Private School Tuition as a Medical Expense in Canada

If your child has a learning disability, ADHD, anxiety, or another mental health condition and you're paying for a private school that specifically supports those needs, you may be sitting on one of the most overlooked credits in the Income Tax Act. Done properly, paragraph 118.2(2)(e) of the Income Tax Act can convert what looks like ordinary tuition into a medical expense that flows through your Canadian personal tax return.

Key takeaways

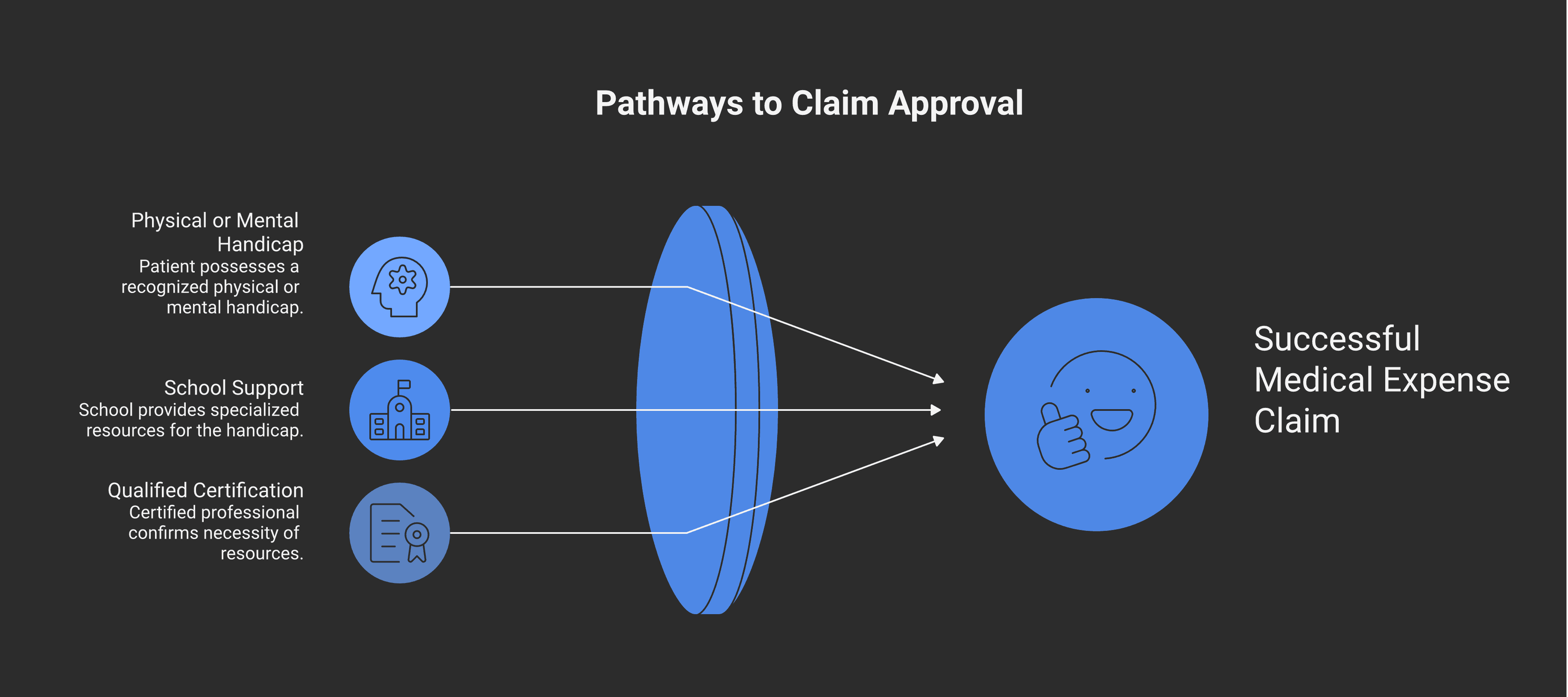

Private school tuition can be claimed as a medical expense in Canada under paragraph 118.2(2)(e) ITA — including the regular tuition portion — when three conjunctive conditions are met: handicap, school resources, and certification.

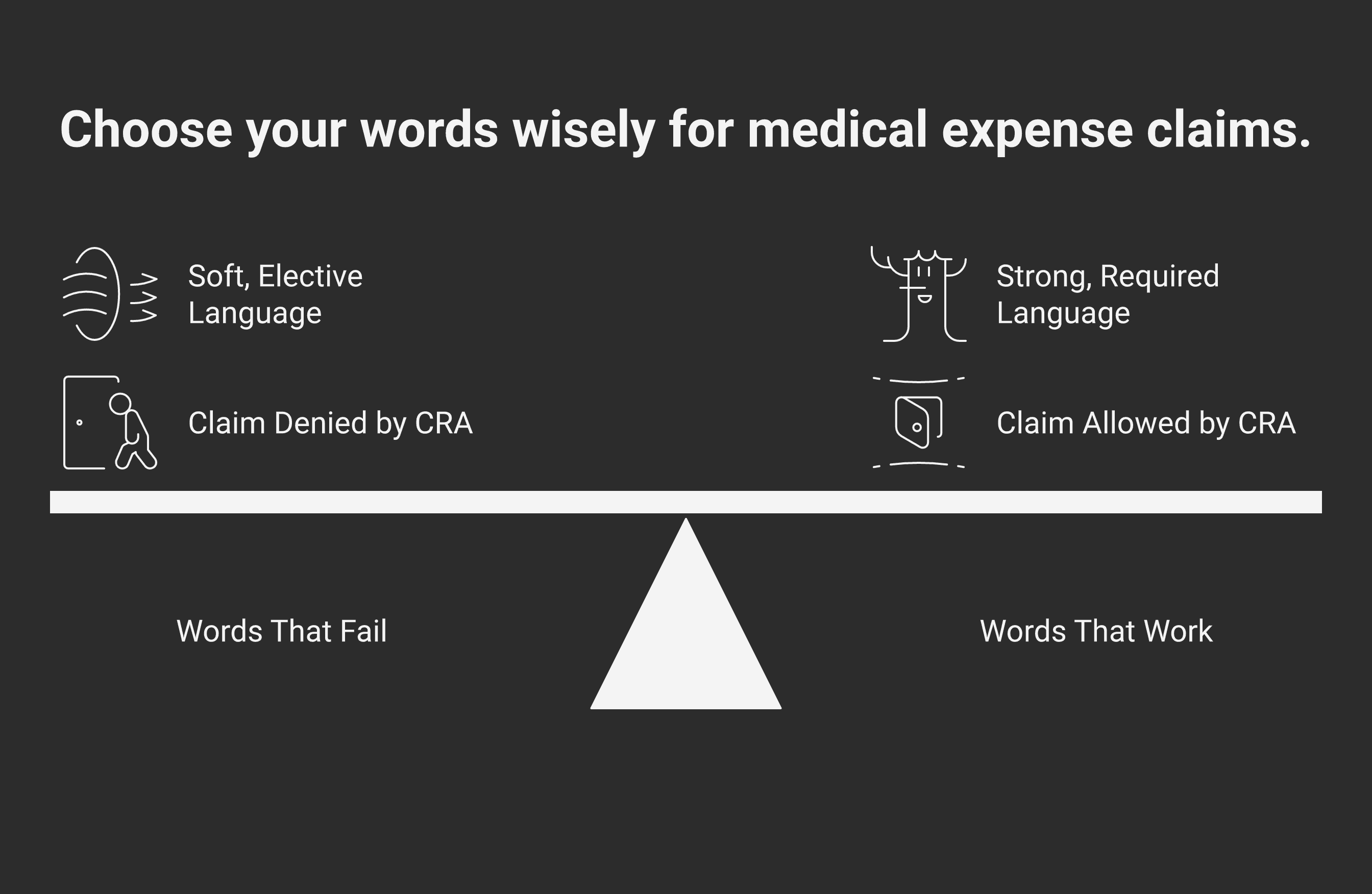

The single word "requires" decides almost every audit. Letters saying the child "would benefit from" the school usually fail; letters saying the child "requires" specialized resources because of a specific diagnosis usually win.

"Mental handicap" includes ADHD, learning disabilities, and anxiety disorders — confirmed in Karn v The Queen, 2013 TCC 92, the leading modern case on paragraph 118.2(2)(e).

The Disability Tax Credit is not a prerequisite; Income Tax Folio S1-F1-C1 paragraph 1.61 confirms the two tests are independent, and many children below the DTC threshold still qualify for this claim.

The catch is that the test is strict, the documentation has to be specific, and the CRA tends to look closely at these claims on audit. Most denials come down to a single word in the statute: requires. There's a meaningful difference between a school that benefits your child and a school your child needs, and that distinction is where claims live or die.

This post walks through the rule, the case law that built it, the documentation that survives audit, and a worked example showing what a successful claim actually looks like.

What the Income Tax Act actually says

Paragraph 118.2(2)(e) allows, as an eligible medical expense, amounts paid:

"for the care, or the care and training, at a school, an institution or another place of the patient, who has been certified in writing by an appropriately qualified person to be a person who, by reason of a physical or mental handicap, requires the equipment, facilities or personnel specially provided by that school, institution or other place for the care, or the care and training, of individuals suffering from the handicap suffered by the patient."

The CRA's administrative position is set out in Income Tax Folio S1-F1-C1, Medical Expense Tax Credit, at paragraphs 1.56 to 1.63. At paragraph 1.56, the folio breaks the rule into three conjunctive conditions that all have to be met:

The patient has a physical or mental handicap.

The patient requires the specialized equipment, facilities, or personnel of the school in question because of that handicap.

An appropriately qualified person has certified, in writing, that the handicap is the reason the patient requires those resources.

Miss any one of those and the claim fails. Hit all three with the right documentation, and the full fees paid to the school — including the part that looks like ordinary tuition — can qualify. That last point comes from Rannelli v MNR, 91 DTC 816 (TCC), which the CRA cites approvingly at paragraph 1.59 of the folio.

"Mental handicap" includes learning disabilities, ADHD, and anxiety

The statute uses the somewhat dated term "mental handicap." For years, the CRA tried to read that narrowly and exclude learning disabilities. The Tax Court rejected that reading in Karn v The Queen, 2013 TCC 92, the leading modern case on this provision.

In Karn, the taxpayer claimed the credit for tuition paid to a Calgary school for children with learning disabilities. The CRA disallowed it, arguing that "mental handicap" did not include learning disabilities. Justice Campbell disagreed and held that the term captures learning disabilities and related impairments. The diagnoses accepted in the case included anxiety disorder, ADHD, and other learning disabilities, all squarely within the scope of paragraph 118.2(2)(e).

Karn is also useful for what Justice Campbell said about the certification itself. The certification does not need to contain the literal phrase "physical or mental handicap." What matters is whether a reasonable person, reading the certifier's letter or report, would conclude that the qualified professional has identified a physical or mental handicap. Substance over form.

In practice, the diagnoses that come up most often in successful claims are dyslexia, dysgraphia, dyscalculia, ADHD (combined, inattentive, or hyperactive type), generalized anxiety disorder, autism spectrum disorder (level 1 in particular), and auditory or sensory processing disorders. A vague "learning difficulty" or "academic struggles" label is generally not enough.

The most important word in the statute: "requires"

Almost every claim that fails on audit fails on this point.

The Act says the patient must require the specialized resources of the school because of the handicap. The folio drives the point home at paragraph 1.59: where attendance is beneficial to the patient but not required, the cost will not qualify.

That distinction is hard to feel until you've seen it in a CRA review letter. A psychologist's report that says the child "would benefit from a small-class environment with individualized instruction" almost always reads as beneficial-only. A report that says the child "requires structured remediation and specifically trained personnel because of [diagnosis], and could not progress in a mainstream school setting" reads as required.

The difference between those two letters is the difference between a successful claim and a denied one. At Modern Axis, we often see otherwise excellent psychoeducational assessments fall short here because the certifying language was written for a school admissions file, not a tax file. Closing that gap usually takes a short follow-up letter from the same professional, written specifically for the tax record.

Who can certify

Subsection 118.4(2) of the Income Tax Act defines "medical practitioner" by reference to the jurisdiction where the service is rendered. For a child receiving services in British Columbia, that typically means a registered psychologist, a pediatrician, a psychiatrist, or a medical doctor — anyone authorized to practise in their field by the relevant BC college.

For paragraph 118.2(2)(e) specifically, the bar is actually a bit lower: the certifier needs to be an "appropriately qualified person." The folio confirms at paragraph 1.57 that this includes medical practitioners but can also include the principal of the school or the head of the institution. In practice, the strongest files combine both: a clinical assessment from a psychologist or physician identifying the diagnosis and the child's need for specialized resources, plus a school letter confirming that the school provides those resources.

What the school has to offer

The school does not have to limit its enrolment to children with disabilities. That point is explicit in the folio at paragraph 1.59. But the school does have to actually have the equipment, facilities, or personnel suited to the patient's specific handicap. Small class sizes alone are generally not enough.

Successful claims usually involve schools that can point to:

Specifically trained staff, often with credentials in special education, learning support, or clinical disciplines such as speech-language pathology or occupational therapy.

Structured remediation programs (Orton-Gillingham, Lindamood-Bell, ABA-informed, integrated speech-language or OT services).

Formal identification or accreditation as a school serving students with the diagnosed disability.

The Federal Court of Appeal made the converse point in Lister v Canada, 2006 FCA 331: a facility whose primary function is providing rental accommodation does not become a "school, institution or other place" within the meaning of paragraph 118.2(2)(e) just because it offers some incidental care services. The same logic applies to schools. A small private school with no specialized programming is unlikely to clear the bar, no matter how warm and supportive the environment.

How the credit actually works

For families that meet all three conditions, the medical expense credit runs through the standard Canadian framework:

Find the threshold. The threshold is the lesser of 3% of net income or the indexed annual cap. For the 2026 tax year, the cap is $2,890. The threshold is per claimant, not per family.

Subtract the threshold from the total medical expenses claimed. The amount above the threshold is what flows into the credit calculation.

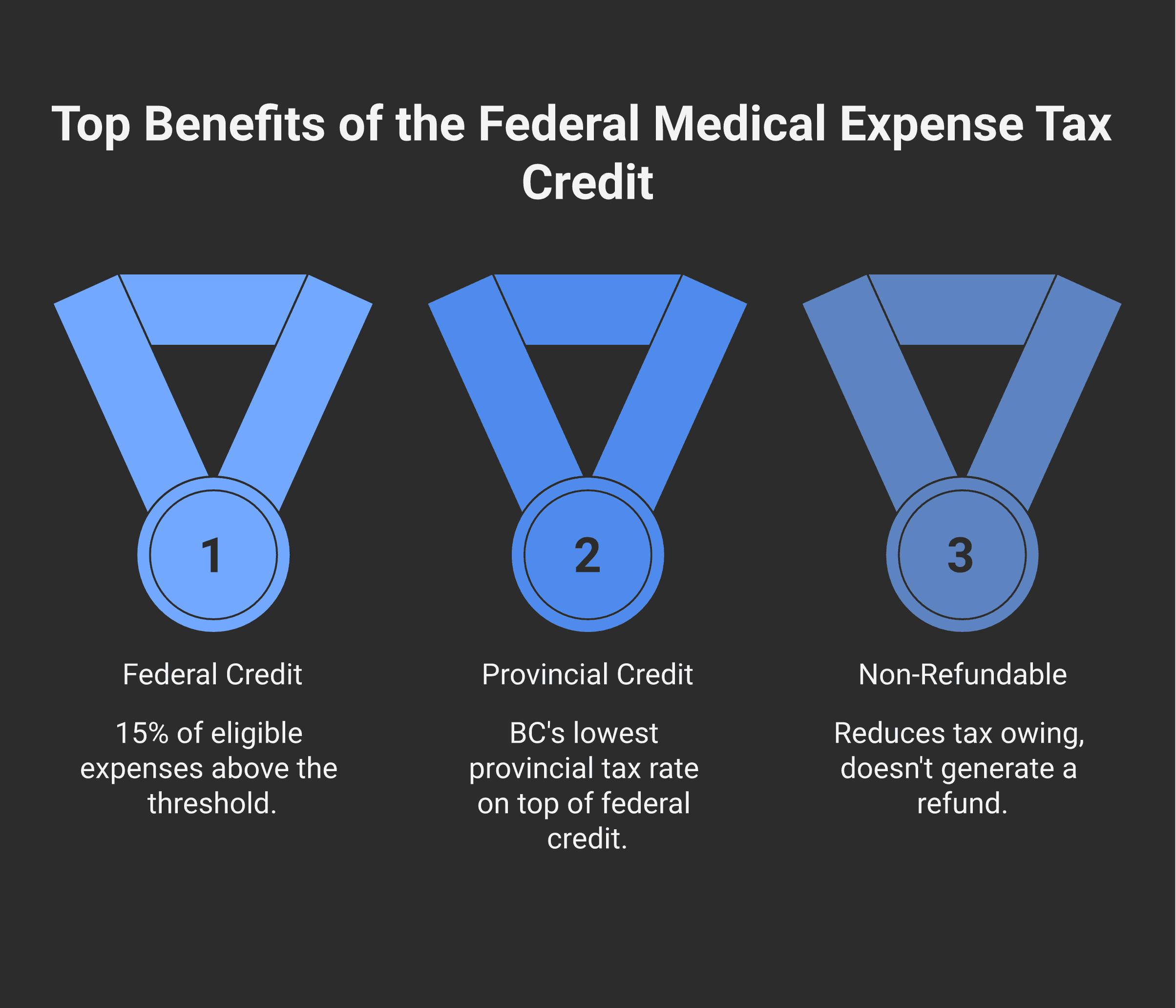

Apply the 15% federal rate to the amount over the threshold. That's the federal medical expense tax credit.

Add the provincial layer. In British Columbia, the provincial METC is calculated at BC's lowest provincial tax rate (5.60% for 2026) on a similar base above its own threshold, so the total credit is materially larger than the federal number alone.

A few practical points that matter when private-school tuition is the largest line on the medical-expense bill:

Medical expenses are usually best claimed on the lower-income spouse's return, because the threshold under paragraph 118.2(1)(c) is a percentage of net income. The lower the net income, the lower the threshold, and the more of the tuition crosses into eligible expense.

The 12-month period the family chooses for the claim is flexible — it doesn't have to align with the calendar year, as long as it ends in the tax year being filed.

The METC is non-refundable: it reduces tax owing, but a household with no tax owing doesn't see a benefit. For families incurring meaningful specialised-school tuition, there's almost always enough tax owing for the credit to offset.

Receipts must be kept on file. They aren't filed with the return, but the CRA requests them on a meaningful share of medical-expense claims, particularly where tuition is involved.

That's the framework. Whether a particular family's numbers translate into a meaningful credit depends on net income, total medical expenses for the year, and which spouse claims — that's the math you and your accountant work through together, with your own facts.

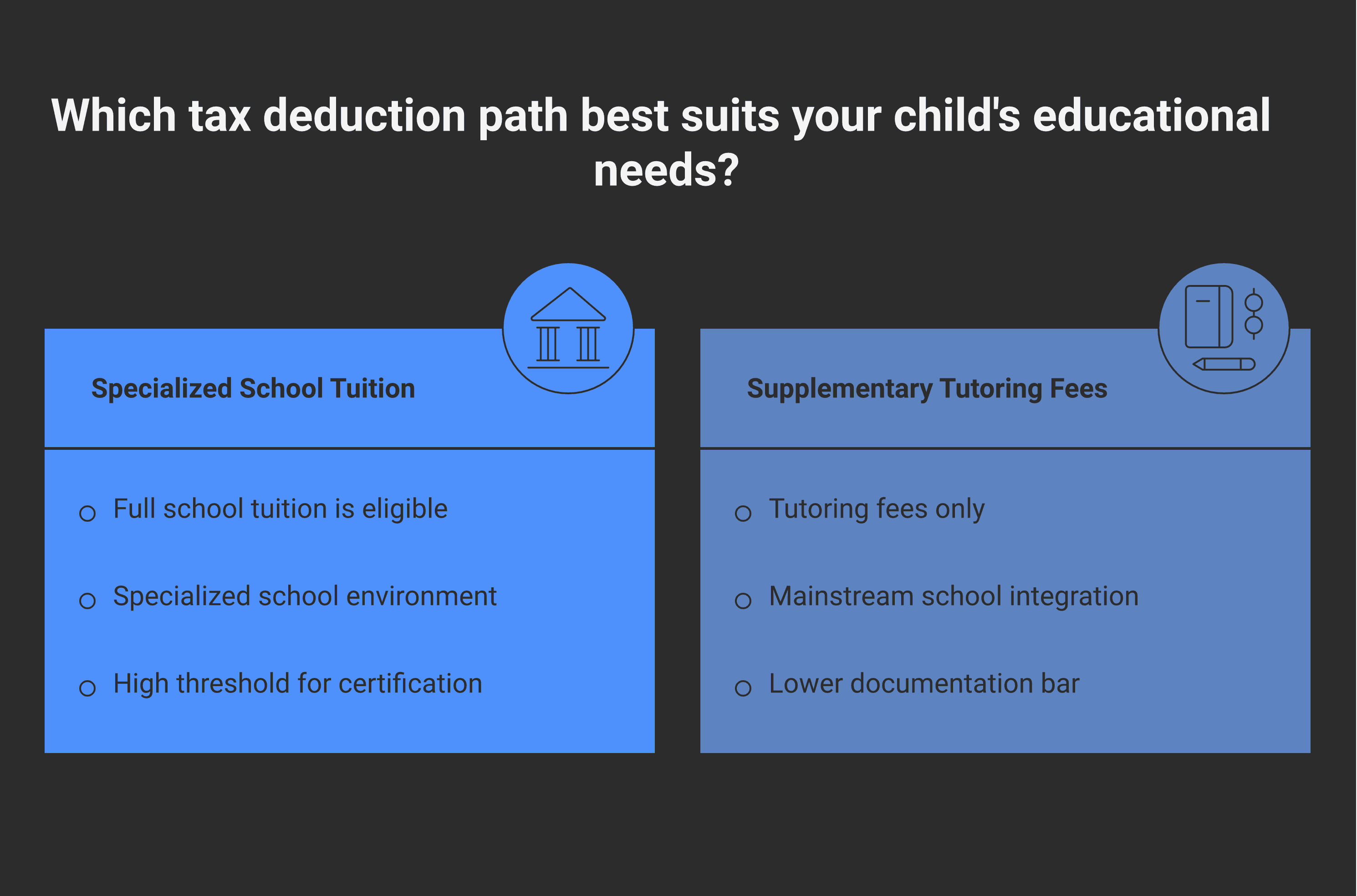

When to use the tutoring pathway instead

If the child attends a mainstream school but receives outside specialized tutoring because of a learning disability or mental impairment, paragraph 118.2(2)(l.91) is a separate route. It applies when:

The tutoring is supplementary to the patient's primary education.

The patient has a learning disability or a mental impairment.

A medical practitioner has certified, in writing, that the patient requires the tutoring because of that disability or impairment.

The tutor is ordinarily in the business of providing tutoring services to unrelated persons.

This avoids the more demanding "specially-provided school" test of paragraph 118.2(2)(e), but it only covers the tutoring fees, not full school tuition. The two pathways are mutually exclusive for the same expense, so a family with a child in a specialized private school typically goes the 118.2(2)(e) route, while a family with a child in a public school plus a private tutor goes the 118.2(2)(l.91) route.

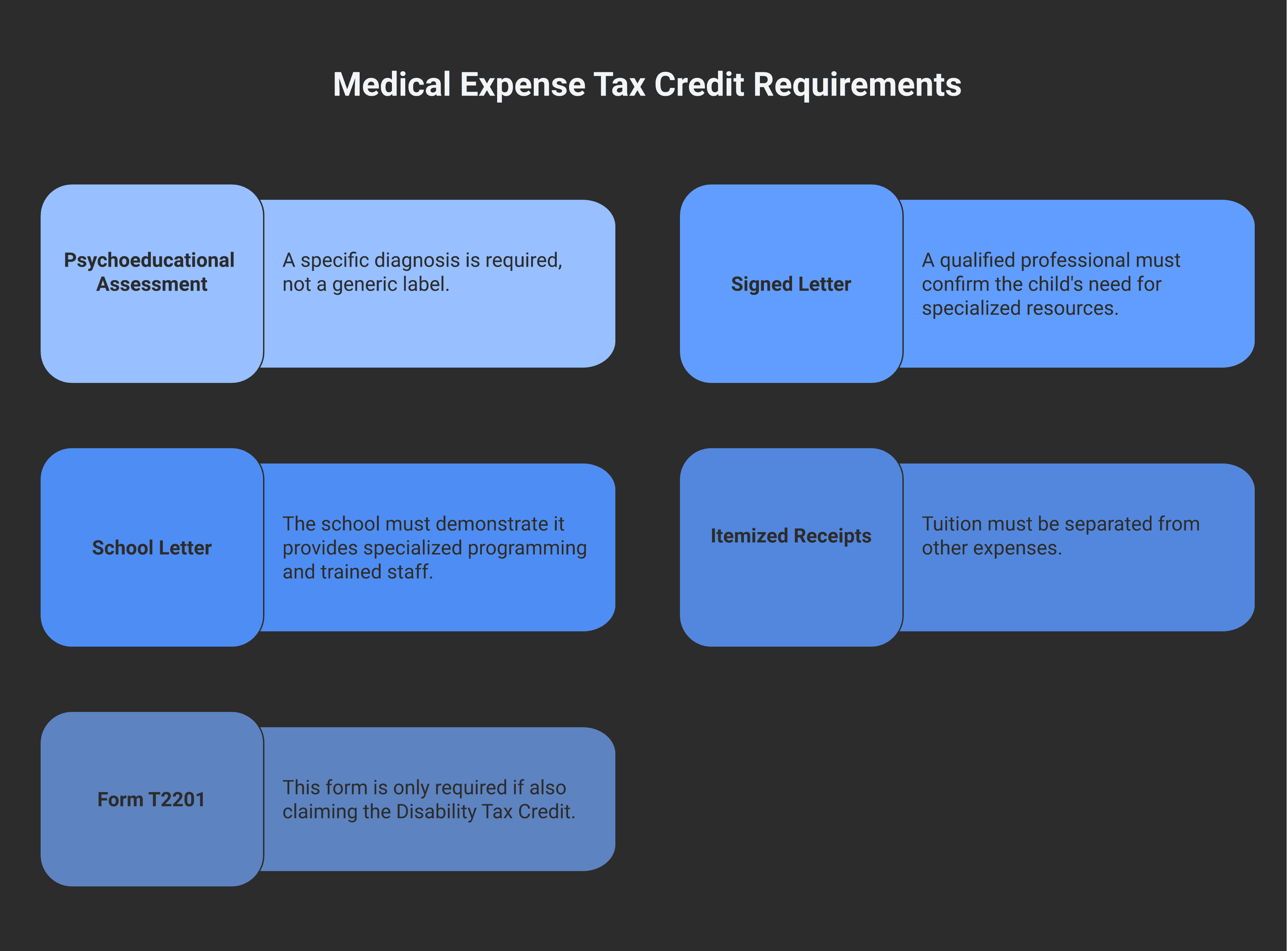

Documentation that survives audit

The CRA tends to ask for backup on these claims. The file should be assembled before filing, not drafted in response to an audit letter. A defensible file usually contains:

A current psychoeducational or medical assessment with a specific diagnosis (dyslexia, ADHD-combined, generalized anxiety disorder, ASD level 1, dysgraphia, auditory processing disorder, and so on). Specific names of conditions matter; "learning disability" alone is thin.

A signed letter from a qualified professional, typically the assessing psychologist, pediatrician, or psychiatrist, that names the diagnosis, states the child requires the specialized resources because of the diagnosis, identifies the school as a provider of those resources, and is dated before or during the relevant tax year.

A school letter or program description establishing what specialized programming, staff, and methodology the school actually provides.

Itemized receipts. Where fees include non-care items (lunch programs, optional after-school enrichment, transportation), those may need to be backed out. Per Folio paragraph 1.71, transportation costs to and from a qualifying school at the start and end of the school year may themselves be eligible under paragraph 118.2(2)(g) or (h), subject to the distance tests.

If a Disability Tax Credit certificate (Form T2201) is also on file, keep it with the medical expense package. Importantly, DTC approval is not a prerequisite for the 118.2(2)(e) claim. The two tests are independent, as confirmed at Folio paragraph 1.61. Many children with learning disabilities and moderate ADHD will not meet the DTC's marked-restriction threshold yet still qualify for the school-fee claim.

Common pitfalls

Beyond the beneficial-versus-required problem, the recurring traps look like this:

A "small private school" with strong pastoral care but no specialized programming. A warm environment is not the test.

A certifier letter that names the school but does not mention the diagnosis, or names the diagnosis but does not say the child requires the specialized resources.

Receipts that aggregate tuition with non-care items, with no breakdown.

Trying to claim both the 118.2(2)(e) school-fee pathway and the 118.2(2)(l.91) tutoring pathway on the same expense.

Claiming rental accommodation near a distant school as a medical expense. Folio paragraph 1.71 is explicit that this does not qualify, even where transportation does.

Working from memory at filing time, then trying to assemble documentation only when CRA's review letter arrives.

Bringing it together

Paragraph 118.2(2)(e) is one of the more powerful provisions in the medical expense rules, but it is also one of the more fact-specific. Whether a particular family's claim works comes down to the strength of the diagnosis, the language in the certifier's letter, the nature of the school, and the way the file is assembled before filing.

If you're paying private school fees because your child genuinely needs specialized programming for a diagnosed condition, the credit is worth getting right. The savings can be meaningful, but so are the consequences of a denied claim that takes years to unwind. Most of the work is upfront — getting the right letter, from the right professional, in the right form — and that work is much easier to do at the start of a school year than after a CRA review notice has landed.

If you'd like a second set of eyes on whether your situation supports a claim, or on the documentation you already have, that's exactly the kind of work our tax planning and compliance team does for clients in Victoria and across Canada. Reach out before filing, not after.

Frequently asked questions

Can private school tuition be claimed as a medical expense in Canada?

Yes. Paragraph 118.2(2)(e) of the Income Tax Act allows the full tuition — not just a special-services portion — to qualify as a medical expense when three conjunctive conditions are met: the child has a physical or mental handicap, the child requires the specialized equipment, facilities, or personnel of the school because of that handicap, and an appropriately qualified person certifies the connection in writing. CRA's administrative position is set out in Income Tax Folio S1-F1-C1, paragraphs 1.56 to 1.63.

Does my child need a Disability Tax Credit certificate to claim this?

No. The DTC and the paragraph 118.2(2)(e) school-fee claim are independent — confirmed at Income Tax Folio S1-F1-C1, paragraph 1.61. Many children with learning disabilities, ADHD, or anxiety will not meet the DTC's "marked restriction" threshold but still qualify for the school-fee claim because the legal test is different. Keep any T2201 you hold on file, but its absence is not a barrier to claiming private school tuition as a medical expense in Canada.

Does "mental handicap" include ADHD and learning disabilities?

Yes. The Tax Court confirmed in Karn v The Queen, 2013 TCC 92, that "mental handicap" under paragraph 118.2(2)(e) captures learning disabilities, ADHD, and anxiety disorders. Successful claims usually involve specific clinical diagnoses — dyslexia, dysgraphia, dyscalculia, ADHD (any subtype), generalized anxiety disorder, autism spectrum disorder level 1, and auditory or sensory processing disorders. Vague language like "learning difficulty" or "academic struggles" is generally not enough.

What is the difference between a school that "benefits" my child and one they "require"?

This single distinction sinks more claims than any other. Income Tax Folio S1-F1-C1, paragraph 1.59, is explicit: where attendance is beneficial but not required, the cost does not qualify. A psychologist's letter saying the child "would benefit from a small-class environment" reads as beneficial-only. A letter saying the child "requires structured remediation and specifically trained personnel because of [diagnosis], and could not progress in a mainstream setting" reads as required.

Who can certify my child for the medical expense school-fee claim?

For paragraph 118.2(2)(e) specifically, the certifier must be an "appropriately qualified person" — broader than the general "medical practitioner" definition in subsection 118.4(2) ITA. Income Tax Folio paragraph 1.57 confirms this includes registered psychologists, pediatricians, psychiatrists, medical doctors, and (for some elements) the principal or head of the school. The strongest files pair a clinical assessment from a clinician with a school-program letter confirming the school actually delivers the resources the child needs.

Which spouse should claim the medical expense in our family?

The lower-income spouse, almost always. Paragraph 118.2(1)(c) defines the threshold as the lesser of 3% of net income or the indexed annual cap ($2,890 for 2026). A lower net income means a lower threshold, which means more of the tuition crosses into the eligible amount. The 12-month medical expense period is also flexible — it doesn't have to align with the calendar year, as long as it ends in the tax year being filed.