The 55% Myth: How Holdco Investment Income Is Taxed

Talk to enough small-business owners about investment income in a holding company in Canada and you'll hear the same line: "I'd love to invest inside the holdco, but the corporate tax rate is around fifty-five percent — there's no point." The line is half-right, which is the dangerous kind of right.

Key takeaways

Holdco investment income tax in Canada looks like a 50.67% sticker rate in BC for 2026, but ~30.67% is refundable as RDTOH the moment the corporation pays a taxable dividend, so the permanent corporate cost is closer to 20%.

RDTOH is split into ERDTOH (eligible dividends) and NERDTOH (non-eligible) under subsection 129(1) ITA; the ordering rule can trap one pool indefinitely if dividends are paid in the wrong order.

If a holdco has an associated opco, Adjusted Aggregate Investment Income above $50,000 grinds the federal Small Business Deduction at $5 per $1 of excess AAII, fully eliminating the SBD at $150,000 (paragraph 125(5.1)(b) ITA).

The Capital Dividend Account is the only mechanism delivering genuinely tax-free flow-through, but missing the Form T2054 election under subsection 83(2) ITA turns a capital dividend into a taxable one.

The headline rate on passive investment income inside a Canadian-controlled private corporation really is in that ballpark. What gets missed is that a meaningful slice of that tax isn't paid, it's prepaid — refundable to the corporation when it pays a taxable dividend out to its shareholders.

Once you put the refund mechanism back into the picture, the story changes. What follows walks through why the gross rate on holding company investment income is so high, where the refundable portion goes while it waits, and a few traps that catch owner-managers who treat the holdco as a permanent tax shelter rather than a deferral tool.

Where the "55%" number actually comes from

The headline rate is built up from a federal stack and a provincial layer. Take a CCPC earning a dollar of investment income — interest, rents, taxable capital gains, or most foreign income earned passively inside the corporation.

The federal piece: the basic Part I rate is 28 percent, less a 10 percent abatement for income earned in a province, plus a 10⅔ percent Additional Refundable Tax that the Income Tax Act layers on a CCPC's investment income. The 13 percent general rate reduction available to active business income doesn't apply to passive investment income. Net federal: 38⅔ percent.

Add the provincial layer. In British Columbia for the 2026 tax year, the general corporate rate is 12 percent, and the active-business 2 percent small business rate doesn't apply to investment income. Combined federal and BC: roughly 50⅔ percent.

Other provinces sit in a similar range — around 47 percent in Alberta, just over 50 percent in Ontario and Quebec, just over 52 percent in Nova Scotia and New Brunswick. The "around 55%" shorthand rounds up, but it is in the right neighbourhood for the gross rate.

That gross rate is what stops most conversations about investment income in a holdco before they start. It is also where most of the misconception lives, because the gross rate is not what the corporation will pay net of the refund mechanism.

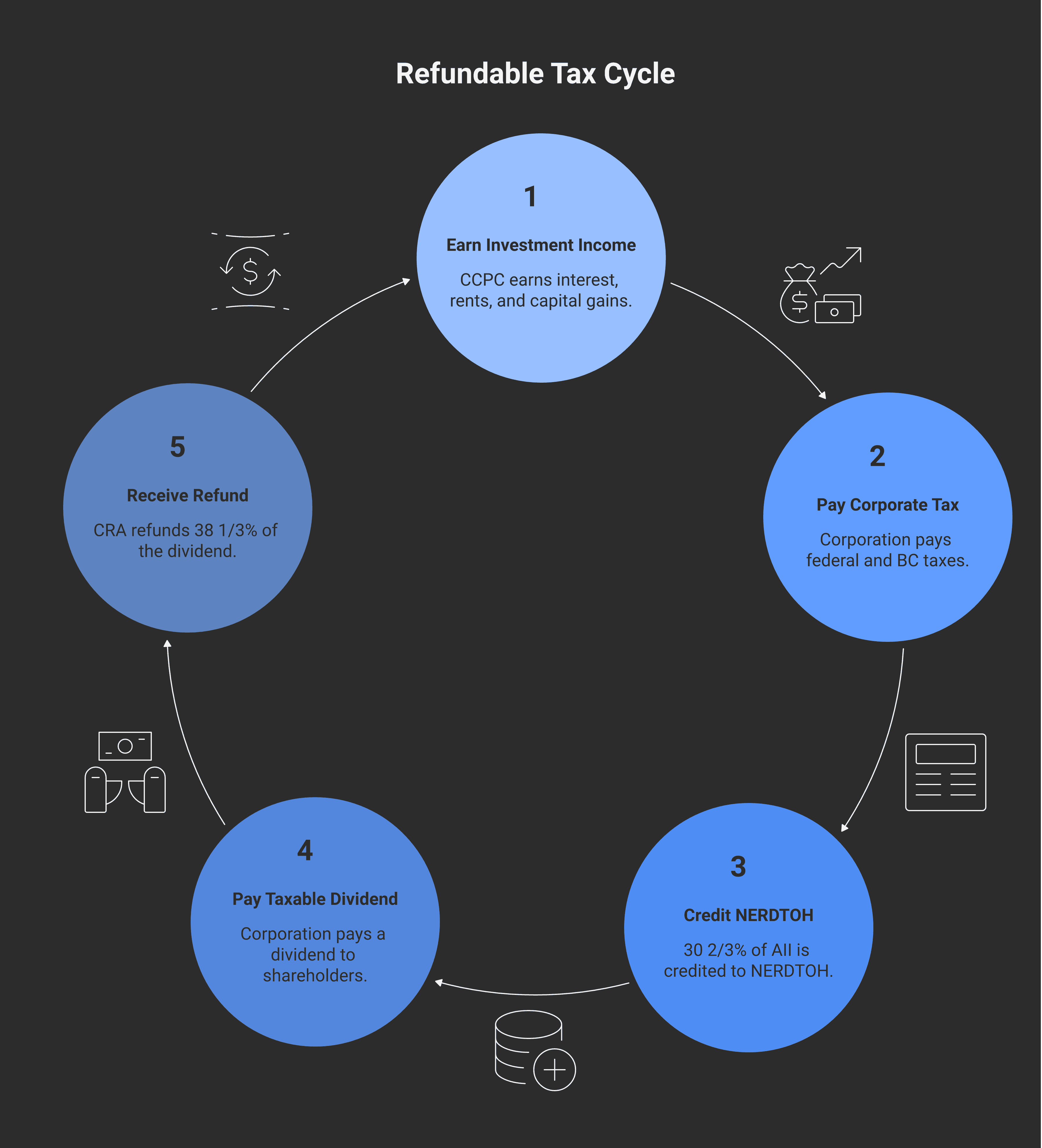

The refund mechanism: RDTOH and the dividend refund

A portion of the federal corporate tax on investment income is held in a notional account at the corporation level, and refunded to the corporation when it pays a taxable dividend out. The notional account is called Refundable Dividend Tax On Hand (RDTOH). The legal hook is subsection 129(1) of the Income Tax Act.

The mechanics are straightforward. Each year, 30⅔ percent of the corporation's investment income gets credited to a notional balance called Non-Eligible RDTOH. When the corporation later pays a taxable dividend, it can claim a refund equal to 38⅓ percent of the dividend paid, capped at the RDTOH balance.

Two practical implications fall out of this.

First, timing. The refund only triggers when a dividend actually flows out to shareholders. Until then, the gross corporate tax has been paid, and the refundable slice is just a balance on a CRA schedule. RDTOH balances do not expire, but they do not earn interest either.

Second, geography. The refundable portion is a federal mechanism. The 12 percent BC corporate tax never refunds. So even after the dividend refund flows back, the corporation has paid roughly 20 percent on the investment income as a permanent cost (50⅔ percent gross, less the 30⅔ percent that came back). That residual is the actual corporate-level cost — far from the 55 percent headline, but not zero.

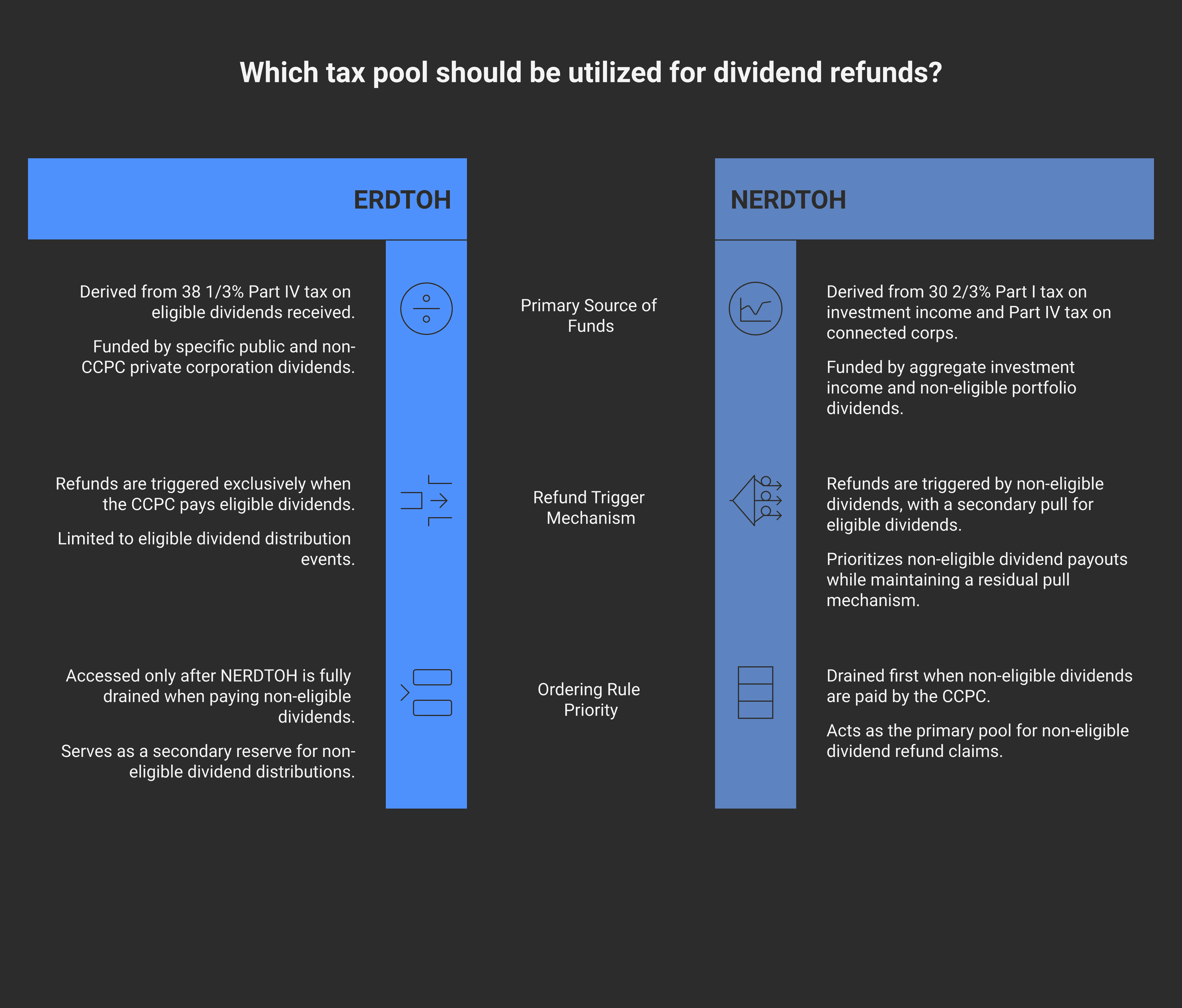

ERDTOH vs NERDTOH: two refund pools, two triggers

Since 2019, the old single RDTOH pool has been split into two. They sit side by side in the Income Tax Act:

Eligible RDTOH (ERDTOH) accumulates when the corporation receives eligible portfolio dividends from a public company or other non-CCPC, and pays the corresponding 38⅓ percent Part IV tax. ERDTOH refunds when the corporation pays eligible dividends out.

Non-Eligible RDTOH (NERDTOH) accumulates from the 30⅔ percent of investment income described above, plus Part IV tax on dividends from connected corporations and any non-eligible portfolio dividends. NERDTOH refunds when the corporation pays non-eligible dividends.

The ordering rule matters more than most owner-managers realise. A non-eligible dividend drains NERDTOH first, and pulls from ERDTOH only after NERDTOH is exhausted. An eligible dividend draws only from ERDTOH. So a corporation that pays only non-eligible dividends can leave its ERDTOH balance trapped indefinitely; one that pays only eligible dividends can leave NERDTOH trapped.

The takeaway: if your holdco is sitting on both kinds of dividend capacity, the type of dividend you choose to pay each year determines which pool empties. That's a planning decision, not a bookkeeping detail.

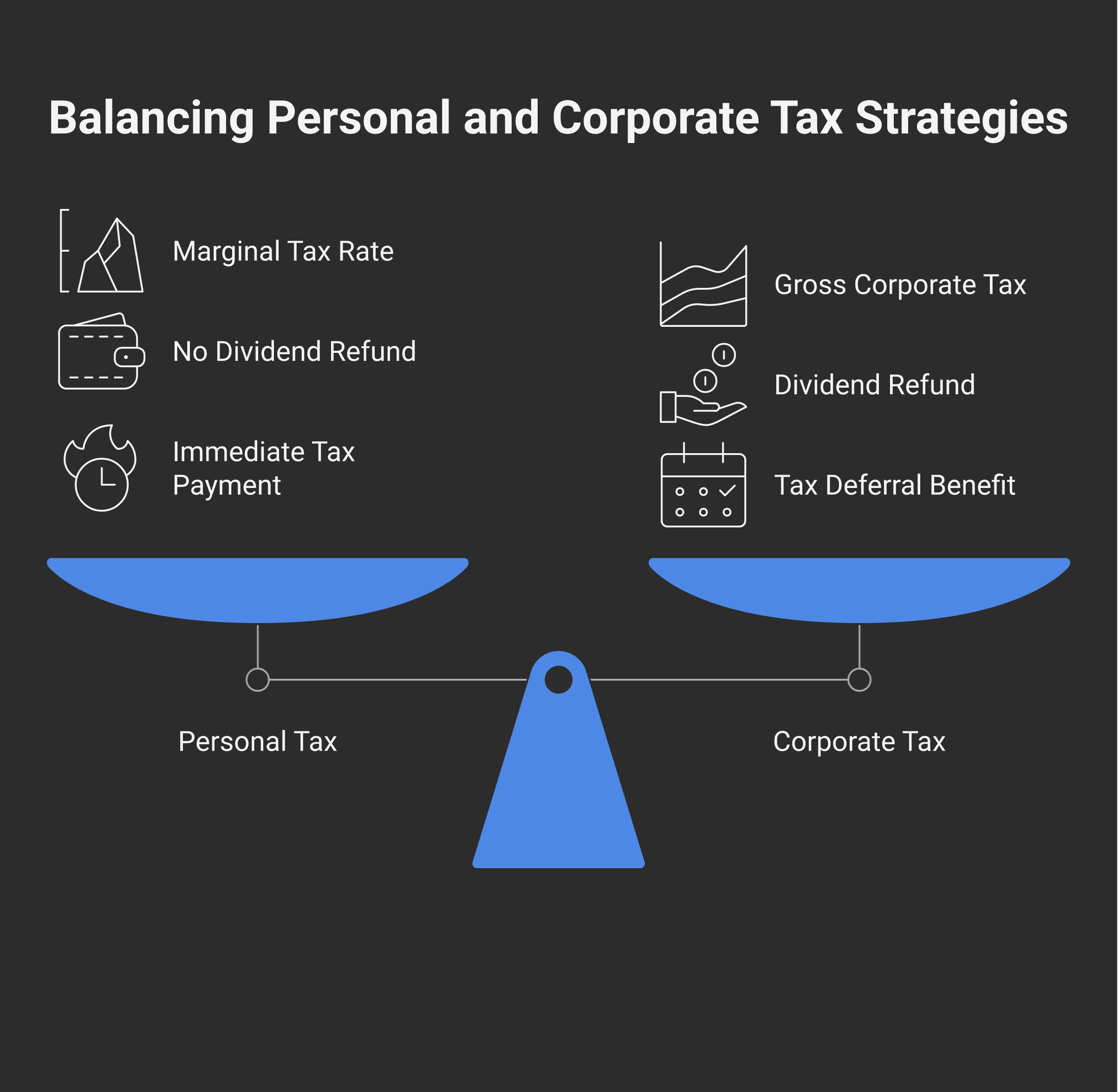

Integration: corporate plus personal tax ≈ personal direct

Everything described above is built around a principle the Canadian tax system aims at but does not perfectly hit: integration. The idea is that a dollar earned through a corporation and paid out as a dividend should bear roughly the same total tax as the same dollar earned by the shareholder personally.

The path: the corporation pays the gross corporate tax, pays a dividend, and gets the dividend refund back. The shareholder receives the dividend, grosses it up, pays personal tax on the grossed-up amount, and claims the dividend tax credit. The credit is calibrated to recognise that the corporation already paid tax on the same dollar.

In British Columbia for the 2026 tax year, the top combined personal rate on a non-eligible dividend is 48.89 percent, on an eligible dividend is 36.54 percent, and on regular income is 53.50 percent. Run the corporate-plus-personal arithmetic and the combined burden lands close to the personal direct rate — a slight under-integration on non-eligible dividends in BC, a slight over-integration in some other provinces. The system is not surgical, but the gap is usually a percentage point or two in either direction.

The holding corporation isn't a tax shelter for investment income. It's a deferral tool: the gross corporate tax is paid up front, the refund waits for the dividend, and the integration math is reconciled when the dividend lands in the shareholder's return. Integration only works if the dividend actually gets paid.

The deferral benefit, and why it disappears if dividends never flow

The genuine planning advantage of investing through a holdco is short-term cash. After the corporation pays the gross corporate tax, roughly 49⅓ percent of the original investment income is available for reinvestment inside the corporation (in BC). A shareholder earning the same dollar at the top BC personal rate would have roughly 46½ percent available to reinvest personally. The corporation has a small head-start on compounding that grows year over year while the funds remain inside the company.

The benefit shows up most cleanly when the eventual dividend is paid in a low-income year — the year the owner sells the operating business, retires, takes parental leave, or for any reason has limited other income. The dividend lands in lower personal brackets, the dividend tax credit does more work, and the deferral pays off. Pay the dividend in a year where the owner is already at the top marginal rate and the deferral benefit shrinks.

At Modern Axis, we see this most often with owner-managers whose holdcos have been accumulating investment income for years without a dividend strategy. The corporate tax has been paid, the RDTOH balances are sitting unused, and nobody has run the integration math against the owner's eventual draw plan.

The trap is straightforward. The holdco is good at deferring tax, not eliminating it. If the dividend never flows, the deferral becomes permanent — and what looked like deferral becomes a permanent overpayment relative to earning the income personally.

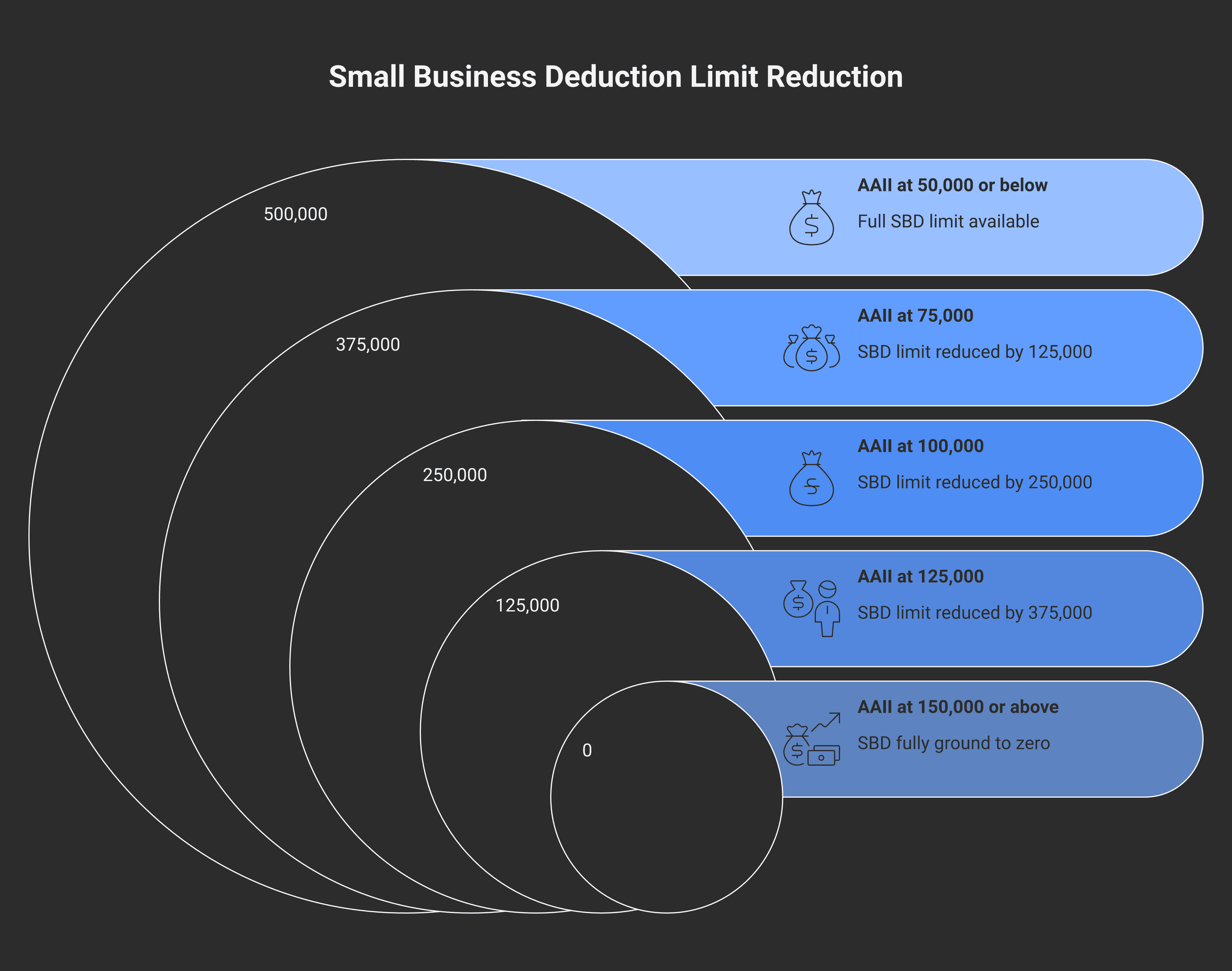

The $50,000 passive income SBD grind

If the holdco has an associated operating company, there is a second consequence to track that has nothing to do with refunds.

Since 2019, subsection 125(5.1)(b) of the Income Tax Act reduces the federal $500,000 Small Business Deduction limit by $5 for every $1 of Adjusted Aggregate Investment Income (AAII) earned by the associated group in the prior calendar year above $50,000. AAII is a slightly modified version of regular investment income designed for this grind.

The math is mechanical. AAII at or below $50,000 leaves the SBD limit intact. AAII at $100,000 cuts it in half. AAII at $150,000 or more grinds the SBD to zero. BC parallels the federal grind for its own small business limit.

The practical effect on a typical opco/holdco structure: a holdco that has been quietly building up an investment portfolio raises the corporate tax bill on the related opco's active business income. The opco pays the higher general corporate rate on whatever portion of the SBD has been ground away, instead of the small business rate it would otherwise have qualified for. The grind is calculated annually, looks at the prior year, and applies to the associated operating company group as a whole.

The pre-2019 model treated active and passive corporate income as separate silos. They are now linked: passive earnings inside the holdco can change the cost of active earnings inside the opco. For owner-managers running a meaningful operating business and a meaningful holdco portfolio, the grind is worth modelling.

The Capital Dividend Account: a tax-free stream

One more piece of the holdco picture worth understanding. When the corporation realises a capital gain on an investment, the gain splits.

The taxable half — currently 50 percent under the half inclusion rate, since the proposed two-thirds rate announced in 2024 was deferred and won't proceed — runs through the rate stack and the refund mechanism just like any other investment income. The non-taxable half flows into the Capital Dividend Account (CDA), a notional balance the corporation tracks separately.

When the corporation has a positive CDA balance, it can pay a capital dividend by election. The capital dividend is received tax-free in the hands of a Canadian-resident shareholder — no gross-up, no tax credit, just non-taxable cash.

The CDA is what genuinely makes a holdco better than personal investment for some specific scenarios involving capital gains or life-insurance proceeds. Capital gains realised inside a corporation do not lose their non-taxable half — they redirect it through the CDA into a tax-free dividend stream. The taxable half still bears the gross corporate rate up front, but the non-taxable half travels a parallel track that never touches personal tax at all.

The trap: capital dividends do not happen automatically. The corporation has to file a Form T2054 election with CRA before paying the dividend. Miss the election and a payment that should have been a tax-free capital dividend can be reassessed as a taxable dividend, sometimes with penalty tax.

Common traps and pitfalls

A handful of recurring issues we see when owner-managers reason about investment income through a holdco:

Treating the gross corporate rate as the final rate. The 50⅔ percent number isn't a permanent cost. It's the gross. The refund and integration math come after.

Forgetting that the refund needs an actual dividend. RDTOH balances accumulate quietly. If no dividend ever flows, the refund stays unrealised and the corporate tax becomes a permanent cost.

Letting AAII drift above $50,000 without modelling the SBD impact. Once the associated opco group is paying the general corporate rate on income that used to qualify for the small business rate, the cost compounds year over year.

Confusing the dividend ordering rule. Non-eligible dividends drain NERDTOH first, then pull from ERDTOH if NERDTOH runs out. Eligible dividends only refund from ERDTOH. The choice of which dividend type to pay each year is a decision, not a default.

Missing the CDA election. A capital dividend isn't a capital dividend until the T2054 election is filed. CRA's position on a missed election is that the dividend is taxable.

Bringing it together

The headline 55 percent number is a real corporate rate. So is the dividend refund. Both numbers describe different points in the same flow, and you cannot draw a planning conclusion from either one without the other.

The integration principle is the system that ties them together. The holding corporation is not a tax shelter for investment income — it is a tool for deferring the timing of personal tax on income that the owner does not yet need in their own hands. Whether the deferral pays off depends on the dividend strategy, the RDTOH and CDA balances, the AAII level relative to the operating company's SBD, and the shareholder's personal tax bracket in the year the dividend lands.

A holdco without a dividend strategy is a permanent prepayment of corporate tax. A holdco with a dividend strategy is a flexible cash-flow tool that lets the owner decide when integration math gets reconciled against their personal-tax picture.

If you're running a holdco and you're not sure whether your dividend strategy is letting the integration math work for you, or whether your active opco's SBD is being quietly eroded by passive investments on the related side, that's exactly the kind of thing our tax planning and compliance team works through with clients. Reach out before year-end if you would like a clear, no-pressure read on where you stand.

Frequently asked questions

Is holdco investment income really taxed at 55% in Canada?

No. The headline rate is roughly 50.67% in BC for 2026, but about 30.67% of every dollar of investment income credits to the corporation's Refundable Dividend Tax On Hand (RDTOH) and refunds at 38.33 cents per dollar of taxable dividends paid out. The actual permanent corporate-level cost on holdco investment income tax in Canada lands closer to 20% in BC once integration runs its course. The 55% figure ignores RDTOH entirely.

How does RDTOH work for a Canadian holding company?

RDTOH is a notional balance tracked annually on the T2 corporate return under subsection 129(1) of the Income Tax Act. It builds as the holdco pays Part I tax on investment income, then refunds at 38.33 cents per dollar of taxable dividends paid to shareholders, capped at the RDTOH balance. The pool does not expire and does not earn interest. No dividend, no refund — which is the core deferral mechanic.

What is the difference between ERDTOH and NERDTOH?

ERDTOH (Eligible RDTOH) accumulates from Part IV tax on eligible portfolio dividends and refunds only when the holdco pays eligible dividends out. NERDTOH (Non-Eligible RDTOH) accumulates from 30.67% of regular investment income plus Part IV tax on connected-corp and non-eligible portfolio dividends. A non-eligible dividend drains NERDTOH first; an eligible dividend pulls only from ERDTOH. Pay them in the wrong order and one pool sits trapped.

What is the $50,000 passive income SBD grind?

Paragraph 125(5.1)(b) of the Income Tax Act reduces the federal $500,000 Small Business Deduction limit by $5 for every $1 of Adjusted Aggregate Investment Income earned by the associated corporate group above $50,000 in the prior calendar year. AAII of $100,000 cuts the SBD in half; AAII of $150,000 grinds it to zero. BC parallels the federal grind on its own small business limit, making holdco investment income tax planning a CCPC-wide problem.

Should I invest through a holdco or personally?

It depends on when dividends actually flow. The holdco's deferral advantage is real when shareholders pull dividends in low-income years — retirement, parental leave, the year a business is sold. If dividends never flow, the corporate tax becomes a permanent overpayment and integration breaks the wrong way. Holdcos help when there's a meaningful spread between current and future personal marginal rates, not as a default.

What is the Capital Dividend Account and why does it matter?

The Capital Dividend Account (CDA) is a notional balance tracking the non-taxable half of capital gains realised inside the corporation, currently 50% of the gain. With a positive CDA balance, the corporation can elect under subsection 83(2) of the Income Tax Act — using Form T2054 — to pay a capital dividend received tax-free by Canadian-resident shareholders. Miss the T2054 election and CRA treats the distribution as an ordinary taxable dividend, often with penalty interest.