Capital Dividend Account: Tax-Free Dividends from Your CCPC

If you own a Canadian-controlled private corporation, the Capital Dividend Account is one of the most valuable lines on the balance sheet — and one of the most consistently overlooked. It is a notional account, meaning it does not show up on the financial statements at all, but it exists for every CCPC the moment the corporation is incorporated. What sits in it is the amount the corporation can distribute to its shareholders tax-free — and the moment you stop tracking it, you usually start losing money.

Key takeaways

The Capital Dividend Account is a notional balance under subsection 89(1) that lets a CCPC distribute its tax-free amounts — mainly the non-taxable half of capital gains and life insurance death benefits — out to shareholders tax-free.

Form T2054 must be filed under subsection 83(2) on or before the earlier of the day the dividend becomes payable and the day it is paid — late or missing election turns the dividend into ordinary taxable income.

The CDA balance runs cumulatively across the corporation's life; capital losses reduce future capital-gain additions, so poor tracking can leave money on the table or trigger excess-tax exposure.

An excess election triggers Part III tax under section 184 at 60% of the excess, with a 90-day window to elect under 184(3) to recharacterise the excess as a taxable dividend.

This post is about what the CDA is, what gets added to it, how the T2054 election works, what happens if you designate more than the balance, and where the most expensive mistakes live. The mechanic is governed by subsection 89(1) of the Income Tax Act (the CDA definition) and subsection 83(2) (the capital dividend election).

The rule, in one sentence

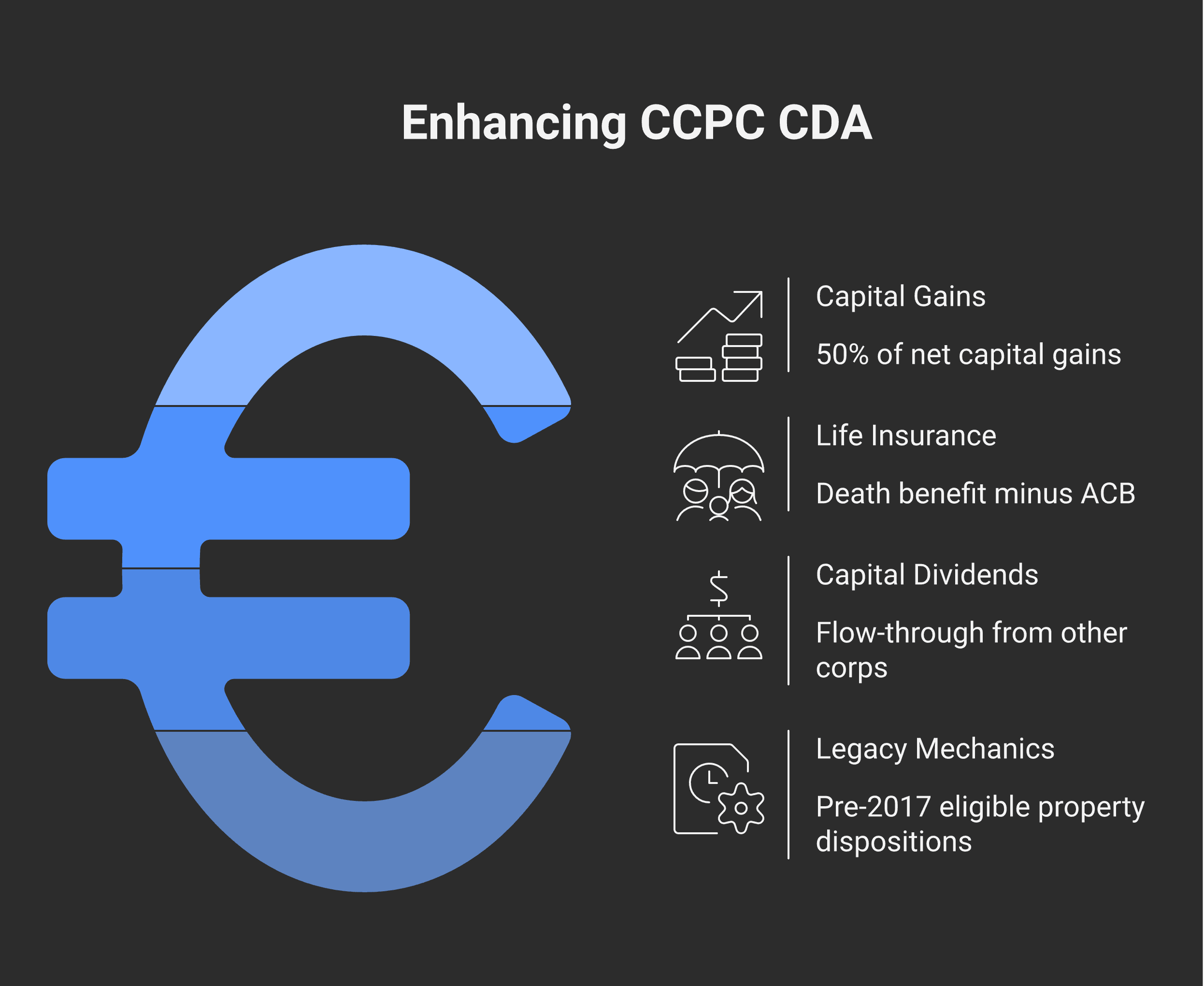

Under subsection 89(1), the Capital Dividend Account of a Canadian-controlled private corporation is a running cumulative balance that tracks the non-taxable half of capital gains realised, life insurance proceeds received in excess of policy ACB, capital dividends received from other corporations, and certain other tax-free receipts; under subsection 83(2), the corporation may elect by filing Form T2054 to designate a dividend (up to that balance) as a capital dividend, which the recipient shareholder receives tax-free.

The rule is straightforward. The places it breaks are entirely in execution.

What goes into the CDA

The CDA additions are listed in subsection 89(1) — the operative paragraphs (a) through (g) — but in practice four sources cover almost everything that lands there:

Source 1: The non-taxable half of capital gains

When a CCPC realises a capital gain, the taxable portion (currently 50%) flows to taxable income. The non-taxable portion (also 50%) is added to the CDA. This is the most common CDA addition and the one to design corporate investment strategy around.

The subtlety: capital losses reduce the addition. Specifically, the CDA addition is calculated cumulatively as 50% of the corporation's net capital gain across all years — meaning if you have a $100,000 gain in 2026 and a $40,000 capital loss in the same year, the CDA addition is 50% × $60,000 = $30,000, not 50% × $100,000.

In practice, this means a corp with a history of trading losses has a smaller CDA addition for any given gain than a corp with a clean record. Tracking the corporation's cumulative net capital gain history is what allows the CDA balance to be calculated accurately.

Source 2: Life insurance proceeds

When a corporation owns a life insurance policy and the insured dies, the death benefit lands in the corporation. The amount added to the CDA is the death benefit minus the policy's adjusted cost basis (ACB).

Policy ACB is a separate concept (under subsection 148(9) of the Act) and tracks the cumulative premiums paid less the net cost of pure insurance — it grows in the early years of a permanent policy and may shrink toward zero in later years. For a long-held permanent policy, the ACB is often a small fraction of the death benefit, meaning almost the entire payout flows to CDA.

This is the foundational mechanic in corporate-owned-life-insurance estate planning. A $2 million death benefit on a corp-owned policy might generate $1.95 million of CDA, which can then be distributed to surviving shareholders or the estate as a tax-free capital dividend.

Source 3: Capital dividends received from another private corp

If your operating company holds shares of another private corp (a sister company, a holdco, an investment), and that company pays a capital dividend, the dividend flows into the recipient corp's CDA — without further tax. This is what allows capital dividends to move through holding-company structures without losing their tax-free character.

Source 4: Pre-2017 eligible capital property residuals

The rules around goodwill and other eligible capital property changed in 2017. Dispositions before the changeover added non-taxable amounts to the CDA under the old rules. For corporations that disposed of goodwill in the pre-2017 regime, residual CDA balances from those events may still be on the books.

What does NOT go into the CDA

The list of CDA additions is closed. Common items that do not add to the CDA:

Active business income (it's already taxed, but it's taxable income, not non-taxable)

Dividends from public corporations

Eligible dividends or non-eligible dividends received from any private corp (only capital dividends pass through)

The principal balance of a corp-held investment portfolio

Refundable Dividend Tax on Hand (RDTOH) — entirely separate mechanic

General Rate Income Pool (GRIP) — also separate; tracks eligible-dividend capacity

The CDA is specifically a non-taxable-receipts tracker. If the corp paid tax on it, it doesn't go to CDA.

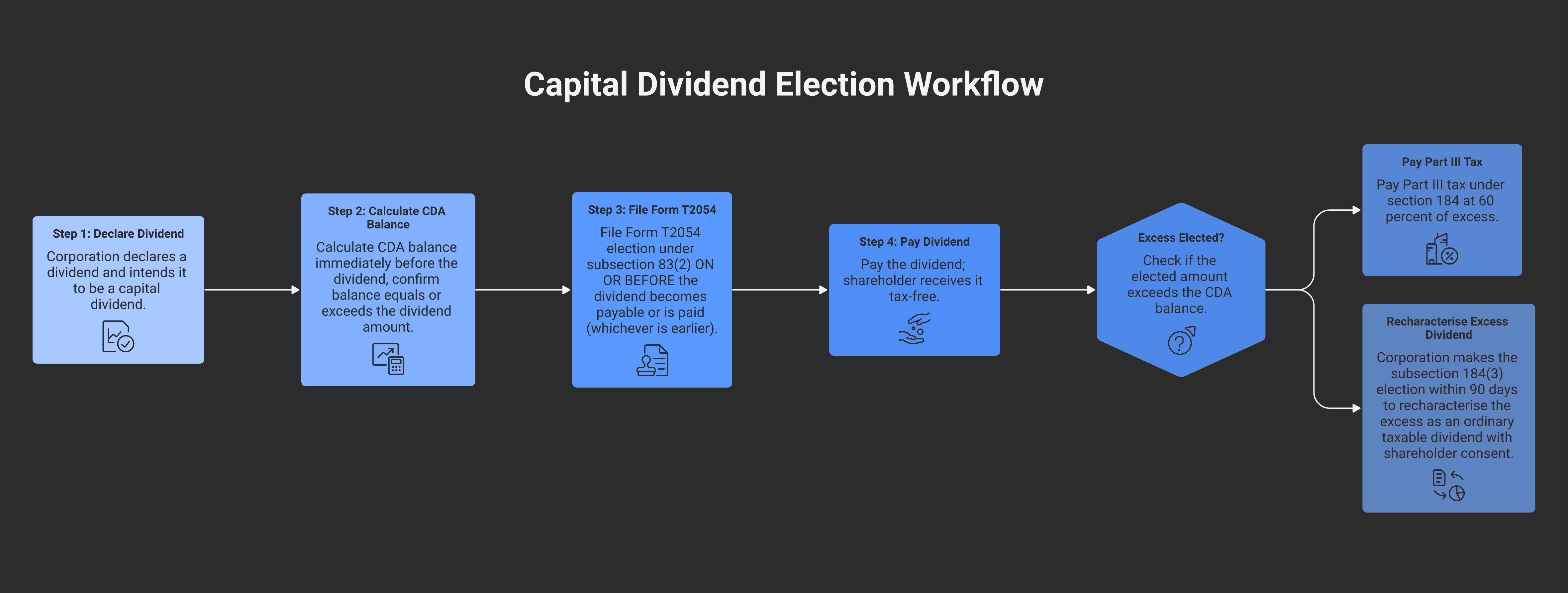

How to actually pay a capital dividend — Form T2054

Declaring the dividend is not enough. The corporation must elect under subsection 83(2) by filing Form T2054 (Election to Designate a Dividend as a Capital Dividend) on or before the earlier of:

The day the dividend becomes payable, OR

The day the dividend is paid

If the dividend is paid on June 1 and the T2054 is not filed by June 1, the election is late — and the dividend is treated as ordinary taxable.

The Form T2054 requires:

The corporation's name, business number, year-end

The amount of the capital dividend being elected

A certified statement of the CDA balance immediately before the election

A directors' resolution authorising the dividend and the election

A schedule showing the CDA calculation

The CDA balance calculation has to be airtight. The CRA reads T2054s carefully and will request a CDA reconciliation for any non-trivial election. Errors in the balance calculation create the excess-election problem below.

The excess election problem — Part III tax under section 184

If the corporation elects a capital dividend in an amount greater than the actual CDA balance immediately before the election, the excess triggers Part III tax under section 184. The rate is 60% of the excess — meaningfully higher than the personal tax that would have applied to the same amount as an ordinary taxable dividend.

The intent of the punitive rate is to deter careless or aggressive CDA elections — the corporation has to genuinely have the balance available.

The escape: subsection 184(3) election. Within 90 days of being assessed Part III tax (or earlier — within 90 days of being notified that the election will be assessed), the corporation may elect to recharacterise the excess portion as a separate taxable dividend paid in addition to (or instead of) the capital dividend originally intended. The 184(3) election requires:

Written consent of every shareholder who received the over-elected amount

The recharacterisation reclassifies the excess as a regular dividend, taxable in the shareholder's hands at normal dividend rates

If the 184(3) election is made on time, no Part III tax. If it's missed, the 60% rate applies on the excess.

Why the CDA matters in estate planning

The most powerful use of the CDA in practice is moving life insurance death benefits to surviving family members tax-free. The mechanic:

The corp owns a permanent life insurance policy on the owner-manager's life. Premiums are paid by the corp (non-deductible, but with cheaper after-tax dollars than personal premiums in many cases).

The owner-manager dies. The death benefit is paid to the corp.

The death benefit, net of policy ACB, lands in the corp's CDA.

The corp's directors (the surviving shareholders or executor) declare a capital dividend. T2054 is filed.

The capital dividend is paid to the estate or to the surviving shareholders — tax-free.

A $1 million death benefit on a policy with an ACB of $50,000 generates $950,000 of CDA. The surviving family receives $950,000 free of personal tax. If the death benefit had simply been kept in the corp and eventually paid out as a taxable dividend, the family would have received roughly $570,000 after dividend tax (on a top-bracket recipient in BC, non-eligible dividend rate). The CDA mechanism preserves the $380,000 spread.

This is one of the central reasons holdco + corp-owned life insurance structures appear in Modern Axis's family trust planning — the CDA flow is what makes the life-insurance leg work.

Pairing with capital gains harvesting and the LCGE

For owner-managers building investment portfolios inside an operating company or a holdco, the CDA mechanic is one of the planning levers around capital gains realisation. Strategies:

Realise gains in years where the corporation can absorb the income. Half goes to CDA; half is taxable. Distribute the CDA half tax-free to shareholders.

Trigger gains on shares of a sister corp before disposition. Especially useful in combination with the Lifetime Capital Gains Exemption on QSBC shares.

Use a holdco to receive capital dividends from operating subs, then re-distribute up the family-share chain.

Time the capital dividend declaration around year-end to align the T2054 filing with corporate tax season.

The CDA is not a one-time-use account. It can be used and replenished repeatedly across the life of the corporation.

Common mistakes

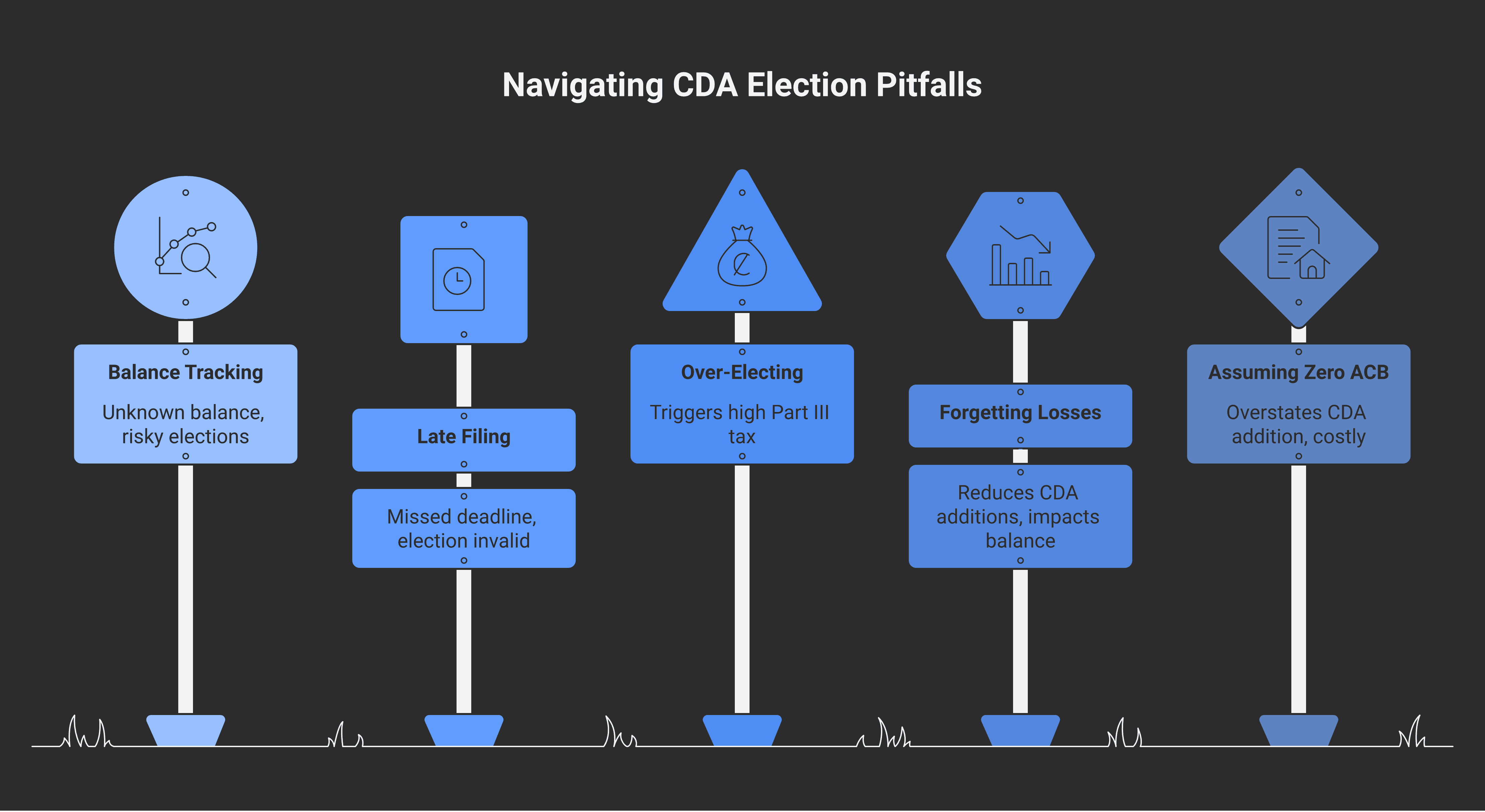

1. Not tracking the balance

The CDA does not appear on the balance sheet. Without explicit tracking, the cumulative balance is unknown. The CRA's CDA verification service (a phone-line and now online request through My Business Account) can confirm what the CRA has on file — and the discrepancy between the corp's records and the CRA's records is often the first thing to surface in a CDA review.

The fix is a CDA continuity schedule maintained year over year, with each addition and election documented. Year-end is when this should be reconciled.

2. Late T2054 filing

A dividend resolution dated June 1, paid June 5, and a T2054 filed June 10 is late — the election is invalid. The capital dividend is reclassified as an ordinary taxable dividend, eliminating the tax-free treatment.

The fix is to treat the T2054 as part of the dividend declaration package — it should be ready and filed simultaneously with the directors' resolution.

3. Over-electing the balance

Designating more than the CDA balance triggers Part III tax. The escape is the subsection 184(3) recharacterisation election within 90 days. Both are recoverable, but the cleanest path is to elect within the actual balance in the first place.

4. Forgetting capital losses reduce the addition

A corp realising a $200,000 capital gain in a year where it also realised a $50,000 capital loss adds $75,000 to CDA (50% × $150,000 net), not $100,000 (50% × $200,000). Forgetting this leads to over-claimed CDA and excess-election exposure.

5. Assuming policy ACB is zero

For a recently-issued permanent life insurance policy, the ACB may be meaningful (a couple of years of premiums paid less the cumulative net cost of pure insurance). The CDA addition is death benefit minus ACB, not the full death benefit. Get the ACB from the insurer's policy schedule before declaring.

When the CDA work lands on Modern Axis

Modern Axis CPA maintains the CDA continuity schedule for every incorporated client where the balance is material — investment-holding corporations, owner-managers with corp-owned life insurance, holdco structures absorbing capital dividends from operating subs. The Tax Planning & Compliance service covers the annual reconciliation; CDA-focused planning (timing gains realisations, sequencing distributions, pairing with the LCGE) is its own engagement scope. For incorporated owners with corp-owned life insurance, the CDA flow is one of the central pieces of estate planning — and the right time to review it is well before the policy event, not after.

Frequently asked questions

What is the Capital Dividend Account in Canada?

A notional balance maintained for every Canadian-controlled private corporation under subsection 89(1) of the Income Tax Act. It tracks tax-free amounts received by the corporation — primarily the non-taxable half of capital gains, life insurance death benefits net of policy ACB, capital dividends received from other private corporations, and certain pre-2017 eligible-capital-property amounts. A dividend designated as a capital dividend via Form T2054 is received tax-free by the shareholder, up to the CDA balance.

How do I pay a capital dividend from my corporation?

File Form T2054 (Election to Designate a Dividend as a Capital Dividend) under subsection 83(2) on or before the earlier of (a) the day the dividend becomes payable and (b) the day the dividend is paid. The election includes the amount, a CDA balance reconciliation, and a directors' resolution. If the election is filed late, the dividend is treated as an ordinary taxable dividend and the CDA strategy fails entirely.

What happens if I elect a capital dividend greater than my CDA balance?

Part III tax applies under section 184 at 60% of the excess. The escape is subsection 184(3) — within 90 days of the assessment, the corporation can elect (with shareholder consent) to recharacterise the excess as an ordinary taxable dividend. The recharacterised amount is then taxable to the shareholder at normal dividend rates, but Part III tax is avoided. The 90-day window is hard — miss it and the 60% penalty stands.

How is the CDA addition from life insurance calculated?

The death benefit received by the corporation minus the policy's adjusted cost basis (ACB) is added to the CDA. ACB is tracked by the insurer under subsection 148(9) — it represents cumulative premiums paid less the cumulative net cost of pure insurance. For long-held permanent policies, ACB is typically a small fraction of the death benefit, so most of the payout flows to CDA. For recently issued policies, ACB can be meaningful and should be confirmed before declaring a capital dividend.

Do capital losses reduce my Capital Dividend Account balance?

Yes. The CDA addition from capital gains is 50% of the corporation's net capital gain (gains minus losses). A corporation with a $200,000 gain and a $50,000 capital loss in the same period adds $75,000 to CDA, not $100,000. The cumulative net calculation runs across the corporation's history, so a poor trading year reduces future CDA additions. Tracking the balance accurately is the single biggest CDA mistake we see.

Can capital dividends flow up a holdco chain tax-free?

Yes. A capital dividend paid by a subsidiary to a parent corp lands in the parent's CDA without being treated as taxable income — preserving the tax-free character through the chain. The parent can then re-distribute up the family-share chain. This is one reason holdco structures are common in owner-manager estate planning, especially around corporate-owned life insurance, since the death benefit flows through multiple corporate layers without losing its CDA character.