Notice of Objection: How Corporations Dispute the CRA

A notice of reassessment lands, the number is wrong, and you have a decision to make. You can pay it and move on, or you can fight it — and the formal way a corporation fights a CRA assessment is the Notice of Objection.

It's a real process with real rules, not a polite letter you dash off. There's a hard deadline, a prescribed way to file, an independent review by a different part of CRA, and — for corporations specifically — a few traps that catch owners off guard, including one about collection that can cost you cash even while you're winning the argument.

Here's how the Notice of Objection works for a Canadian corporation, what the large-corporation rules add on top, and what happens if CRA's Appeals area still doesn't see it your way.

Key takeaways

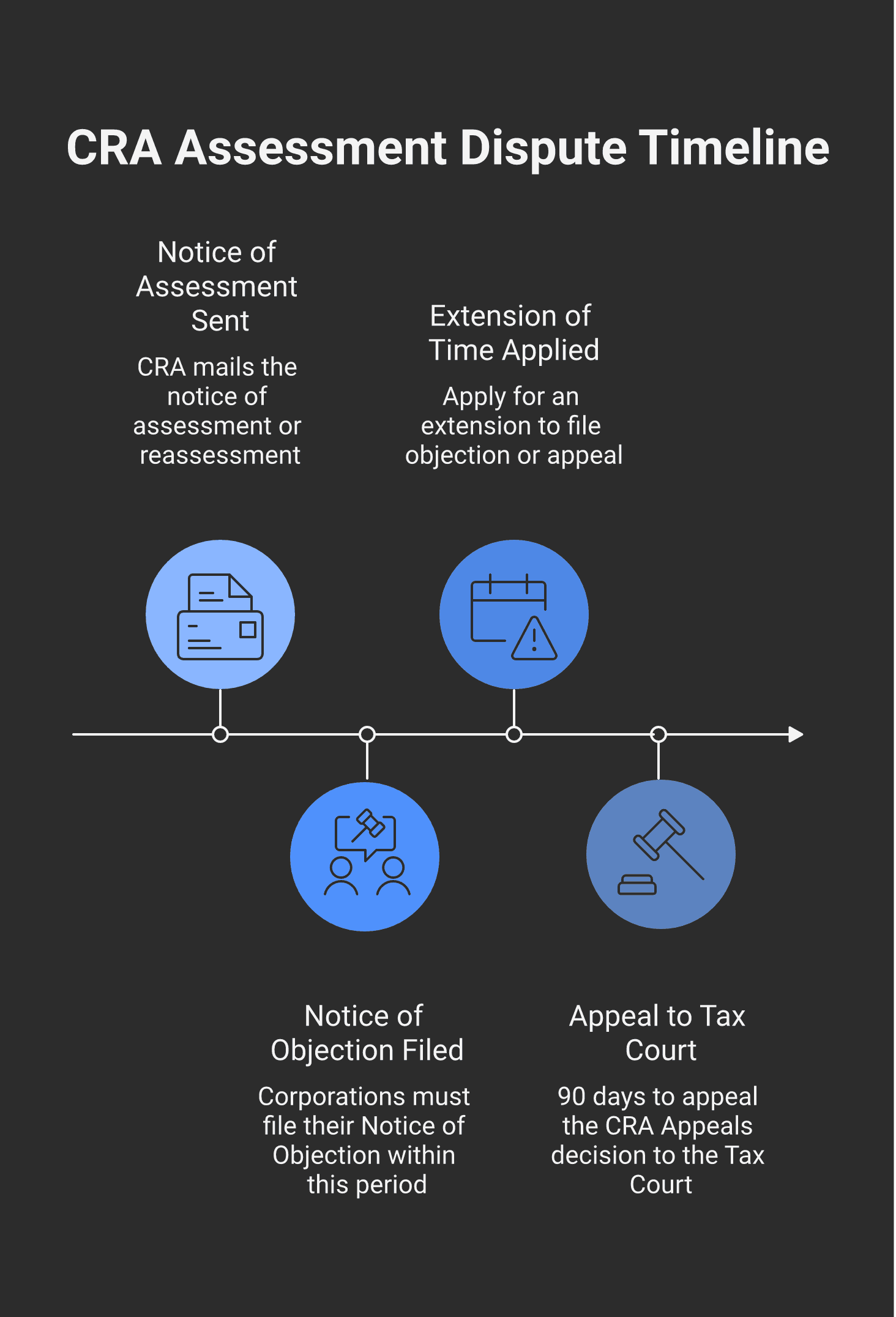

A corporation has 90 days from the date the notice of (re)assessment was sent to file a Notice of Objection under subsection 165(1) of the Income Tax Act. Individuals get a more generous "later of" deadline; corporations do not.

The objection goes to CRA's Appeals area, which reviews the file independently of the auditor who made the assessment — a genuine second look, not a rubber stamp.

"Large corporations" (taxable capital over $10 million, grouped with related corporations) face extra rules: they must spell out every issue, the relief sought, and the facts in the objection itself, and CRA can collect 50% of the disputed amount immediately under subsection 225.1(7).

Objecting pauses CRA collection on disputed income tax — but not on payroll source deductions or GST/HST, and arrears interest keeps compounding daily the whole time under section 161.

If Appeals confirms the assessment, you have 90 days to appeal to the Tax Court of Canada under section 169, where the informal procedure is available for disputes of $25,000 or less in tax and penalties per year.

What a Notice of Objection actually is

A Notice of Objection is the formal, statutory step that says: I disagree with this assessment, and here's why. It's governed by section 165 of the Income Tax Act, and filing one does something important — it moves your file out of the audit function and into CRA's Appeals area.

That hand-off matters. The appeals officer who reviews your objection is administratively separate from the auditor who raised the reassessment. CRA's mandate for Appeals is an impartial, complete review of the file. In practice, a lot of disputes resolve here, without ever going near a courtroom, because a fresh set of eyes looks at the law and the facts you put forward. The objection is your chance to make the full argument — with documents — that maybe never got heard during a correspondence audit.

This is also why the proposal-letter stage of an audit matters so much: if you couldn't resolve it with the auditor, the objection is the next, more formal venue to try.

The 90-day deadline — and it's stricter for corporations

For a corporation, the rule is short and unforgiving: you have 90 days from the day the notice of assessment or reassessment was sent to file your objection, under paragraph 165(1)(b).

Individuals and graduated rate estates get a softer deadline — the later of one year after their filing-due date or 90 days after the notice was sent (paragraph 165(1)(a)). Corporations don't get that cushion. Ninety days from the date on the notice, full stop. Calendar it the day the reassessment arrives, and build in a buffer; the date that counts is when CRA sent the notice, not when you opened it.

How a corporation files an objection

There are three accepted ways to file:

Form T400A, the prescribed Notice of Objection form;

Online through My Business Account, using the "Register my formal dispute (notice of objection)" service — the cleanest route for most corporations; or

A signed letter to the Chief of Appeals at your tax centre.

Whichever route you choose, the objection has to do more than register displeasure. State clearly which assessment and which tax year you're objecting to, explain why you disagree, and attach the relevant facts and supporting documents. A well-built objection reads like a brief: here's the issue, here's the law, here's the evidence. The more complete it is, the better your odds of resolving it at Appeals instead of court.

Missed the deadline? You may still have a window

If the 90 days slip past, the door isn't necessarily shut — but the path narrows fast. You can apply for an extension of time:

First, to CRA, under section 166.1. The application has to be made within one year after the original objection deadline expired, and you have to show you genuinely intended to object, had a real reason you couldn't, and applied as soon as you could.

If CRA refuses (or sits on it for 90 days), to the Tax Court of Canada, under section 166.2, on the same conditions.

The hard outer wall is one year after the original 90-day deadline. Past that, the assessment is final and there is no route back. Extensions are granted on genuine inability to act, not on "I forgot" — so the practical lesson is to treat the 90 days as the only deadline that exists.

The large-corporation rule

If your corporation is a "large corporation," the objection rules get stricter. A corporation is "large" for a year when its taxable capital employed in Canada — aggregated with related corporations — is more than $10 million at year-end (the same Part I.3 threshold defined in subsection 225.1(8)). Note the aggregation: a modest company can be caught because the related-corporation group clears $10 million together.

Two consequences follow, both under subsection 165(1.11):

You must nail down the objection up front. A large corporation has to reasonably describe each issue, specify the relief sought as a dollar change in a balance, and give the facts and reasons for each issue. Boilerplate "we object to everything" language won't fly.

You're locked in for the appeal. If the dispute later goes to the Tax Court, a large corporation can't raise new issues or ask for more relief than it set out in the objection. Whatever you didn't specify, you've generally lost the right to argue.

For large corporations, the objection isn't a placeholder — it's the document that defines the entire dispute, all the way through the courts.

Can CRA still collect while you object?

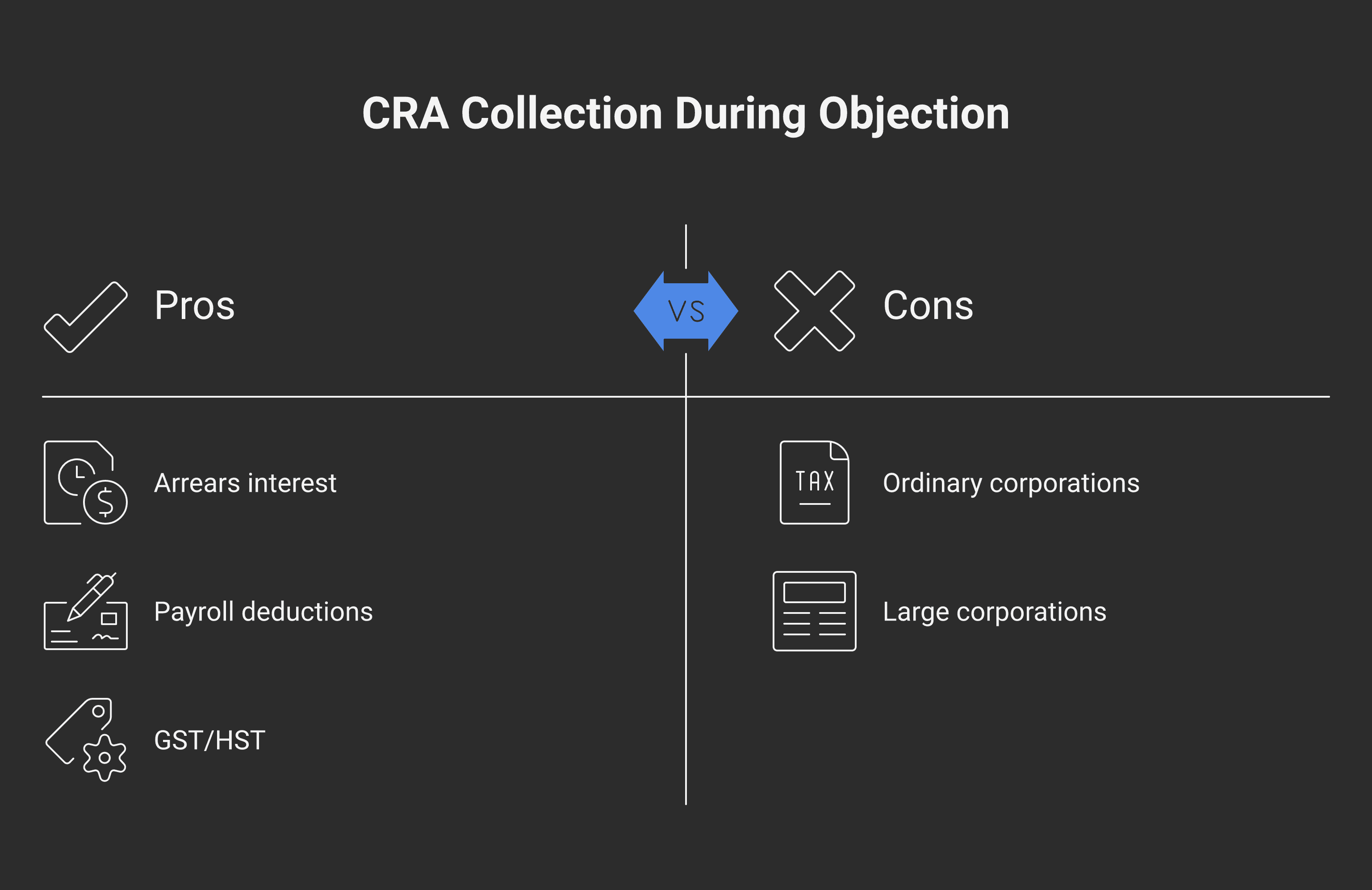

This is the wrinkle that surprises corporate clients most. For ordinary corporations, objecting to an income tax assessment generally pauses CRA's collection action on the disputed amount under subsection 225.1(1) — CRA can't garnish or seize disputed income tax while the objection or appeal is alive. Good news, but with three sharp exceptions:

Large corporations don't get the full hold. Under subsection 225.1(7), CRA can collect 50% of the disputed amount immediately, plus 100% of anything not in dispute.

Payroll source deductions are never protected by the income-tax hold (subsection 225.1(6)). CRA can pursue unremitted source deductions regardless of any objection.

GST/HST lives under the Excise Tax Act, which has no equivalent collection hold. CRA can keep collecting disputed GST/HST and can even offset credits and refunds against the debt.

Interest keeps running the entire time

A collection pause is not an interest holiday. While you object, arrears interest under section 161 keeps accruing at the prescribed rate on any unpaid balance — and it's compounded daily (subsection 248(11)). The prescribed rate is reset every quarter under Regulation 4301: it's the average yield on three-month Government of Canada Treasury bills, rounded up, plus 4% on amounts you owe the Receiver General.

Run the math on a multi-year dispute and the interest can rival the tax. That creates a real strategic choice: if you're genuinely unsure of your position, you can pay the disputed amount (or post acceptable security) to stop the interest clock while you fight. Win, and CRA refunds it with its own refund interest; lose, and you've avoided years of daily-compounded arrears interest piling on top. The same interest mechanics drive corporate tax instalments, and the logic is identical — interest at the prescribed rate is expensive money.

If Appeals doesn't agree — the Tax Court of Canada

If CRA's Appeals area confirms or varies the assessment and you still disagree, the next step is the Tax Court of Canada under section 169. You have 90 days from the date CRA sends its confirmation or reassessment to file your appeal. And if Appeals simply goes quiet — 90 days pass after you filed the objection with no response — you don't have to wait; you can appeal straight to the Tax Court under paragraph 169(1)(b).

The Tax Court runs two tracks, and which one you're on depends mostly on the dollars at stake.

Informal vs. general procedure

The informal procedure is faster, cheaper, and forgiving — relaxed rules of evidence, limited costs, and you don't strictly need a lawyer. It's available where:

the tax and penalties in dispute are $25,000 or less for a taxation year;

the loss in dispute is $50,000 or less; or

for GST/HST, the amount in dispute is $50,000 or less.

A corporation over the line can still elect the informal procedure by capping its claim at the threshold. The general procedure covers everything else — full pleadings, examinations for discovery, and formal rules of evidence. Corporations generally need to be represented by a lawyer in the general procedure, and the stakes (and costs) are higher.

Beyond the Tax Court

A Tax Court decision isn't always the end. From a general-procedure judgment, either side can appeal to the Federal Court of Appeal within 30 days of the judgment (the count excludes July and August), under section 27 of the Federal Courts Act. The final rung is the Supreme Court of Canada, reachable only with the Court's permission — an application for leave filed within 60 days of the Federal Court of Appeal's decision. The vast majority of disputes never travel this far; most settle at Appeals or in the Tax Court.

Disputing the CRA is as much about sequencing and deadlines as it is about being right. A strong objection, filed on time and built like a brief, resolves far more files than a court date ever will. At Modern Axis, we help corporations build the objection properly the first time — because for large corporations especially, what you leave out of the objection is what you lose at trial.

If a reassessment has landed and the 90-day clock is running, don't let it run out. Reach out to Modern Axis and we'll map the fastest credible route to the right number.

Frequently asked questions

How long does a corporation have to file a Notice of Objection?

A corporation has 90 days from the date the notice of assessment or reassessment was sent, under paragraph 165(1)(b) of the Income Tax Act. Unlike individuals — who get the later of one year after their filing-due date or 90 days — corporations get only the 90-day window, measured from when CRA sent the notice, not when you received it.

How does a corporation file a Notice of Objection?

Three ways: Form T400A (the prescribed form), online through My Business Account using "Register my formal dispute," or a signed letter to the Chief of Appeals. In every case the objection must identify the assessment and year, explain why you disagree, and include the relevant facts and supporting documents.

What is the large corporation rule for objections?

A corporation with taxable capital over $10 million (aggregated with related corporations) must, under subsection 165(1.11), describe each issue, specify the relief sought as a dollar amount, and give the facts and reasons in the objection itself. It's then limited at the Tax Court to those stated issues and amounts — and CRA can collect 50% of the disputed amount immediately under subsection 225.1(7).

Can the CRA still collect tax while I dispute an assessment?

For ordinary corporations, objecting generally pauses CRA collection on disputed income tax under subsection 225.1(1). But there's no hold on payroll source deductions or GST/HST, and large corporations can have 50% collected anyway. Arrears interest under section 161 also keeps compounding daily throughout the dispute.

Does interest keep accruing during a Notice of Objection?

Yes. Arrears interest under section 161 continues to accrue on any unpaid balance at the prescribed rate, compounded daily under subsection 248(11). The rate resets quarterly under Regulation 4301 at the three-month Treasury bill yield plus 4%. Paying the amount or posting security stops the interest clock while you dispute.

What happens if the CRA rejects my objection?

You can appeal to the Tax Court of Canada under section 169 within 90 days of CRA confirming or varying the assessment. If CRA doesn't respond within 90 days of your objection, you can appeal directly. The Tax Court offers an informal procedure for smaller disputes ($25,000 or less in tax and penalties per year) and a general procedure for larger ones.

What's the difference between the informal and general Tax Court procedures?

The informal procedure is faster and cheaper, with relaxed evidence rules and no requirement for a lawyer; it's available where the tax and penalties in dispute are $25,000 or less per year (or $50,000 for a loss or GST/HST). The general procedure handles larger disputes with full pleadings, discovery, and formal rules — corporations generally need counsel.

Disclaimer: This article provides general information about Canadian tax matters and does not constitute professional tax, legal, or accounting advice. Tax disputes turn on specific facts, deadlines, and amounts, and the analysis above may not reflect your situation. The author and Modern Axis CPA accept no responsibility for actions taken in reliance on this content. Consult a qualified tax professional or tax lawyer before objecting to or appealing a CRA assessment.

Alex Ataman, CPA

Founder

Modern Axis CPA