GST/HST for Small Business Canada: Complete 2026 Guide

The GST/HST system is the single biggest source of unforced compliance errors among Canadian small businesses — and the most common pattern is registering too late, missing input tax credits, or filing on the wrong frequency. The mechanics are largely the same as they were in 1991 when the GST was introduced, but the practical traps have multiplied as e-commerce, digital platforms, cross-border services, and remote contractors have made the "place of supply" question harder.

This guide walks through how the GST/HST works for a Canadian small business in 2026 — the $30,000 small-supplier threshold, voluntary early registration, filing frequencies, Input Tax Credits (ITCs), the Quick Method overview, place-of-supply rules, and the most common compliance mistakes we see in practice.

Key takeaways

A Canadian business must register for GST/HST under subsection 240(1) of the Excise Tax Act once taxable supplies exceed $30,000 over any four consecutive calendar quarters (or in a single calendar quarter). For public service bodies, the threshold is $50,000.

Voluntary registration is allowed below the threshold under subsection 240(3). For most B2B service businesses, voluntary early registration is a positive — it lets the business claim Input Tax Credits on startup expenses that would otherwise be lost.

Filing frequency depends on annual taxable supplies: under $1.5M = annual filer; $1.5M to $6M = quarterly; over $6M = monthly. Filers can voluntarily file more frequently for cash flow management.

Input Tax Credits (ITCs) under section 169 of the Excise Tax Act let registrants recover the GST/HST paid on inputs used in commercial activity. The ITC eligibility test, documentation requirements, and timing rules are where most small-business errors happen.

The Quick Method under section 227 of the ETA is an alternative reporting method where the business remits a flat percentage of GST/HST-included sales instead of tracking ITCs. Eligible for businesses with worldwide revenue under $400,000. Often more efficient for low-input service businesses.

What is the GST/HST?

The GST (Goods and Services Tax) is a 5% federal value-added tax on most supplies of goods and services in Canada. The HST (Harmonized Sales Tax) is the same federal 5% plus a provincial component, combined into a single tax administered by the federal government, in five provinces:

Province | HST rate | Federal portion | Provincial portion |

|---|---|---|---|

New Brunswick | 15% | 5% | 10% |

Newfoundland and Labrador | 15% | 5% | 10% |

Nova Scotia | 14% | 5% | 9% |

Ontario | 13% | 5% | 8% |

Prince Edward Island | 15% | 5% | 10% |

In the remaining provinces and territories — BC, Alberta, Saskatchewan, Manitoba, Quebec, Yukon, NWT, Nunavut — only the federal 5% GST applies. Several of those provinces have a separate provincial sales tax (BC's PST, Saskatchewan's PST, Manitoba's RST) layered on top, administered provincially, not by the CRA.

Quebec has the QST (Quebec Sales Tax) at 9.975%, administered by Revenu Québec on top of the federal 5% GST — together producing a combined 14.975%.

The "GST/HST" system in this post refers to the federal-and-HST regime administered by the CRA. Provincial sales taxes are administered separately.

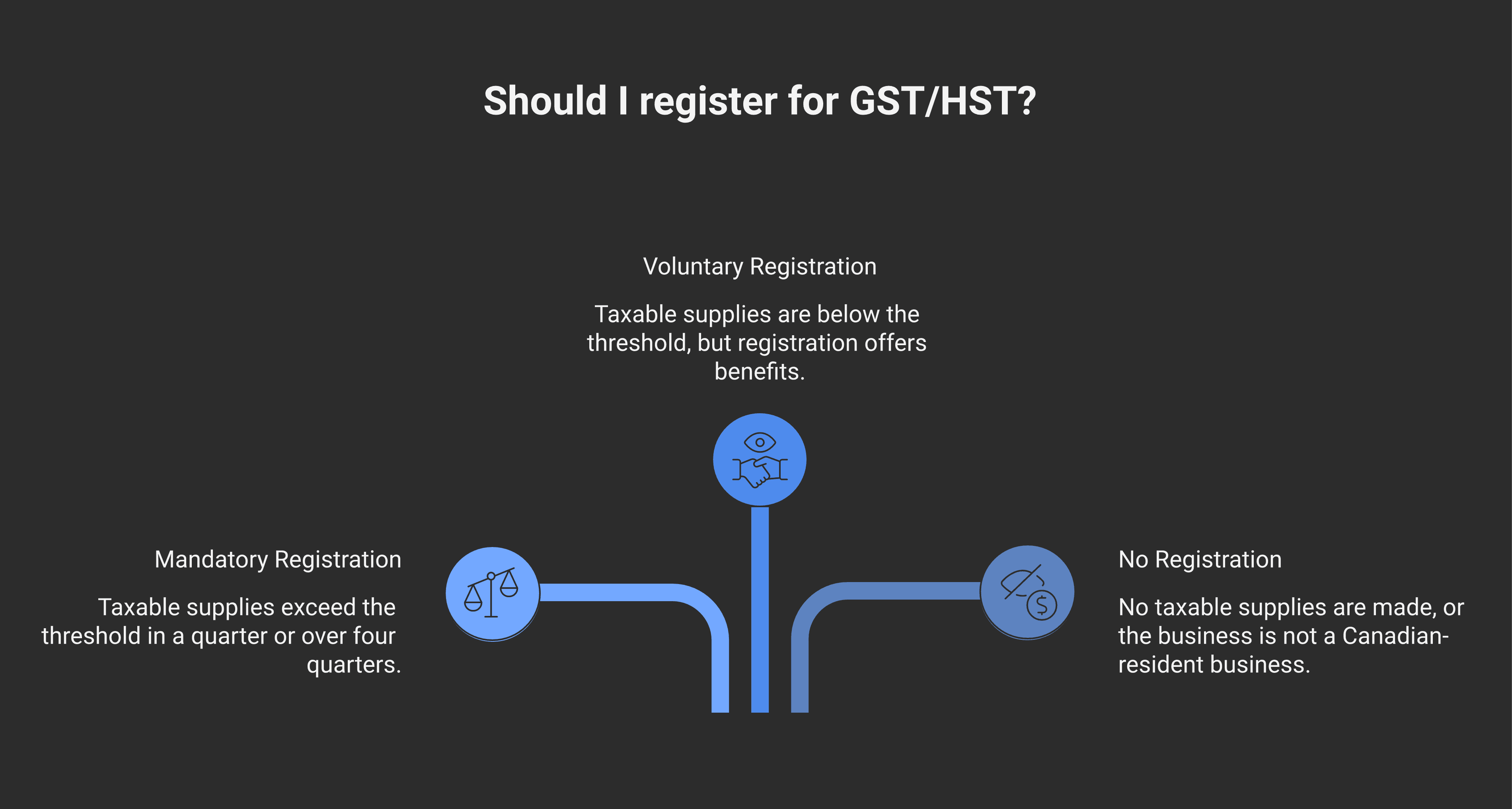

The $30,000 small-supplier threshold

Under section 148 of the Excise Tax Act, a business is a "small supplier" if its worldwide taxable supplies (plus those of associated persons) are $30,000 or less over the prior four calendar quarters.

Small suppliers:

Do not have to charge GST/HST on their supplies

Do not have to register

Cannot claim ITCs on their inputs (the GST/HST paid on business expenses is just a cost)

A business stops being a small supplier and must register in either of two scenarios:

Single-quarter test: Taxable supplies (and those of associates) exceed $30,000 in a single calendar quarter. The business is liable for GST/HST on the supply that made it exceed the threshold and onward.

Four-quarter test: Taxable supplies (and those of associates) exceed $30,000 in any four consecutive calendar quarters (not necessarily a fiscal year). The business has one month from the end of the month following the quarter in which the threshold was crossed to register.

Public service bodies (charities, non-profits, universities, schools, public hospitals, municipalities) have a higher $50,000 threshold under subsection 148(1) of the ETA.

Excluded from the threshold calculation under section 148: revenue from financial services, supplies of capital property, and proceeds from sale of goodwill.

The single biggest mistake here is counting too narrowly. The threshold is worldwide taxable supplies — not just Canadian, not just product-line specific. A Canadian-resident IT consultant making $25K of Canadian work and $15K of US client work has $40K of taxable supplies for threshold purposes, despite the US work being zero-rated for HST purposes.

Voluntary registration

Section 240(3) of the Excise Tax Act allows businesses below the small-supplier threshold to register voluntarily. The decision turns on a simple cost-benefit:

Voluntary registration benefits:

Claim ITCs on GST/HST paid on business inputs (often substantial in early years: legal, accounting, software, equipment, etc.)

Reduced friction with B2B customers — most prefer to deal with registered suppliers who can provide a GST/HST receipt

Easier transition once growth crosses the threshold

Voluntary registration costs:

Compliance burden — quarterly or annual filings; record-keeping

Customer prices rise (or business absorbs the tax) — most relevant for B2C service businesses

Locks the business into the system; deregistration requires a separate process and minimum holding period

Best fit for voluntary registration:

B2B service businesses where customers are also GST/HST registrants (they recover the GST/HST as ITCs and don't care)

Businesses with substantial early-stage capital purchases (vehicles, equipment, build-out costs)

Businesses expecting to cross $30K within 12-18 months

Best fit to stay unregistered:

B2C service businesses where customers can't recover the tax (the price increase hurts)

Truly small operations with little input GST/HST to recover

For most Canadian small business owners we work with at Modern Axis, voluntary registration is a positive choice from year one — the lost ITCs from waiting are usually larger than the compliance friction.

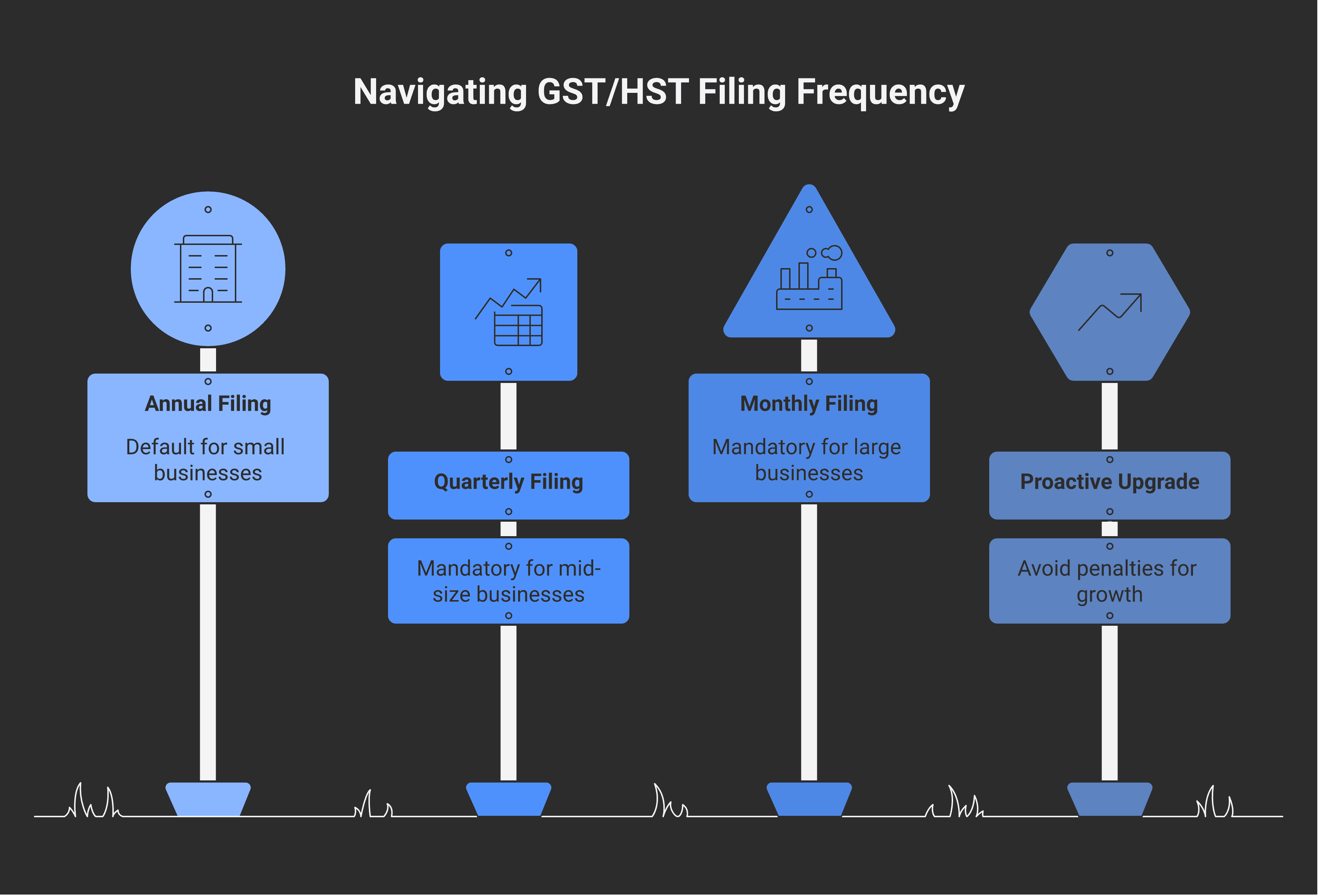

Filing frequency

Once registered, the business is assigned a filing frequency under section 245 of the Excise Tax Act:

Annual taxable supplies | Default filing frequency |

|---|---|

Under $1.5M | Annual |

$1.5M to $6M | Quarterly |

Over $6M | Monthly |

Voluntary increase in filing frequency is allowed:

Annual filers can elect quarterly or monthly

Quarterly filers can elect monthly

This matters for two reasons:

Refund position. A business in a regular refund position (because ITCs exceed collections — common for net exporters, businesses with heavy capital purchases, certain construction businesses) wants to file more frequently to receive refunds sooner. Annual filing means waiting up to a year for the refund.

Cash flow management. A business in a regular tax-owing position can manage cash flow better with quarterly filings (smaller, more predictable remittances) than annual (one large bill).

The deadlines are tight: monthly and quarterly filers must file and remit within one month after the reporting period ends. Annual filers (for individuals filing on the sole-proprietorship side) have until June 15 of the following year, but any tax owing is due April 30. Corporations on annual filing remit three months after fiscal year-end. Most businesses find a quarterly cadence is the practical sweet spot.

Input Tax Credits — the recovery side

Input Tax Credits are how GST/HST registrants recover the tax they paid on business inputs. The mechanic, under section 169 of the Excise Tax Act:

Eligible ITC = GST/HST paid or payable × percentage of use in commercial activity

For most fully-commercial businesses, the percentage is 100% and the ITC equals the full GST/HST paid. Mixed-use property (a vehicle used 70% for business, 30% personal) gets a 70% ITC.

Documentation requirements under Regulations to the Excise Tax Act, section 3 of the Input Tax Credit Information (GST/HST) Regulations:

Total invoice amount | Required information |

|---|---|

Under $30 | Supplier name + date |

$30 to $150 | Above + supplier GST/HST number + amount of tax (or statement) |

$150 or more | Above + purchaser name + business address + indication of total tax paid |

The single biggest ITC error: missing the supplier's GST/HST number on invoices over $30. CRA can deny the ITC for a missing GST/HST number on an invoice over $30 — even where the supplier is registered and the tax was paid. Always verify the supplier's GST/HST number on invoices over $30.

Timing of the claim. ITCs can be claimed in the reporting period in which they become eligible — but the rule is that ITCs must be claimed within four years of the period in which they were eligible (two years for "large" claimants — generally those over $6M of taxable revenue). Missed ITC claims after the deadline are permanently lost.

Mixed-use property special rules. Several specific items have ITC rules that depart from the general formula:

Meals and entertainment. ITC is limited to 50% of the GST/HST paid (mirroring the income tax 50% limit under section 67.1 of the ITA).

Passenger vehicles. ITC limited to the GST/HST on the prescribed cost ceiling — currently the GST/HST on $39,000 plus tax for non-luxury passenger vehicles.

Club memberships and recreational dues. Generally no ITC.

Personal-use portions of mixed-use property. No ITC on the personal-use portion.

Place of supply rules

Whether a particular supply attracts GST, HST (and at which provincial rate), or zero-rating depends on the place of supply rules under Part IX of the Excise Tax Act and the New Harmonized Value-Added Tax System Regulations.

The general principles:

Tangible goods. Place of supply is generally where the goods are delivered. Shipping a product from Ontario to a customer in BC = BC place of supply (GST only, no HST).

Services. Place of supply is generally where the recipient is ordinarily located (for B2B) or where the service is performed (for B2C). The detailed rules are in the New Harmonized Value-Added Tax System Regulations.

Exports. Most goods and services supplied to customers outside Canada are zero-rated — no tax charged, but full ITCs available on inputs. The supplier collects no tax but recovers the tax on their inputs.

Digital products and services to consumers in Canada. Since 2021, non-resident vendors selling digital products and services to Canadian consumers must register for the simplified GST/HST and collect tax — including platforms like Netflix, Spotify, Microsoft 365, AWS for personal accounts. B2B sales to Canadian-registered businesses don't trigger the simplified registration, but the Canadian buyer typically self-assesses HST under the reverse-charge rules.

Quebec. The QST has its own parallel place-of-supply rules administered by Revenu Québec. A business doing sales into Quebec generally needs to register with both CRA (federal HST/GST) and Revenu Québec (QST).

Common compliance mistakes

Mistake 1: Late registration. A business that crosses the $30,000 threshold and doesn't register on time still owes the GST/HST on the supply that triggered the threshold and onward — they just have to pay it from their own pocket (no longer able to add it to invoices retroactively for many cases). This is the single most expensive small-business GST/HST error we see.

Mistake 2: Counting only Canadian sales toward the threshold. Worldwide taxable supplies count, including zero-rated exports. A Canadian consultant working primarily for US clients can easily cross the threshold without realizing it.

Mistake 3: Mixed-use vehicle ITCs above 50% on a passenger vehicle. Vehicles used 30%+ personally don't get the full ITC. Even at 100% business use, passenger vehicles have a hard cost-ceiling cap on the ITC.

Mistake 4: Meals and entertainment ITC at 100%. Only 50% of the GST/HST on meals is recoverable as an ITC, mirroring the income tax 50% limit.

Mistake 5: Missing supplier GST/HST numbers. Especially in industries where small contractors send hand-written or template invoices, the supplier's GST/HST number is often missing. ITC denied on invoices over $30 without the number.

Mistake 6: Mis-applying place of supply. Charging Ontario HST (13%) to a BC customer who should have been charged GST only (5%) creates a customer dispute and a CRA correction.

Mistake 7: Not changing filing frequency proactively. A business that grew from $400K to $2.5M of revenue is now required to file quarterly — not annually. Defaulting to the prior frequency triggers late-filing penalties on the quarterly returns that should have been filed.

Mistake 8: Missing the four-year ITC claim deadline. Old invoices from prior years sitting in the bookkeeping system without their ITC claimed are lost after four years.

For more on the GST/HST treatment of specific situations — GST on short-term rentals, GST on real estate transactions — see our companion guides.

The Quick Method — preview

The Quick Method (covered in detail in our forthcoming Quick Method deep-dive) is an alternative reporting method where the registrant remits a flat percentage of GST/HST-included sales to the CRA instead of tracking ITCs in detail.

Eligibility under section 227 of the Excise Tax Act:

Worldwide annual revenue under $400,000 (taxable supplies, not including zero-rated exports)

The business has been registered for at least one year (some exceptions apply for new registrants)

The business is not a member of certain ineligible categories (professional accountants and bookkeepers, financial-service providers, certain other categories)

Quick Method rates are lower than the standard 5%/13%/15%, reflecting an embedded ITC. For example:

A service business in Ontario (HST 13%) remits 8.8% of GST/HST-included sales (down from 13%)

A service business in BC (GST 5% only) remits 3.6% of GST/HST-included sales

The savings come from the implicit ITC built into the Quick Method rate, plus a $300 ITC bonus on the first $30,000 of supplies each year for the registrant. For low-input service businesses, the Quick Method often produces a meaningful savings versus the regular method.

The Quick Method election is made on Form GST74 under section 227. The election can be revoked once made, but only after one full year and not retroactively.

Annual GST/HST planning

A few practical moves for small-business GST/HST management:

Register early voluntarily. For most B2B service businesses, the ITC recovery from voluntary registration outweighs the compliance burden. The decision is fact-specific — but the default for small business owners working with us is registration from year one.

Set the filing frequency to match the cash position. Net refund position → file as frequently as possible. Net owing → match the cadence to the business's cash flow rhythm.

Run the Quick Method analysis annually. A business with stable low-input service revenue under $400K may benefit from the Quick Method. Run the math each year against the regular method to confirm.

Reconcile ITCs to GST/HST collected quarterly. A regular reconciliation catches missing supplier numbers, mis-coded entries, and timing issues before they become four-year-old problems.

Track the place-of-supply analysis for each customer. Especially important for service businesses with cross-province or cross-border customers. A simple lookup table of customer location → applicable tax saves audit time.

Use the Dext-style automation we recommend for source-document capture. Missing supplier GST/HST numbers is the easiest preventable error.

Frequently asked questions

What is the GST/HST registration threshold for 2026?

The small-supplier threshold is $30,000 of worldwide taxable supplies over any four consecutive calendar quarters under subsection 240(1) of the Excise Tax Act. A business with public service body status (charity, non-profit, etc.) has a $50,000 threshold. The threshold is also breached in any single calendar quarter where taxable supplies exceed $30,000. The threshold has not changed for many years and is not indexed.

Can I voluntarily register for GST/HST before reaching the threshold?

Yes. Under subsection 240(3) of the Excise Tax Act, small suppliers can voluntarily register. The decision turns on whether the ITC recovery from voluntary registration outweighs the compliance burden. For most B2B service businesses with substantial input GST/HST and business-customer audiences, voluntary registration from year one is the right default.

What is the GST/HST filing frequency for a small business?

Filing frequency is set under section 245 of the Excise Tax Act based on annual taxable supplies: under $1.5M = annual filer, $1.5M to $6M = quarterly, over $6M = monthly. Registrants can voluntarily file more frequently for cash-flow or refund-position reasons. Defaulting to the prior frequency after a revenue tier change creates late-filing penalties.

What documentation do I need to claim an Input Tax Credit?

Documentation requirements scale with invoice amount under the Input Tax Credit Information (GST/HST) Regulations: under $30 needs supplier name and date; $30 to $150 adds the supplier's GST/HST number and tax amount (or "GST/HST included" statement); $150+ adds purchaser name, business address, and indication of total tax paid. The most common ITC denial is for missing the supplier's GST/HST number on invoices over $30.

What is the Quick Method and who can use it?

The Quick Method under section 227 of the Excise Tax Act lets eligible registrants remit a flat percentage of GST/HST-included sales instead of tracking ITCs. Eligibility requires worldwide annual revenue under $400,000 and the registrant cannot be in certain ineligible categories (professional accountants and bookkeepers, financial-service providers, etc.). The election is made on Form GST74.

Do I have to charge HST when selling to a customer in another province?

Place-of-supply rules under the New Harmonized Value-Added Tax System Regulations determine which rate applies. For tangible goods, the place of supply is generally where the goods are delivered — so a sale from Ontario to BC attracts only the 5% GST (not the 13% Ontario HST). For services, the place of supply is generally where the recipient is ordinarily located (B2B) or where the service is performed (B2C). The detailed rules are nuanced — registrants should reference the specific regulation for each transaction type.

What happens if I don't register for GST/HST on time?

If you cross the $30,000 threshold and fail to register on time, you remain liable for the GST/HST on supplies made after the threshold was crossed — even though you didn't collect it from customers. The unpaid GST/HST becomes a personal cost. Late registration also triggers penalties under section 280 of the Excise Tax Act on the unpaid tax. The Voluntary Disclosures Program may provide relief from penalties (though not the underlying tax) — see our VDP guide.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA