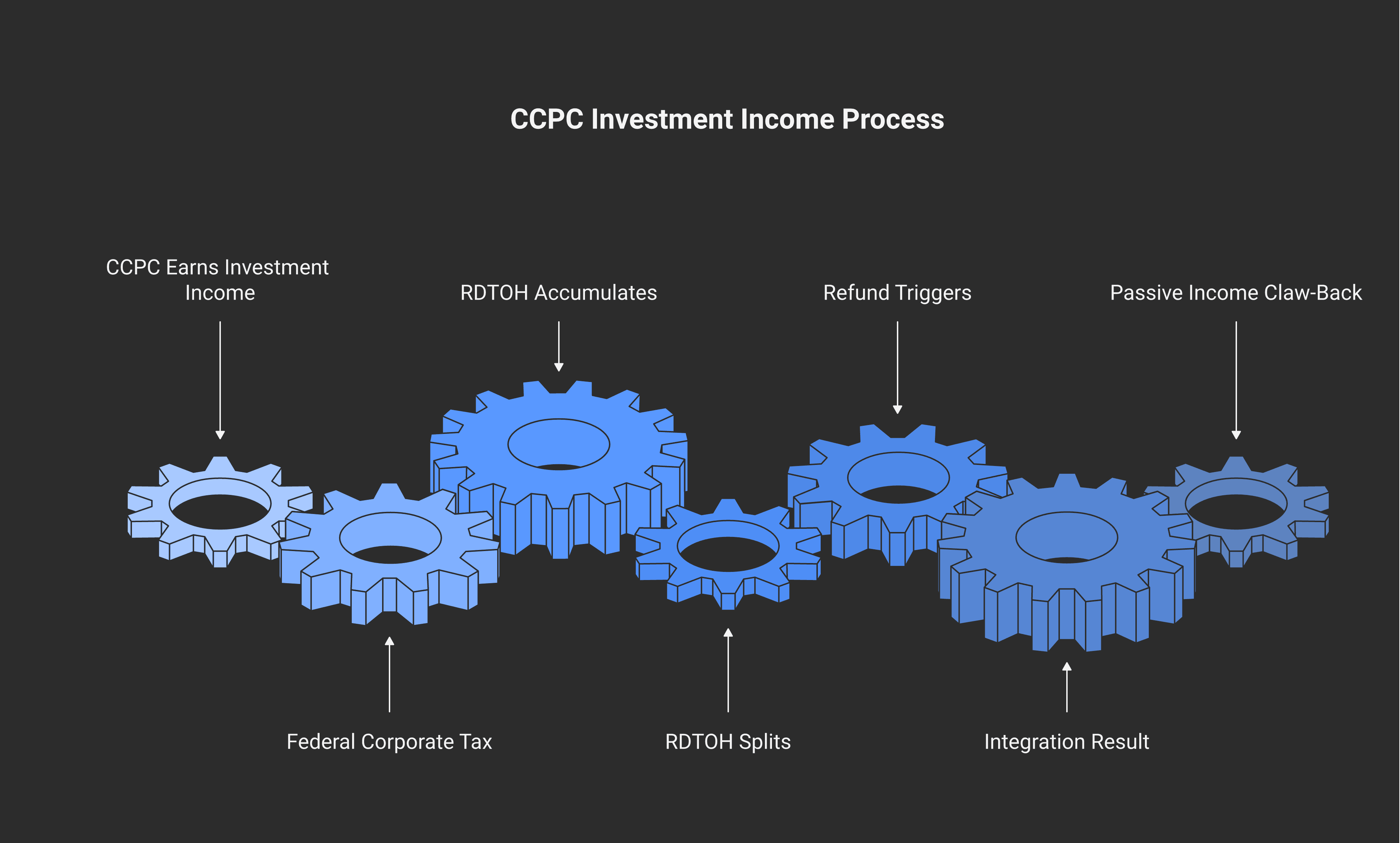

RDTOH (Refundable Dividend Tax on Hand) under section 129 of the Income Tax Act is a corporate-level account that tracks refundable tax paid on a CCPC's investment income. The refund triggers when the CCPC pays dividends to its shareholders — effectively spinning the corporate-level tax back out as the corporation distributes profits.

Investment income earned by a CCPC faces a federal rate of 38.67% (28% Part I + 10.67% Additional Refundable Tax under section 123.3 ITA). About 30.67% of that is refundable — added to the corporation's RDTOH.

Since 2019, RDTOH is split into two pools: Eligible RDTOH (ERDTOH) — refunded when eligible dividends are paid; Non-Eligible RDTOH (NERDTOH) — refunded when non-eligible dividends are paid. The split prevents owners from "stripping" refundable tax via dividend type choice.

The $1-of-dividend-paid-triggers-$0.38-of-refund rule means a CCPC must pay roughly $2.61 of dividend for every $1 of refundable tax it wants to recover.

The $50K passive income claw-back under subsection 125(5.1) — passive investment income above $50K in the prior year reduces the SBD limit. This rule interacts with RDTOH but operates separately.

Investment income inside a CCPC

A CCPC earning investment income (interest, dividends from non-connected payors, taxable capital gains, rental income that doesn't qualify as active business income) faces a high corporate-level tax rate. The federal portion:

28% Part I corporate tax (the federal general rate of 38% minus the 10% federal abatement, since investment income doesn't qualify for the SBD)

10.67% Additional Refundable Tax (ART) under section 123.3 of the Income Tax Act

Total federal: 38.67%

Plus provincial tax (~11-16% depending on province), the all-in corporate tax on investment income is roughly 50-55% — higher than even top personal marginal rates.

The RDTOH refund mechanism is what makes this rate tolerable. Of the 38.67% federal tax:

30.67% is refundable to the corporation (added to RDTOH)

8% is non-refundable (a permanent tax)

When the corporation eventually pays dividends to its shareholders, the refundable portion is paid back to the corporation at the rate of $1 of RDTOH refund for every $2.61 of taxable dividends paid.

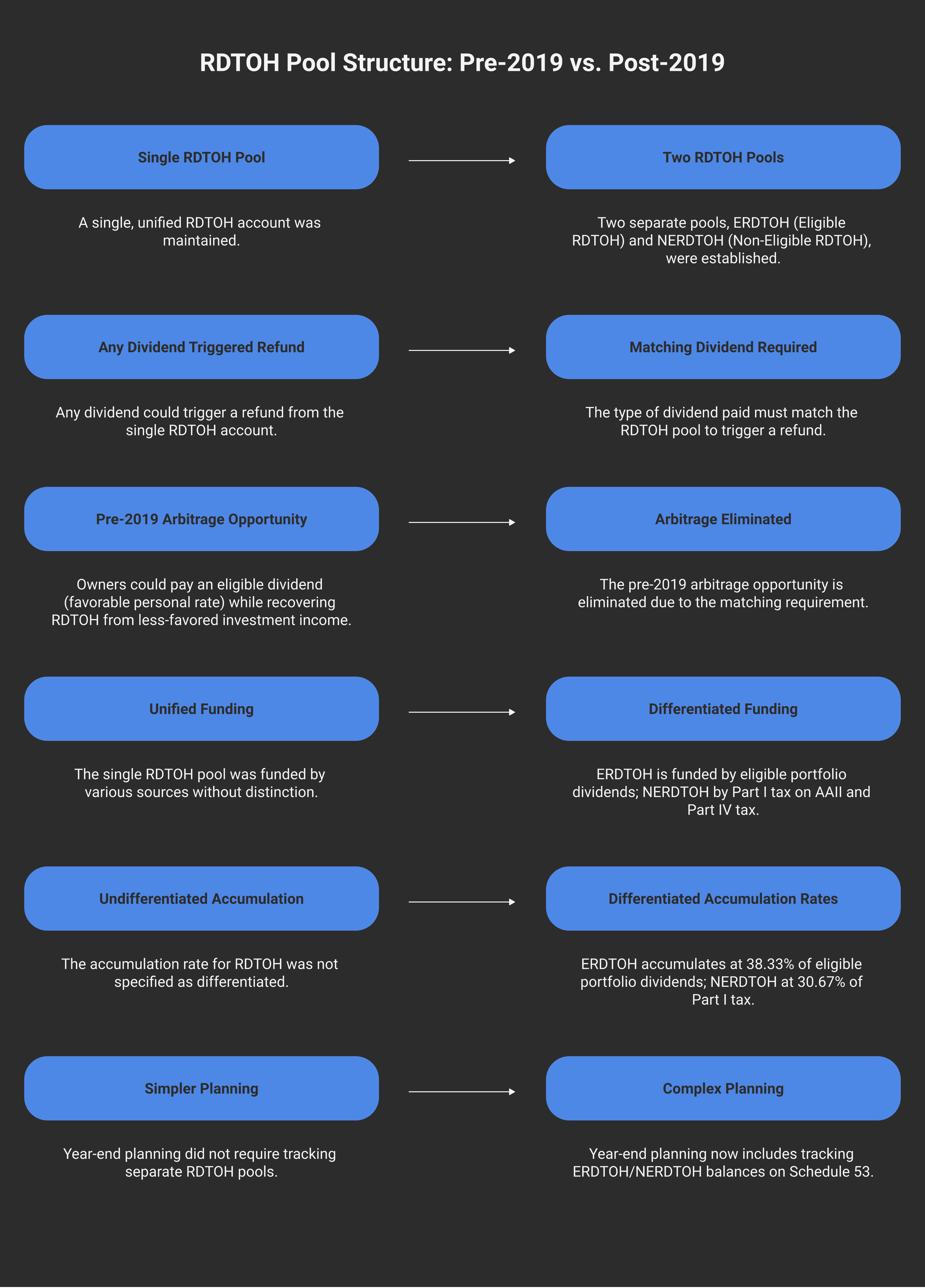

Pre-2019 mechanic — single RDTOH pool

Until 2019, RDTOH was a single pool. Any dividend the corporation paid (eligible or non-eligible) triggered a refund proportional to the RDTOH balance. This created an arbitrage opportunity:

A CCPC with substantial investment income would accumulate RDTOH. To recover the refund, it would pay an eligible dividend to its shareholder — which on the personal side enjoyed a smaller gross-up and a better DTC (more favourable than non-eligible). The shareholder paid less personal tax on the eligible dividend than they would have paid on a non-eligible dividend, while the corporation recovered the full RDTOH.

The 2019 RDTOH split was a Department of Finance response to this arbitrage.

Post-2019 mechanic — two pools

Effective for tax years starting after 2018, RDTOH was split into two pools under subsection 129(4) of the Income Tax Act:

Eligible RDTOH (ERDTOH)

Funded by: dividends received from non-connected Canadian corporations (essentially, portfolio dividends and dividends from public corporations)

Refunded when: the CCPC pays an eligible dividend to its shareholders

Rate of accumulation: 38.33% of the eligible portfolio dividend received

Non-Eligible RDTOH (NERDTOH)

Funded by: Part I tax on aggregate investment income (interest, capital gains, etc.) + Part IV tax on dividends from connected corporations

Refunded when: the CCPC pays a non-eligible dividend to its shareholders

Rate of accumulation: 30.67% of the Part I tax on AAII

The split forces the corporation to pay non-eligible dividends to access the NERDTOH refund, and eligible dividends to access the ERDTOH refund. This eliminates the pre-2019 arbitrage where a corporation could pay eligible dividends to recover refundable tax that came from less-favoured-treatment investment income.

The $50K passive income claw-back

The RDTOH system is separate from but interacts with the passive income claw-back under subsection 125(5.1) of the Income Tax Act.

The claw-back:

A CCPC with adjusted aggregate investment income (AAII) over $50,000 in the prior year has its small business deduction (SBD) limit reduced

For every $1 of AAII over $50,000, the $500,000 federal SBD limit is reduced by $5

AAII over $150,000 eliminates the SBD entirely

The interaction: RDTOH accumulates on investment income regardless of the claw-back. But the corporation's active business income loses the SBD-rate treatment (drops from 9% to 15% federal). The combined effect of high AAII inside a CCPC:

Investment income taxed at 38.67% federal, with 30.67% added to RDTOH

Active business income loses SBD, taxed at 15% federal instead of 9%

The "passive investment income trap" — where the CCPC's investment portfolio actively damages the corporation's active business tax position

For owner-managers with substantial investment portfolios, separating the investment portfolio into a separate holding company is often the optimal structure. The operating company maintains the SBD; the holdco holds the passive investments and pays its own corporate tax + RDTOH.

Integration intuition

The RDTOH system is designed to achieve integration: the total tax burden on investment income earned by a CCPC and paid out to a shareholder should approximate the personal tax on the same investment income earned directly.

A simplified illustration (Ontario, 2026, framework-level only):

$100 of interest income earned personally at top combined rate:

Combined federal + provincial top rate ≈ 53.5%

After-tax = $46.50

$100 of interest income earned in CCPC, then dividend paid to shareholder:

Corporate Part I tax + ART (38.67% federal) + provincial (~12%) = ~50.67% combined corporate tax → $49.33 stays in corp

ART portion (10.67%) is refundable → $10.67 added to RDTOH

CCPC pays a non-eligible dividend → triggers NERDTOH refund

$49.33 retained × dividend distribution → shareholder receives some, personal tax applies

After dividend gross-up + DTC: personal tax on non-eligible dividend ~47.74% (Ontario top)

After-tax in shareholder's hands ≈ $46-48 (approximately matches direct-income path)

The integration result is approximate — small under- or over-integration of 1-3% is common depending on province. The RDTOH refund mechanic is what makes the math work even close to neutral.

Year-end RDTOH management

For owner-manager CCPCs with investment income, year-end RDTOH management is a recurring exercise:

Track ERDTOH and NERDTOH balances separately. The corporation's ERDTOH and NERDTOH balances are reported in the refundable dividend tax on hand area on pages 6 and 7 of the T2 return itself, not on a separate schedule. Most accounting systems don't track them automatically; the year-end CPA review is when the corporation's RDTOH position becomes clear.

Plan dividend declarations to recover refundable tax. If the corporation has $50,000 of RDTOH and no plan to pay dividends, that's $50,000 of corporate tax sitting on the books unnecessarily. Annual dividend declarations sized to recover RDTOH are common.

Match dividend type to RDTOH type. Paying eligible dividends from GRIP refunds ERDTOH; paying non-eligible dividends from LRIP refunds NERDTOH. Cross-paying (eligible dividends not matched to ERDTOH) means the dividends are taxed at the favourable eligible rate but don't recover the right RDTOH pool.

Watch the AAII claw-back. If the corporation's prior-year AAII exceeded $50K, the SBD claw-back has already reduced the current year's SBD limit. Active business income above the reduced SBD limit is taxed at the general rate, regardless of dividend planning.

Consider the holdco structure for substantial investment portfolios. Separating investment income from active business income via a separate holding corporation often produces meaningfully better overall outcomes — the operating corp keeps its SBD, the holdco handles RDTOH on its investment income.

For Modern Axis client engagements on owner-manager CCPCs, year-end RDTOH analysis is a standard deliverable — including ERDTOH/NERDTOH balance projections, dividend strategy to optimize refunds, and AAII claw-back interaction.

Frequently asked questions

What is RDTOH (Refundable Dividend Tax on Hand)?

RDTOH is a corporate-level account under section 129 of the Income Tax Act that tracks refundable tax paid on a CCPC's investment income. The refund is triggered when the CCPC pays dividends to its shareholders. The mechanism preserves integration between corporate and personal taxation of investment income — without RDTOH, investment income earned in a CCPC would be double-taxed at the highest combined rate.

Why is RDTOH split into two pools since 2019?

The split (ERDTOH and NERDTOH) was a 2018 Department of Finance response to a pre-2019 arbitrage. Pre-2019, RDTOH was a single pool — any dividend triggered a refund. Owners would pay eligible dividends (more favourable personal-side treatment) while recovering RDTOH that came from less-favoured investment income. The 2019 split forces dividend type to match the RDTOH pool: eligible dividends trigger ERDTOH refunds; non-eligible dividends trigger NERDTOH refunds.

What is the rate of RDTOH accumulation on investment income?

For non-eligible RDTOH (NERDTOH), the accumulation rate is approximately 30.67% of the Part I tax paid on a CCPC's aggregate investment income (AAII). For eligible RDTOH (ERDTOH), the accumulation rate is 38.33% of eligible portfolio dividends received from non-connected Canadian corporations.

What dividend amount do I need to pay to fully recover my RDTOH?

The refund rate is approximately $1 of RDTOH refund for every $2.61 of taxable dividends paid. To recover $50,000 of RDTOH, the corporation must pay approximately $130,500 in matched dividends (either eligible or non-eligible depending on which RDTOH pool is being recovered).

How does the $50,000 passive income clawback interact with RDTOH?

The $50,000 AAII claw-back under subsection 125(5.1) reduces the corporation's small business deduction limit when prior-year AAII exceeds $50,000. RDTOH continues to accumulate on the investment income regardless. The combined effect is that high passive income causes both: (a) loss of SBD treatment on active business income, and (b) RDTOH accumulation that requires dividend distributions to recover.

What's the difference between ERDTOH and NERDTOH?

ERDTOH is the eligible portion — funded by eligible portfolio dividends received from non-connected Canadian corporations; refunded only when the CCPC pays eligible dividends to its shareholders. NERDTOH is the non-eligible portion — funded by Part I tax on aggregate investment income and Part IV tax on dividends from connected corporations; refunded only when the CCPC pays non-eligible dividends.

Should I move my investment portfolio to a separate holding company?

For substantial investment portfolios inside an operating CCPC, separating the investments into a separate holding company is often the right structural answer. The operating company maintains its SBD on active business income; the holdco handles the RDTOH on its investment income separately. The cost is one additional corporate structure to maintain. The benefit is preserving the SBD-rate treatment on active business income, which can save $40K-$80K per year of corporate tax for higher-income operations.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA