Capital Gains Tax Canada 2026: Where the Rate Actually Landed

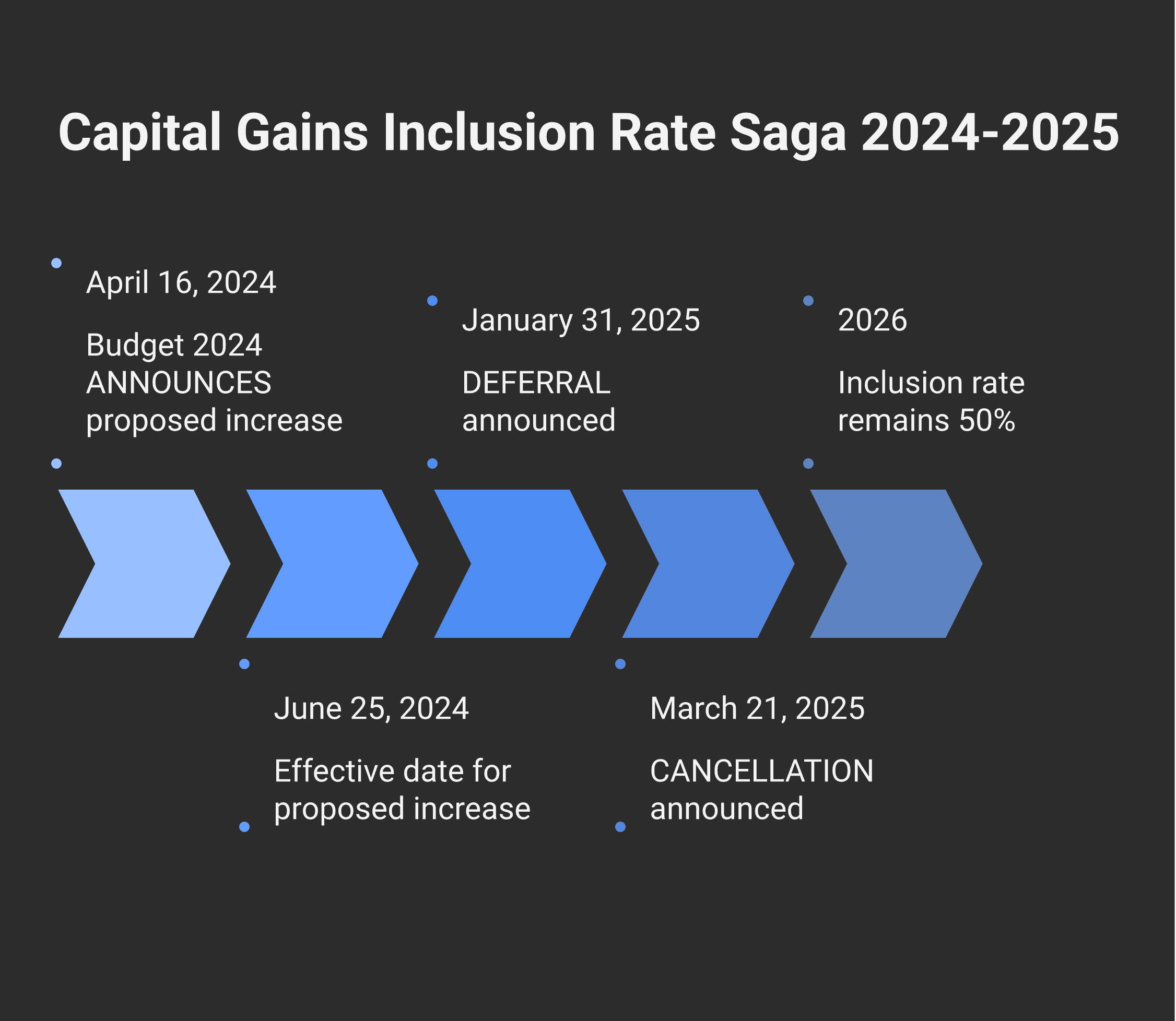

The Canadian capital gains tax landscape went through more change between April 2024 and March 2025 than in the prior two decades combined — and ended up almost exactly where it started. The 2024 Federal Budget proposed raising the capital gains inclusion rate from 1/2 to 2/3 for gains above $250,000 for individuals (and on all corporate and most trust gains) effective June 25, 2024. Markets, accountants, and planners pivoted hard. The federal government deferred the increase to January 1, 2026 on January 31, 2025. Then on March 21, 2025, the new Carney government cancelled the increase altogether.

The net result for 2026: the inclusion rate is 50% — the same as 2023, as 2010, as 1990. The 2024 proposal is gone. The Lifetime Capital Gains Exemption increase from roughly $1.02M to $1.25M (effective June 25, 2024) was kept and is now indexed to inflation, sitting at $1,275,000 for 2026.

This guide walks through how capital gains tax actually works in 2026 — the 50% inclusion rate under section 38 of the Income Tax Act, how to calculate a gain, the multi-year capital gains reserve, the principal residence exemption, the LCGE intersection, deemed disposition on death and emigration, and the corporate capital dividend account that ties it all together.

Key takeaways

For 2026, the capital gains inclusion rate is 50% under paragraph 38(a) of the Income Tax Act — confirmed unchanged after the 2024 proposal to raise to 2/3 was deferred (January 2025) then cancelled (March 2025).

A capital gain is taxed at the filer's marginal rate on 50% of the gain. For a top-bracket Ontario filer in 2026, the combined federal-and-provincial rate on capital gains is approximately 26.76% — half of the 53.53% ordinary income rate.

The Lifetime Capital Gains Exemption for 2026 is $1,275,000 under section 110.6, indexed from the $1.25M established by the 2024 Federal Budget effective June 25, 2024. The LCGE applies to qualifying small business corporation (QSBC) shares and qualifying farm and fishing property (QFFP).

The principal residence exemption under paragraph 40(2)(b) eliminates capital gains on a designated principal residence, prorated by years of qualifying use.

A capital gains reserve under subparagraph 40(1)(a)(iii) lets sellers receiving proceeds over multiple years spread the gain across up to 5 years (10 years for some intergenerational transfers). The minimum annual recognition is 20% of the gain regardless of proceeds collected.

Donations of publicly listed securities to a registered charity have a 0% inclusion rate under paragraph 38(a.1) — the donor gets the full charitable receipt and pays no capital gains tax on the donated shares.

How a capital gain is calculated

A capital gain arises when you dispose of capital property for more than its adjusted cost base. The formula under section 40 of the Income Tax Act:

Capital gain = Proceeds of disposition − Adjusted cost base (ACB) − Selling costs

Each component:

Proceeds of disposition. Usually the cash sale price plus the FMV of any non-cash consideration. For deemed dispositions (death, emigration, gift), it's the FMV at the deemed-disposition moment.

Adjusted cost base (ACB). Usually purchase cost plus capitalised improvements, transaction costs, and certain other adjustments. For property received as a gift or inheritance, ACB starts at FMV at the date of acquisition by the recipient (unless a rollover applied).

Selling costs. Real estate commissions, legal fees on sale, transfer taxes paid by the seller, and similar amounts directly tied to the disposition.

The taxable portion is then 50% of the capital gain under paragraph 38(a). That taxable capital gain is added to other income on the T1 (or T2 for corporations) and taxed at the relevant marginal rate.

The 50% mechanic means capital gains are always taxed at exactly half the rate of ordinary income for the same filer. For a top-bracket Ontario filer in 2026, ordinary income at 53.53% means capital gains at 26.76% — a meaningful tax-rate advantage that drives a lot of investment planning. See our Canada tax brackets guide for the combined federal-and-provincial rate table across all 13 provinces and territories.

Capital gains reserve — spreading the gain over multiple years

When sale proceeds are received over multiple years (vendor takeback financing, instalment sales, family business transitions), subparagraph 40(1)(a)(iii) allows a capital gains reserve that defers the unrealised portion of the gain.

Standard 5-year reserve. The maximum reserve in any year is the lesser of:

Proceeds not yet received ÷ Total proceeds × Capital gain

20% of the gain × (4 − number of preceding years ending after the disposition)

Practical effect: at least 20% of the gain must be recognised each year, starting in the year of disposition. By year 5, the entire gain is recognised regardless of whether all proceeds have been collected.

Extended 10-year reserve for specific scenarios:

Transfers of family-farm or fishing property to a child under subsection 73(3)

Transfers of qualifying small business corporation shares between parent and child (subsection 73(4))

Transfers under a qualifying cooperative conversion

The 10-year reserve is one of the most valuable planning tools for owner-managers transferring a business to the next generation. Combined with the LCGE multiplication through a family trust, the after-tax economics of intergenerational business transfer have improved materially since 2024.

Principal residence exemption

A designated principal residence is exempt from capital gains tax under paragraph 40(2)(b). Mechanically, the deemed disposition still occurs and the capital gain is still calculated — but the exemption fully offsets it. The PRE formula:

Exempt portion = Capital gain × (1 + years designated as principal residence) ÷ years of ownership

The "1 +" gives a one-year bonus that simplifies the math when a family moves mid-year. The formula prorates the exemption when the home was the principal residence for only part of the ownership period (e.g., rented out for some years, used personally for others).

One principal residence per family unit per year. A married couple can designate only one property — the cottage, the city home, the secondary condo. The designation is made by the executor on Form T1255 or T2091 when the property is sold or deemed disposed.

For a deep dive on the principal residence exemption's interaction with CCA recapture, the anti-flipping rule, and the change-of-use election, see our real estate tax guide.

Lifetime Capital Gains Exemption (LCGE)

The LCGE under section 110.6 of the Income Tax Act shelters capital gains on the disposition of qualifying property — up to a lifetime limit per individual.

2026 LCGE limit: $1,275,000, indexed from the $1.25M established by Budget 2024 effective June 25, 2024.

Qualifying property:

Qualified small business corporation (QSBC) shares — shares in a Canadian-controlled private corporation that meet a multi-part test (90% active business assets in Canada or used in active business of a related corporation, etc.)

Qualified farm or fishing property (QFFP) — land, buildings, fishing boats and licences, and shares in family-farm/fishing corporations meeting specific conditions

We cover the QSBC qualification mechanics and purification strategies in our LCGE guide. The combined federal-plus-provincial benefit of the LCGE in 2026 — full $1.275M sheltered for a top-bracket owner — is approximately $341,000 in tax savings in Ontario or BC.

Capital losses — what you can offset and when

When ACB exceeds proceeds, the result is a capital loss. Loss treatment:

Capital losses can only offset capital gains (not ordinary income, in most circumstances)

Excess losses can be carried back 3 years (T1A request) or carried forward indefinitely

Net capital losses apply against taxable capital gains, not gross capital gains — i.e., loss inclusion is also 50%

Superficial loss rule under section 54 of the Income Tax Act, and applied by subparagraph 40(2)(g)(i): a capital loss is deemed nil if the taxpayer (or an affiliated person) acquires the same or identical property in the period beginning 30 days before and ending 30 days after the disposition and still owns it at the end of that period. This blocks the obvious tax-loss harvest involving an immediate repurchase. The denied loss is added to the ACB of the replacement security and is effectively deferred until the replacement is sold without a superficial-loss trigger.

Allowable business investment loss (ABIL) under section 38(c): a special category where a capital loss on shares (or debt) of a small business corporation can offset ordinary income, not just capital gains. ABILs are a meaningful planning lever when a small business goes under.

Deemed disposition — death and emigration

Capital property is deemed disposed of at FMV under subsection 70(5) when:

The owner dies (covered in our inheritance tax guide)

The owner emigrates from Canada (becomes a non-resident) under subsection 128.1(4) — this is the departure tax

For emigration specifically: when an individual becomes a non-resident of Canada, they're deemed to have disposed of all capital property at FMV (subject to specific exclusions: Canadian real estate, RRSPs/RRIFs, certain pensions, and a small list of others). The resulting capital gains are reported on the final Canadian tax return as a Canadian resident.

There's a deferral election under subsection 220(4.5) — security can be posted with CRA to defer payment of the departure-tax liability until the property is actually sold. Useful where the emigrating filer expects to eventually sell.

Corporate capital gains and the Capital Dividend Account

When a Canadian-controlled private corporation realises a capital gain, the non-taxable half (50%) flows into the Capital Dividend Account (CDA) under subsection 89(1). From the CDA, the corporation can pay a tax-free capital dividend to shareholders under subsection 83(2) by filing Form T2054.

The mechanic preserves integration: the corporation pays tax on its 50% taxable portion (at the corporate refundable tax rate that gets recovered when dividends are paid), the other 50% becomes tax-free distributable balance, and the net effect approximates what the shareholder would have paid by holding the asset personally.

We cover the CDA mechanics in detail in our Capital Dividend Account guide.

For owner-managers, the corporate-vs-personal decision on holding appreciating assets often turns on the CDA flow-through. A holdco that realises capital gains and immediately pays a capital dividend produces nearly identical after-tax results to the owner holding the asset personally — but with the asset protection and estate flexibility a corporate structure provides.

Donations of publicly listed securities — the 0% inclusion rate

Under paragraph 38(a.1) of the Income Tax Act, the taxable capital gain on the donation of a publicly listed security to a registered charity is zero. The donor:

Pays no capital gains tax on the donated shares (vs the standard 50% inclusion if sold for cash)

Receives a full charitable donation receipt for the FMV of the donated shares

Gets a federal charitable donation tax credit on the receipt amount

The math: a high-bracket Ontario filer donating $100K of publicly listed shares with a $30K ACB pays no tax on the $70K gain (a saving of $18,700 in tax) AND gets a charitable credit on the $100K ($50K combined federal-provincial tax reduction). The net cost of donating $100K of appreciated stock is well under $50K — among the most efficient charitable giving structures available.

Qualifying securities: publicly listed shares, bonds, ETFs, mutual fund units, and certain partnership interests. Private company shares do not qualify unless a specific in-kind donation programme is used.

Common planning moves

Use the LCGE on QSBC shares as part of a multi-year plan. Most QSBC sales require purification — removing passive assets from the corporation so it qualifies as a small business corporation throughout the holding period. We walk through purification and the 24-month holding-period test in our LCGE guide.

Harvest losses against gains within the same year. Losses denied in a year can be carried forward — but matching them to a gain in the same year is more economically efficient because they reduce the immediate tax, not future tax.

Time large gains around the December 31 year-end. Realising a large capital gain in late December rather than early January typically accelerates the tax payment by 12+ months. Where possible, defer the realisation to January 1.

Avoid the superficial loss trap. When tax-loss harvesting in a non-registered account, ensure that the same security is not repurchased by you (or an affiliated person — spouse, controlled corporation, RRSP, TFSA) within 30 days before or after the disposition.

For owner-managers, coordinate corporate capital gains with the CDA distribution. A pattern of realise-gain → pay capital dividend → recapitalise is sometimes more efficient than holding gains in the corporation forever.

For tax planning at Modern Axis, capital gains planning is a recurring annual engagement — typically synchronised with year-end portfolio review for non-registered holdings, QSBC purification for owner-managers, and CDA distribution timing for corporate investors. The 2024-2025 inclusion rate saga is fully behind us, the rate is settled at 50%, and the planning principles are durable again.

Frequently asked questions

What is the capital gains tax rate in Canada for 2026?

Capital gains are taxed at 50% of the filer's marginal rate under paragraph 38(a) of the Income Tax Act — meaning capital gains are always taxed at half the rate of ordinary income for the same filer. For a top-bracket Ontario filer, that's approximately 26.76% (half of the 53.53% ordinary rate). The 2024 proposal to raise the inclusion rate to 2/3 for gains above $250,000 was deferred in January 2025 and cancelled on March 21, 2025.

What is the Lifetime Capital Gains Exemption for 2026?

The LCGE for 2026 is $1,275,000 under section 110.6 of the Income Tax Act, indexed from the $1.25M increase established by Budget 2024 effective June 25, 2024. The LCGE applies to qualifying small business corporation (QSBC) shares and qualifying farm and fishing property (QFFP). At top combined marginal rates in Ontario or BC, the full LCGE shelters approximately $341,000 of federal-plus-provincial capital gains tax.

How is a capital gain calculated in Canada?

Capital gain = Proceeds of disposition − Adjusted cost base − Selling costs. The taxable portion is 50% of the capital gain under paragraph 38(a) of the Income Tax Act. The taxable amount is added to other income and taxed at the filer's marginal rate. Adjusted cost base is usually purchase cost plus capitalised improvements and transaction costs.

What is the capital gains reserve and how many years does it span?

A capital gains reserve under subparagraph 40(1)(a)(iii) of the Income Tax Act lets sellers receiving proceeds over multiple years defer the unrealised portion of the gain. The standard reserve spans 5 years (4 carry years plus the year of disposition), with a minimum 20% recognition each year. An extended 10-year reserve applies to qualifying intergenerational transfers of family farm/fishing property and QSBC shares to a child.

Do I pay capital gains tax on my principal residence?

Generally no. The principal residence exemption under paragraph 40(2)(b) of the Income Tax Act eliminates the capital gain on a designated principal residence, prorated by years of qualifying use. The designation is made by the homeowner (or executor) on Form T1255 or T2091. A family unit can designate only one principal residence per year. If the home was rented out for part of the ownership period, the exemption is prorated.

Can I offset capital gains with capital losses?

Yes. Capital losses can offset capital gains in the same year. Excess capital losses can be carried back 3 years (request via Form T1A) or carried forward indefinitely. The matching is 50:50 — loss inclusion is also 50%. Capital losses generally cannot offset ordinary income, except in the case of an Allowable Business Investment Loss (ABIL) under paragraph 38(c) for losses on shares or debt of a small business corporation.

How do I donate stock to charity tax-free?

Donations of publicly listed securities (shares, bonds, ETFs, mutual fund units) to a registered charity have a 0% capital gains inclusion rate under paragraph 38(a.1) of the Income Tax Act — meaning no capital gains tax on the appreciation of the donated shares. The donor also receives a charitable donation receipt for the FMV of the donated securities, which generates a charitable donation tax credit at the donor's combined federal-plus-provincial rate. This is one of the most tax-efficient charitable giving structures available in Canada.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA