How to Pay Corporate Tax to the CRA Through Plooto

When the time comes to pay corporate tax to the Canada Revenue Agency, it should be the easy part. You've done the hard work — the bookkeeping, the T2, the planning. Then you go to actually move the money, and you're squinting at online banking trying to remember whether this payment is a "corporation tax instalment" or a "balance owing," hoping you picked the right account and the right period.

It's a small thing that goes wrong surprisingly often. A missed instalment, a payment applied to the wrong account, a balance paid a few days late — each one quietly adds interest at a rate most owners would never accept on a loan.

So we've added a service: Modern Axis can now initiate your corporate tax payments — T2 instalments and balance-due amounts — through Plooto, with you approving every payment before a dollar leaves your account. Here's how corporations pay the CRA today, where the friction is, and how this fits in.

Key takeaways

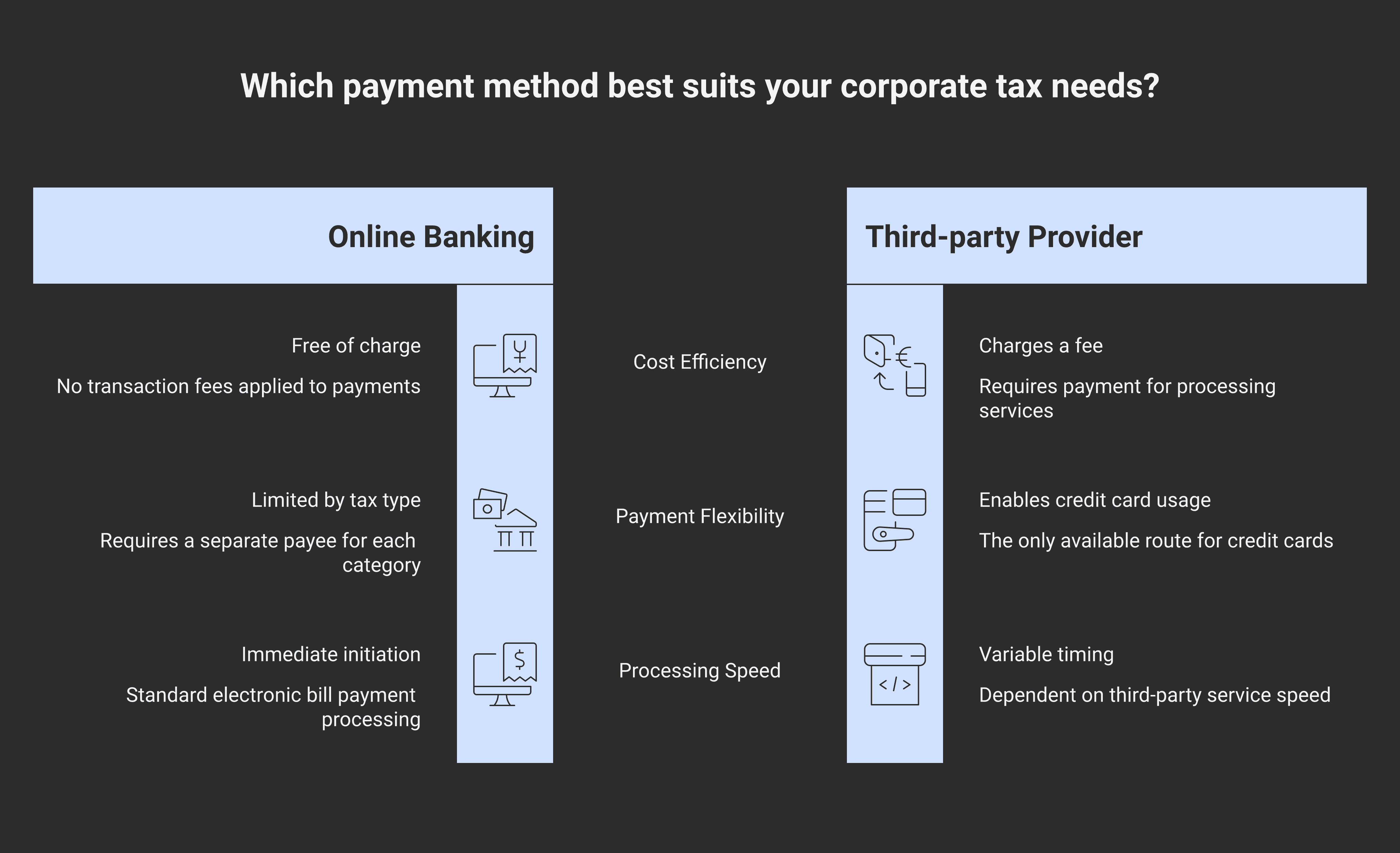

The CRA accepts no direct credit card payments for corporate tax — only debit, online banking, pre-authorized debit, wire (non-residents), or a third-party provider that charges a fee. That narrows your options more than most owners expect.

A corporation's balance of tax is due two months after year-end — or three months for a CCPC that claimed the small business deduction and meets the income test, under the "balance-due day" definition in subsection 248(1) of the Income Tax Act. Miss it and arrears interest compounds daily.

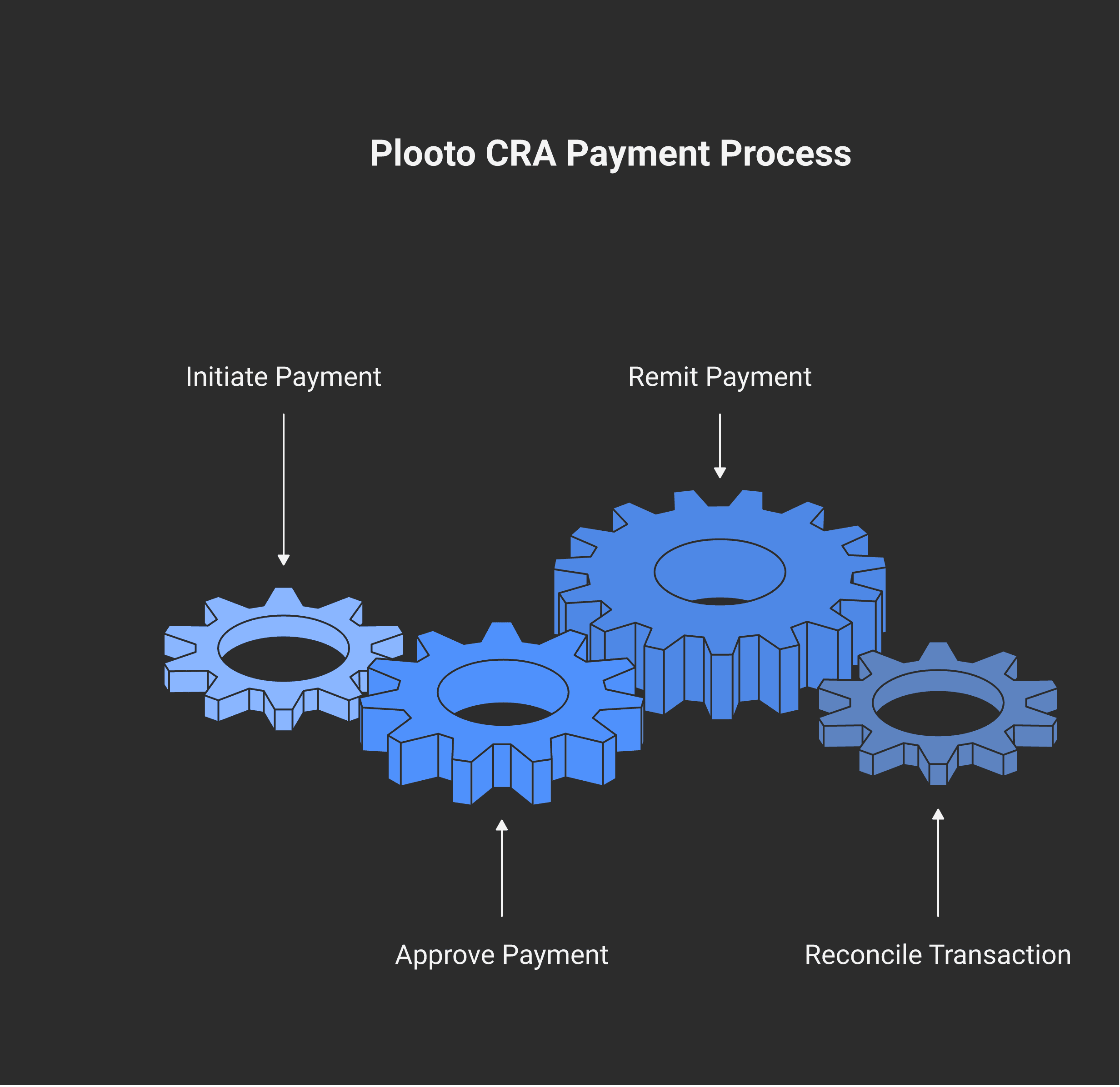

Plooto pays the CRA by electronic funds transfer for payroll source deductions, GST/HST, and T2 corporate income tax — with a flat fee per payment and an approval step before money moves.

The control mechanic is the point: a bookkeeper or our firm can initiate a payment, but it doesn't move until you approve it — and Plooto keeps a full audit trail and syncs back to QuickBooks or Xero.

It's not for everyone. A one-person corporation happy with online banking, or paying CRA twice a year, may be better served by free pre-authorized debit straight from My Business Account.

How corporations pay the CRA today

A corporation has roughly seven sanctioned ways to pay its T2 balance and instalments:

Online banking / bill payment through your financial institution (you add a CRA payee like "corporation tax — amount owing" or "corporation tax — instalment");

Pre-authorized debit (PAD) set up inside CRA My Business Account;

A debit card through CRA's My Payment service;

At a teller with a remittance voucher;

A mailed cheque;

A third-party service provider (this is the only way to use a credit card, and it charges a fee); or

Wire transfer (for non-residents without a Canadian bank account).

The friction is real once you look closely. The CRA does not accept credit cards directly — only through a fee-charging third party. My Payment takes Visa Debit and Debit Mastercard but no credit cards. PAD requires the first pull to be dated at least five business days out. And each CRA program — corporate income tax, payroll, GST/HST — is a separate payee with its own account number and reference fields, which is exactly where payments end up misapplied. None of this is hard, but it's fiddly, manual, and unforgiving of small mistakes.

The deadlines you're paying against

The reason precision matters is that interest on a late corporate payment is expensive and automatic.

Most corporations owe monthly instalments under section 157, each due on the last day of the month. A small CCPC that claimed the small business deduction, was a Canadian-controlled private corporation throughout the year, kept taxable income at $500,000 or less and taxable capital at $10 million or less, and has a clean 12-month compliance record can switch to quarterly instalments instead.

Then there's the balance-due day, defined in subsection 248(1): the remaining tax is due three months after year-end for a CCPC that claimed the small business deduction and meets the income test, and two months after year-end for everyone else. That two-versus-three-month split is the single most-missed corporate deadline we see.

Miss an instalment and you accrue instalment interest under subsection 161(2); if that interest tops $1,000, an instalment penalty under section 163.1 stacks on top. Leave the balance unpaid past the balance-due day and arrears interest runs under subsection 161(1) — at the prescribed rate, compounded daily. The prescribed rate is reset every quarter and sits at the three-month Treasury bill yield plus 4% on amounts you owe. It adds up faster than people expect, which is the whole argument for paying on time, every time. (For the full mechanics, see our guide to tax instalments in Canada.)

What Plooto is

Plooto is a payment-automation platform built for Canadian small businesses and the accounting firms that serve them. Its day job is accounts payable — paying suppliers by electronic funds transfer with proper approvals — but the feature that matters here is that it pays the CRA: payroll source deductions, GST/HST, and T2 corporate income tax.

The mechanics are straightforward. Plooto sits on top of your business bank account and remits to the CRA by electronic funds transfer for a flat fee of about $3 per payment, with a per-transaction maximum of $11,000 (a larger balance is split across multiple payments). One detail to plan around: the CRA treats the payment as made on the day it receives the funds, not the day Plooto initiates it — so payments are scheduled with lead time, never fired off on the due date itself.

The control mechanic: you approve before money moves

Here's why this works as a firm-managed service rather than handing over your banking login. Plooto separates initiating a payment from approving it. Our team (or your bookkeeper) can queue a CRA payment — correct program, correct period, correct amount — but it doesn't move until the designated approver signs off. You can set the rules: the owner always approves, or any two of a named group of approvers, or dual approval over a dollar threshold. Approvers get an email, log in, review the payment, and release it.

Two things fall out of that design. First, you keep control — nobody moves your money without your sign-off, which is the separation of duties every good controls environment wants. Second, Plooto keeps a complete record of who approved what and when, and syncs the paid transaction back to QuickBooks Online or Xero, marking the bill paid and reconciling it automatically. That audit trail is genuinely useful: the CRA expects you to keep books and records for six years under section 230, and a clean, time-stamped log of every tax payment is exactly the kind of documentation that makes a CRA review a non-event.

The new Modern Axis service

Putting it together: as part of our accounting and tax service, Modern Axis can now manage your corporate tax payments end to end. We track your instalment schedule and balance-due dates against your T2 filing, prepare each payment in Plooto with the correct CRA program and period, and send it to you for approval. You click approve; the money moves; it reconciles itself back into your books.

The point isn't the convenience for its own sake — it's that the most common, most avoidable corporate tax cost is interest on a payment that was late, misapplied, or forgotten. Taking that off your plate, while leaving the final approval in your hands, removes the failure point without removing your control.

What it costs and how onboarding works

Plooto charges a modest monthly subscription plus a per-transaction fee (the CRA payment fee noted above), with the plan tier scaling to your payment volume. Because fintech pricing and plan structures change, confirm the current Canadian figures and billing currency on Plooto's own pricing page rather than relying on a number here. Onboarding is a matter of connecting your bank account and your accounting software, setting your approver rules, and adding the CRA as a payee inside Plooto — something we handle as part of setting up your systems.

The one constraint worth flagging up front is the $11,000 per-transaction cap. For routine instalments it rarely matters; for a large year-end balance it means several payments (and several small fees and reconciliation lines) rather than one. We plan around it.

When Plooto isn't the right answer

We'd rather you skip a tool than pay for one you won't use. If you run a one-person corporation, pay the CRA two or three times a year, and are perfectly comfortable in online banking, a paid subscription plus a per-payment fee is hard to justify. Pre-authorized debit straight from My Business Account is free and handles scheduled, automatic CRA pulls perfectly well — you just don't get the approval workflow or the automatic reconciliation. And if your tax balances routinely run well into five or six figures, the per-transaction cap means more payments to manage. Plooto earns its place when you want a controlled, reconciled, never-missed payment process — not when "set up a PAD and forget it" already does the job.

If never missing a corporate tax deadline — and never wondering whether a payment landed in the right place — sounds worth a conversation, get in touch with Modern Axis. We'll tell you honestly whether the Plooto-managed service is a fit for your corporation or whether a free pre-authorized debit does everything you need.

Frequently asked questions

How do I pay corporate income tax to the CRA?

A corporation can pay its T2 instalments and balance through online banking or bill payment at a financial institution, pre-authorized debit set up in My Business Account, a debit card via CRA's My Payment service, at a teller with a remittance voucher, by cheque, through a third-party provider (the only credit-card route, for a fee), or by wire transfer for non-residents. The CRA does not accept credit cards directly.

Can I pay CRA corporate tax with a credit card?

Not directly. The CRA does not accept credit card payments through its own channels. The only way to use a credit card is through a third-party service provider, which charges a processing fee on top of your tax. Debit card payments are accepted through the CRA's My Payment service (Visa Debit and Debit Mastercard).

When is corporate tax due in Canada?

Most corporations pay monthly instalments during the year under section 157, with the balance of tax due on the "balance-due day" — three months after year-end for a CCPC that claimed the small business deduction and meets the income test, and two months after year-end for other corporations. Small eligible CCPCs may pay instalments quarterly instead of monthly.

Does Plooto let you pay the CRA?

Yes. Plooto can remit payroll source deductions, GST/HST, and T2 corporate income tax to the CRA by electronic funds transfer, for a flat fee per payment with a per-transaction maximum. Payments require approval before funds move, and the paid transaction syncs back to QuickBooks Online or Xero for reconciliation.

Is it safe to let my accountant pay my taxes through Plooto?

Plooto separates initiating a payment from approving it. Your accountant or bookkeeper can prepare the payment, but it doesn't move until the designated approver — typically the owner — signs off. You can require dual approval or owner-only approval, and Plooto keeps a full audit trail of who approved each payment, so you keep control of your money.

What happens if I pay my corporate tax late?

Arrears interest accrues under subsection 161(1) at the prescribed rate, compounded daily, on any balance unpaid after the balance-due day. Late or short instalments draw instalment interest under subsection 161(2), and if that interest exceeds $1,000, an additional instalment penalty applies under section 163.1. The prescribed rate resets quarterly and is set above market, so late payments are costly.

This article is for general information only and does not constitute professional tax, accounting, or product advice, and is not sponsored by or affiliated with Plooto. Software features, fees, and limits change over time, so confirm current details with the provider. Every corporation's situation is different, and a blog post can't account for yours. Speak with a qualified tax professional about your corporate tax obligations and the right way to meet them.

Alex Ataman, CPA

Founder

Modern Axis CPA