Corporate Restructuring Canada: Sections 85, 86, 87, 88

Most Canadian corporate restructuring transactions — estate freezes, family business reorganizations, amalgamations, sub wind-ups, holding-company implementations — use one of four key Income Tax Act provisions: section 85 (asset rollover), section 86 (internal share reorganization), section 87 (amalgamation), or section 88 (wind-up). Each tool achieves a specific structural outcome with different tax mechanics, documentation requirements, and post-transaction implications.

This guide maps which tool fits which problem — the "which section for which transaction" reference that owner-managers, in-house counsel, and CPAs use when planning corporate change.

Key takeaways

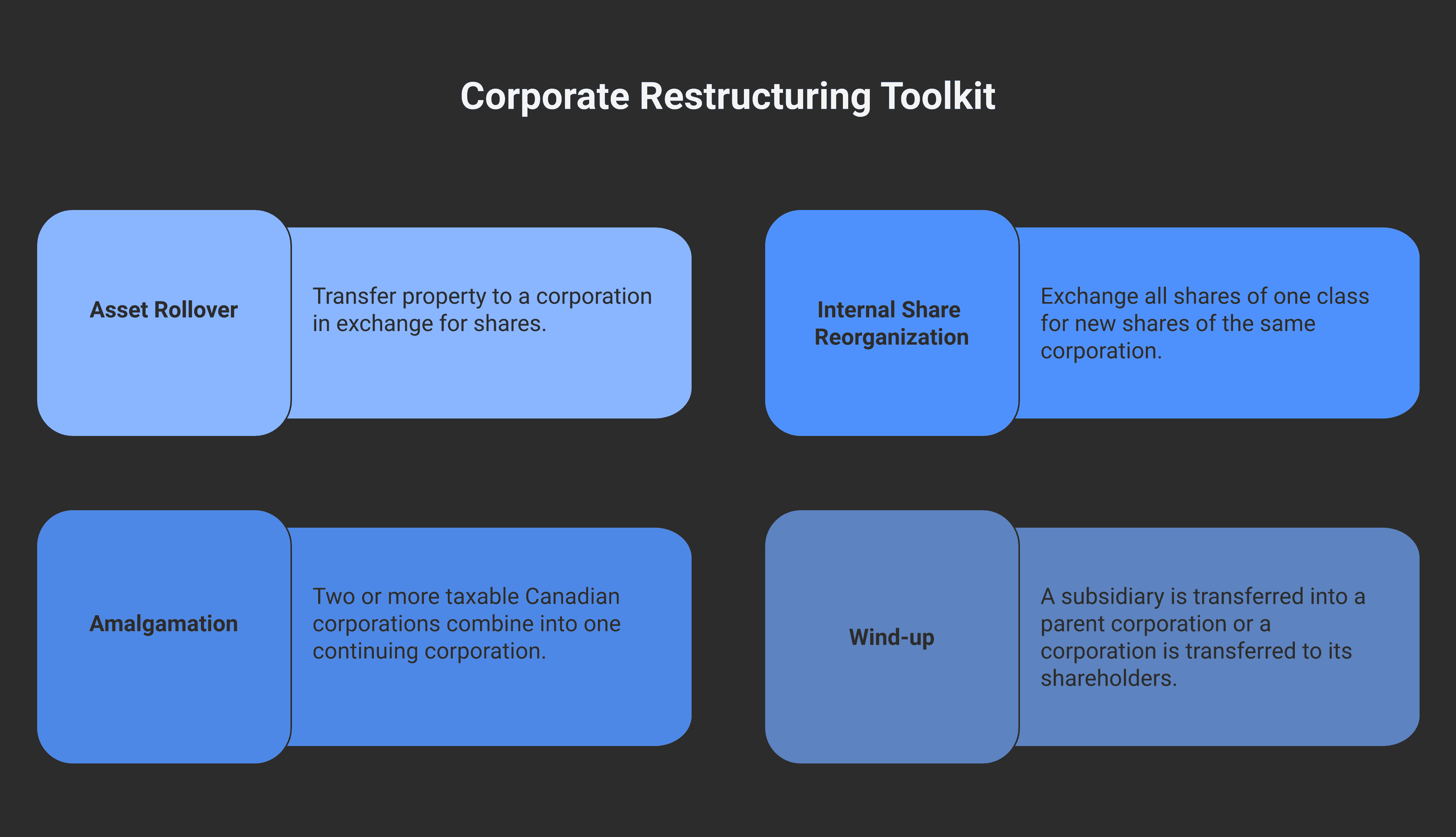

Section 85 — rollover of property from a person to a corporation in exchange for shares (and optional non-share consideration "boot"). Used for estate freezes (section 85 path), pre-sale restructuring, asset reorganizations, and contributions to holdco structures.

Section 86 — internal share reorganization within an existing corporation. Used primarily for estate freezes (section 86 path) and for restructuring share classes.

Section 87 — amalgamation of two or more taxable Canadian corporations into a single continuing corporation. Used for combining sister companies, simplifying complex structures, and acquiring sub-corporations.

Section 88 — wind-up of a corporation. Section 88(1) for vertical wind-ups (subsidiary into parent); section 88(2) for horizontal wind-ups (corporation into shareholders).

Each section provides tax-deferred treatment when properly executed — but each has specific eligibility requirements, election obligations, and post-transaction tracking. Improper structuring can convert what should be tax-deferred into a fully taxable disposition.

Section 85 — Asset rollover to a corporation

Section 85 of the Income Tax Act lets a person transfer property to a corporation in exchange for shares (and optional non-share consideration up to ACB) without triggering immediate capital gains tax.

Eligible transferors: individuals (including estates and trusts), partnerships, and corporations.

Eligible property: capital property, eligible capital property, certain inventory, real property used in active business.

The mechanic:

Transferor and transferee corporation jointly elect to use section 85

Election (Form T2057) specifies the agreed amount — the deemed proceeds of disposition

The agreed amount must be:

At least equal to the property's ACB (so no capital loss is triggered)

Not exceed the property's FMV (so no capital gain is triggered above intended)

The corporation issues at least one share as consideration

Boot (non-share consideration like cash or promissory note) can be received up to the agreed amount

Common use cases:

Estate freeze (section 85 path) — owner rolls operating co shares into new holdco, receiving preferred shares at frozen value

Pre-sale restructuring — separate active business assets from passive holdings before sale

QSBC purification — move non-active assets into a sister corporation to qualify operating co for QSBC LCGE

Holdco implementation — set up holdco structure from existing operating co shares

The flexibility of the agreed amount makes section 85 the most-used corporate reorganization tool in Canadian tax practice. The election deadline is generally on or before the tax return filing deadline for the transferor's tax year of the rollover.

Section 86 — Internal share reorganization

Section 86 of the Income Tax Act provides automatic rollover treatment when a shareholder exchanges all of a particular class of shares for new shares of the same corporation (and optionally non-share consideration).

The mechanic:

Shareholder exchanges all old shares of a class for new shares of the same corporation

New shares can have different rights, restrictions, redemption value, etc.

Section 86 automatically applies — no election needed

The shareholder's cost base in the new shares equals the old cost base

Optional non-share consideration (boot) is treated as a "deemed disposition for FMV"

Common use cases:

Estate freeze (section 86 path) — owner converts existing common shares into fixed-value preferred shares

Share recapitalization — restructure share classes for governance or family planning purposes

Preferred share creation — issue new preferred class to enable freezing or specific rights

Section 86 is simpler than section 85 (automatic rather than election-driven), but requires that the shareholder is exchanging all of the relevant class. Partial exchanges don't qualify.

Section 87 — Amalgamation

Section 87 of the Income Tax Act governs amalgamations — the combining of two or more taxable Canadian corporations into a single continuing corporation.

Requirements:

All amalgamating corporations are taxable Canadian corporations

All shareholders of each amalgamating corporation receive shares (or property, in certain triangular structures) of the amalgamated corporation

The amalgamated corporation continues the assets, liabilities, and tax attributes of the amalgamating corporations

Common use cases:

Sister company combination — combine two sister corps under common ownership to simplify structure

Acquisition post-merger — buyer's holdco and target operating co amalgamate after share acquisition

Pipeline transaction completion — pipeline structure typically completes with an amalgamation step

Simplification of complex multi-corp structures

The amalgamated corporation succeeds to the tax attributes (tax pools, GRIP/LRIP balances, capital cost balances, etc.) of the amalgamating corporations. CRA accepts the amalgamation as a tax-neutral event when the section 87 requirements are met.

Section 88 — Wind-up

Section 88 of the Income Tax Act governs corporate wind-ups — the legal dissolution of a corporation with assets distributed to its shareholders. Two main subsections:

Section 88(1) — Vertical wind-up

A subsidiary corporation is wound up into its parent corporation (a separate parent that owns ≥90% of the subsidiary's shares).

Common use cases:

Subsidiary becomes redundant after a parent acquisition

Holdco wants to absorb an operating subsidiary

Simplification post-restructuring

Tax mechanic: the parent inherits the subsidiary's assets at the subsidiary's cost base (general rule under s.88(1)). Tax attributes (loss pools, GRIP, etc.) flow through to the parent.

Section 88(2) — Horizontal wind-up

A corporation is wound up directly to its shareholders (typically individuals or a parent that doesn't qualify for 88(1) treatment).

Common use cases:

Single-owner CCPC wound up to its shareholder

Holdco wound up with assets distributed to multiple shareholders

Post-sale wind-up of acquired corporation

Tax mechanic: deemed disposition of assets at FMV (more complex than 88(1)), with potential capital gains and recapture triggered. Less tax-efficient than 88(1).

"Which tool for which problem" matrix

Goal | Primary tool | Secondary considerations |

|---|---|---|

Estate freeze, simple structure | Section 86 | Section 85 if new holdco preferred |

Estate freeze, with new holdco | Section 85 | Combined with family trust |

Pre-sale QSBC purification | Section 85 | Move passive assets to sister corp |

Combine sister corporations | Section 87 (amalgamation) | Vertical wind-up under 88(1) if parent-sub |

Wind up redundant subsidiary | Section 88(1) — vertical wind-up | Section 87 amalgamation if combining functions |

Wind up single-owner CCPC | Section 88(2) — horizontal wind-up | Tax-efficiency consideration on deemed FMV |

Pre-sale separation of assets | Section 85 | Combined with section 22 for AR in deal |

Pipeline post-mortem | Section 88(1) typically | Combined with section 87 amalgamation |

Spin-off (one corp into two) | Section 85 + section 88(2) | Or specific spin-off election |

For Modern Axis client engagements involving corporate restructuring, the typical workflow is: identify the structural goal → select the appropriate tool from the four sections → prepare election documents and corporate amendments → execute → confirm tax-pool succession → maintain ongoing tracking.

Common combinations

Real corporate restructurings often combine multiple tools:

Estate freeze with section 85 + section 86. Owner uses section 85 to roll operating co into a new holdco, then uses section 86 internal reorganization within the holdco to issue different share classes. Common for sophisticated freezes with multiple generations of beneficiaries.

Pipeline transaction using section 88(1) wind-up. Post-mortem estate pipelines often complete with a section 88(1) vertical wind-up — Newco (owned by beneficiaries) absorbs the deceased's holdco, distributing assets to beneficiaries.

Combined sister-company amalgamation (section 87) followed by parent wind-up (section 88). Multi-stage simplification of corporate group structures.

Pre-sale section 85 + sale + post-sale section 88(2). Pre-sale restructuring under section 85 to purify QSBC status, then share sale, then wind-up of the now-acquired sub via section 88(2) under the buyer's structure.

Key cautions

Section 85 elections must be filed on time. The election (Form T2057) is due on the earliest tax return filing deadline of the transferor or transferee for the year of the rollover. Late-filed or amended elections that CRA accepts carry a penalty under subsection 85(8) equal to the lesser of (a) 1/4 of 1% of the amount by which the property's fair market value exceeds the agreed amount, for each month or part of a month from the original due date until the election is filed, and (b) $100 multiplied by the number of those months, to a maximum of $8,000.

Section 86 requires ALL of the relevant share class be exchanged. Partial exchanges don't qualify and trigger deemed FMV dispositions.

Section 87 amalgamation requires real continuity. All shareholders of amalgamating corps must receive shares (or qualifying triangular consideration) of the amalgamated corporation. Failure of the continuity requirement converts the transaction into something other than a clean section 87 amalgamation.

Section 88(1) requires the parent to own at least 90% of the issued shares of each class of the sub's capital stock. Below 90%, the transaction must use section 88(2) or another mechanism.

Tax-attribute succession is automatic under section 87 and section 88(1) — but the corporation must continue to comply with the conditions of those attributes (e.g., associated-corp rules for the SBD, holding-period rules for the LCGE on QSBC shares).

For owner-manager planning, the most common restructurings — estate freezes, holdco implementations, sister-corp amalgamations — fit cleanly into the four tools. More complex transactions (cross-border restructurings, public-company spin-offs, distressed restructurings) may require additional provisions and elections beyond the basic four sections.

Frequently asked questions

What are sections 85, 86, 87, and 88 of the Income Tax Act?

These are the four main corporate reorganization provisions in Canadian tax law. Section 85 governs the tax-deferred transfer of property to a corporation in exchange for shares (plus optional boot). Section 86 governs internal share reorganizations (exchanging old shares for new shares of the same corporation). Section 87 governs amalgamations (combining two or more taxable Canadian corporations into one). Section 88 governs corporate wind-ups (vertical 88(1) for parent-subsidiary; horizontal 88(2) for general). Each provides tax-deferred treatment when properly executed.

When should I use section 85 vs section 86?

Section 86 is appropriate when the reorganization is internal to one corporation (exchanging share classes within the same corp). Section 85 is appropriate when transferring property between persons and corporations — typically setting up a new holding company or restructuring across multiple corporate entities. For an estate freeze, both paths exist: section 86 keeps everything in one corp; section 85 implements a new holdco structure. The choice depends on whether the owner wants the structural separation a holdco provides.

What is a section 87 amalgamation?

A section 87 amalgamation is the combining of two or more taxable Canadian corporations into a single continuing corporation. All shareholders of each amalgamating corp receive shares of the amalgamated corp (in qualifying ratios). The amalgamated corp inherits all tax attributes — capital cost balances, GRIP/LRIP pools, RDTOH balances, loss pools, etc. Amalgamations are commonly used to combine sister companies, simplify complex corporate structures, or complete pipeline-style transactions.

What's the difference between vertical and horizontal wind-up?

A vertical wind-up under section 88(1) is when a subsidiary corporation is wound up into its parent corporation (the parent must own at least 90% of the issued shares of each class of the sub's capital stock). The parent inherits the sub's assets at the sub's cost base. A horizontal wind-up under section 88(2) is when a corporation is wound up to its shareholders directly (no parent-sub relationship). Section 88(2) wind-ups trigger deemed FMV dispositions and are less tax-efficient than 88(1) wind-ups.

Does section 87 amalgamation flow through tax attributes?

Yes. The amalgamated corporation succeeds to the tax attributes (loss pools, GRIP, LRIP, RDTOH balances, capital cost allowance balances, etc.) of all amalgamating corporations. This is one of the main reasons amalgamation is used for corporate group simplification — the tax history flows through cleanly. However, the amalgamated corp must continue to comply with the conditions of those attributes (e.g., associated-corp rules for SBD, holding-period rules for LCGE on QSBC shares).

What is Form T2057 and when is it due?

Form T2057 is the joint election form for section 85 rollovers, filed by the transferor and transferee corporation. It specifies the "agreed amount" — the deemed proceeds of disposition for the property transferred. The election is due on the earliest tax return filing deadline of either the transferor or the transferee for the year of the rollover. Late-filed elections face escalating penalties under subsection 85(7).

Can I combine sections 85 and 86 in one estate freeze?

Yes — combined section 85 + section 86 freezes are common for sophisticated estate planning. The owner uses section 85 to roll operating-co shares into a new holdco; section 86 internal reorganization within the holdco then creates the new preferred and common share classes for the family trust to subscribe to. This combination provides structural separation (via the new holdco) and the share-class flexibility (via section 86) needed for multi-generation planning.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA