GST/HST Quick Method: When It Beats Regular Method (2026)

The GST/HST Quick Method is one of the most underused tax tools available to small Canadian service businesses. Eligible businesses remit a flat percentage of GST/HST-included sales to the CRA instead of tracking Input Tax Credits (ITCs) on every business expense. For low-input service businesses, the Quick Method often produces a meaningful savings — sometimes $1,000-$5,000 per year — versus the regular method.

This guide walks through the Quick Method mechanics under section 227 of the Excise Tax Act, the eligibility rules, the by-province rate table, when to elect (and when not to), the $300 ITC bonus, and how to switch back if circumstances change.

Key takeaways

Eligibility under section 227 of the Excise Tax Act: worldwide annual revenue under $400,000 (including taxable supplies and zero-rated exports), registered for at least one fiscal quarter, and not engaged in certain ineligible activities (professional accountants and bookkeepers, financial service providers, lawyers, charities with specific designations).

The mechanic: instead of tracking ITCs on every business expense, the registrant remits a flat Quick Method rate of GST/HST-included sales each reporting period. The Quick Method rate is lower than the actual GST/HST rate — the differential is the implicit ITC bonus.

First $30,000 of supplies each year gets a $300 ITC bonus under section 17 of the Streamlined Accounting (GST/HST) Regulations — automatic credit for newly-electing businesses, equivalent to a 1% reduction on the first $30K of supplies.

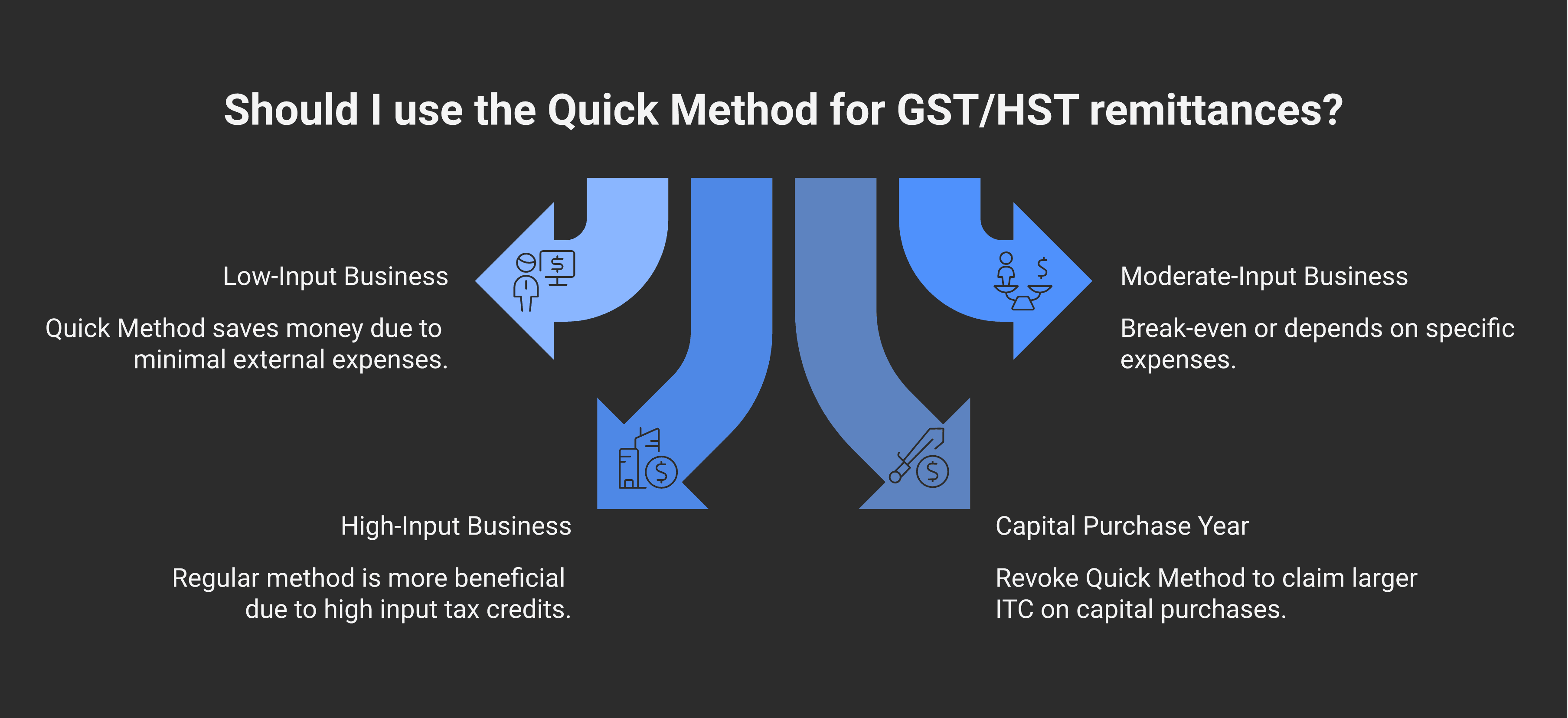

Service businesses with low input GST/HST typically win with the Quick Method. Businesses with substantial capital purchases, inventory, or other high-input expenses typically lose — the implicit ITC built into the Quick Method rate doesn't cover their actual ITC entitlement.

Election is made on Form GST74, effective from the start of the GST/HST reporting period. Switch-back is allowed but only after one full year and not retroactively.

Quick Method eligibility

Section 227 of the Excise Tax Act sets out four eligibility requirements:

1. Worldwide annual revenue under $400,000. Includes all taxable supplies (zero-rated exports count toward the threshold). The test is applied annually; a business that grows past $400K must revoke the Quick Method election.

2. Registered for GST/HST. Must have been in business continuously throughout the year (365 days) ending immediately before your current reporting period; new registrants who have not been in business that long qualify instead via the first-full-year reasonable-expectation test ($400,000 or less in taxable supplies).

3. Not in an ineligible category. The following businesses cannot use the Quick Method:

Professional accountants and bookkeepers

Lawyers and notaries

Financial-service providers (banks, securities dealers, insurance brokers)

Listed financial institutions

Charities with specific designations (some can elect; most cannot)

Tax preparers (per CRA's interpretation)

4. The election applies for at least one full year. Once elected, the registrant must use the Quick Method for at least one full fiscal year before revoking.

For most Canadian small-business service registrants (consultants, IT contractors, marketing agencies, design firms, freelance professionals), the Quick Method is available.

Quick Method rate table by province (2026)

The Quick Method rate is lower than the regular GST/HST rate. The differential represents the implicit ITC bonus the Quick Method gives.

Rates depend on:

Where the customer is located (place of supply rules)

The business type (services vs goods)

The province where the business operates

A representative Quick Method rate table for service businesses (where the customer is in the same province as the business):

Province where business is located | Quick Method rate on services (customer in same province) | Regular rate |

|---|---|---|

British Columbia (GST only) | 3.6% | 5% |

Alberta (GST only) | 3.6% | 5% |

Saskatchewan (GST only) | 3.6% | 5% |

Manitoba (GST only) | 3.6% | 5% |

Quebec (GST only) | 3.6% | 5% |

Yukon, NWT, Nunavut (GST only) | 3.6% | 5% |

Newfoundland and Labrador (HST 15%) | 10.4% | 15% |

Prince Edward Island (HST 15%) | 10.4% | 15% |

Nova Scotia (HST 15%) | 10.4% | 15% |

New Brunswick (HST 15%) | 10.4% | 15% |

Ontario (HST 13%) | 8.8% | 13% |

Important nuance: these are the rates where the customer is in the same province as the business. For sales to customers in other provinces, the rate adjusts based on the customer's province (the place of supply). For example, an Ontario business selling services to a BC customer typically applies a lower Quick Method rate to that BC-bound sale.

Goods sales have different (slightly higher) Quick Method rates than services — the implicit ITC is smaller for goods businesses because goods businesses typically have higher actual ITCs.

For the comprehensive Quick Method rate table covering all province combinations and goods vs services, see CRA's RC4058 Quick Method publication.

How the math works — when Quick Method wins

The Quick Method's appeal comes from two factors:

1. The implicit ITC built into the rate. A typical Ontario service business charges 13% HST to customers and remits 8.8% under Quick Method. The 4.2% difference is the implicit ITC. For a business with low actual ITCs, the implicit ITC exceeds their actual ITC entitlement — net savings.

2. The $300 ITC bonus on first $30,000 of supplies. Under section 17 of the Streamlined Accounting (GST/HST) Regulations, the first $30,000 of supplies each fiscal year gets an automatic $300 credit. This is equivalent to a 1% reduction on the Quick Method rate for the first $30K.

Where Quick Method wins: Low-input service businesses with annual revenue under $400K and minimal capital purchases.

Where Quick Method loses: Businesses with substantial capital purchases (new equipment, vehicles, build-outs), inventory-heavy businesses, businesses with significant operating expenses subject to GST/HST. For these, the actual ITCs they would claim under the regular method exceed the implicit ITC in the Quick Method rate.

A typical analysis:

Hypothetical Ontario consultant with $200K annual revenue, $5K in deductible GST/HST on business expenses:

Regular method:

HST collected: $200,000 × 13% = $26,000

ITCs claimed: $5,000

Net HST remittance: $26,000 − $5,000 = $21,000

Quick Method:

HST collected: $200,000 × 13% = $26,000 (charged to customers; still includes the 13%)

Quick Method remittance: $226,000 × 8.8% = $19,888

$300 ITC bonus on first $30K (actually $30,000 × 1% = $300)

Net remittance: $19,888 − $300 = $19,588

Net savings with Quick Method: $21,000 − $19,588 = $1,412

For a consultant with low input GST/HST, that's $1,400+ per year of savings — meaningful relative to compliance time saved.

When Quick Method doesn't win

Heavy capital purchase year. A business in a year of substantial capital purchases (new equipment, vehicle, build-out) typically should NOT be on Quick Method that year. The actual ITC on the capital purchase would exceed the Quick Method savings.

Inventory-heavy businesses. Retail and goods-based businesses typically claim substantial ITCs on inventory purchases. The Quick Method rate for goods is smaller (less implicit ITC), and the actual ITC on inventory typically exceeds the Quick Method differential.

Mixed businesses. A consulting business that also resells products has mixed actual ITCs. Quick Method analysis is complicated; case-by-case review needed.

High-expense service businesses. Some service businesses have substantial third-party subcontractor expenses, software subscriptions, or other operating expenses subject to GST/HST. If these are large relative to revenue, the actual ITC entitlement exceeds the Quick Method's implicit ITC.

How to elect and switch

Election: File Form GST74 with CRA. The election is effective from the start of the reporting period in which the form is filed (or the prior reporting period, if filed within 1 month of the start).

Switching back: Once elected, the Quick Method must be used for at least one full fiscal year. After that, the registrant can revoke by filing another GST74 (with the revoking option selected). The revocation is effective from the start of the reporting period in which the revocation form is filed.

Switching can be done strategically: A consultant who anticipates a large capital purchase year can revoke the Quick Method for that year, claim the actual ITCs on the capital purchase under the regular method, then re-elect Quick Method for subsequent low-input years.

Coordination with the broader GST/HST framework

Quick Method registrants still need to:

Charge full GST/HST on supplies — Quick Method affects only the remittance, not the customer-facing rate

Issue compliant invoices — same documentation requirements

File GST/HST returns on the normal cadence (annual / quarterly / monthly per filing-frequency tier — see our GST/HST pillar)

Recover ITCs on capital purchases even on Quick Method — the rule is that capital property (such as computers and vehicles) can still claim ITCs separately, with no dollar threshold

Track for the $400K revenue ceiling annually

The Quick Method is one piece of the broader GST/HST framework — it changes the remittance calculation, but the rest of the compliance is unchanged.

Common compliance considerations

Re-evaluate annually. Business circumstances change. A consulting business in year 1 (minimal input) may shift to a higher-input model in year 3 (hiring contractors, buying equipment). Annual review of Quick Method vs Regular Method is standard practice.

Watch the $400K ceiling. A business growing past $400K must revoke the Quick Method. The revocation is effective from the start of the relevant reporting period — not retroactively. Failure to revoke can trigger CRA review.

Don't double-claim ITCs. Some new Quick Method registrants attempt to claim ITCs on expenses despite being on Quick Method — this is incorrect. The implicit ITC is built into the Quick Method rate; explicit ITC claims on the same expenses are not allowed (except for the specific capital-purchase exception, which applies to capital property regardless of dollar amount).

Document the choice. When the Quick Method is elected, document the analysis showing why it's the better choice. This protects against a CRA review questioning the election.

For Modern Axis client engagements on small-business GST/HST, the Quick Method analysis is part of the annual planning conversation — whether to elect, whether to revoke, and whether the current business mix supports continued Quick Method use.

Frequently asked questions

What is the GST/HST Quick Method?

The Quick Method under section 227 of the Excise Tax Act lets eligible small-business GST/HST registrants remit a flat percentage of GST/HST-included sales each reporting period, instead of tracking Input Tax Credits (ITCs) on every business expense. The implicit ITC is built into the Quick Method rate. The election is made on Form GST74.

Who can use the GST/HST Quick Method?

Eligibility requires: (1) worldwide annual revenue under $400,000 (including zero-rated exports); (2) GST/HST registered for at least one fiscal quarter; (3) not in an ineligible category (professional accountants and bookkeepers, lawyers, financial service providers, listed financial institutions, certain charities). Service businesses with low input GST/HST typically benefit most.

What is the Quick Method rate for a service business in Ontario?

For a service business operating in Ontario (HST 13%) with customers in Ontario, the Quick Method rate is 8.8% of GST/HST-included sales (down from 13% under the regular method). The 4.2% differential represents the implicit ITC. For services sold to customers in other provinces, the rate adjusts based on the customer's province under place-of-supply rules.

What is the $300 ITC bonus under the Quick Method?

Under section 17 of the Streamlined Accounting (GST/HST) Regulations, the first $30,000 of supplies each fiscal year gets an automatic $300 ITC credit. This is equivalent to a 1% reduction on the Quick Method rate for the first $30K. The credit applies to most Quick Method registrants — providing additional savings on top of the implicit ITC built into the rate.

When does the Quick Method save money vs the regular method?

The Quick Method saves money when actual ITC entitlement is less than the implicit ITC built into the Quick Method rate. This typically applies to low-input service businesses with annual revenue under $400K. The Quick Method loses money when actual ITCs exceed the implicit ITC — typically for businesses with substantial capital purchases, inventory-heavy operations, or high operating expenses subject to GST/HST.

How do I elect the Quick Method?

File Form GST74 with CRA. The election is effective from the start of the reporting period in which the form is filed (or the prior reporting period, if filed within 1 month of the start). Once elected, the Quick Method must be used for at least one full fiscal year before revocation is allowed.

Can I switch back from Quick Method to Regular Method?

Yes, after using the Quick Method for at least one full fiscal year. Revocation is also filed on Form GST74. The revocation is effective from the start of the reporting period in which the revocation form is filed — not retroactively. Strategic switching is allowed: a business anticipating a large capital purchase year can revoke for that year, claim actual ITCs, then re-elect for subsequent low-input years.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA