Business Succession Planning for Canadian Owners 2026

Succession planning is the single most consequential tax decision most Canadian business owners ever make — and it has changed materially since 2021. The intergenerational business transfer exception under Bill C-208 (June 29, 2021) and the Bill C-59 amendments (effective January 1, 2024) reshaped the after-tax economics of selling a family business to the next generation. The lifetime capital gains exemption (LCGE) — currently $1,275,000 for 2026 — sits alongside the new immediate-transfer and gradual-transfer paths to make intergenerational transfer dramatically more attractive than it was even five years ago.

This guide walks through how Canadian business succession planning works in 2026 — the three main exit paths (family, employee/management buyout, third-party sale), the section 84.1 anti-surplus-stripping rule and its Bill C-208/C-59 carve-out, the LCGE multiplication mechanic via a family trust, the asset-vs-share-sale decision, and the typical 5-10 year planning timeline.

Key takeaways

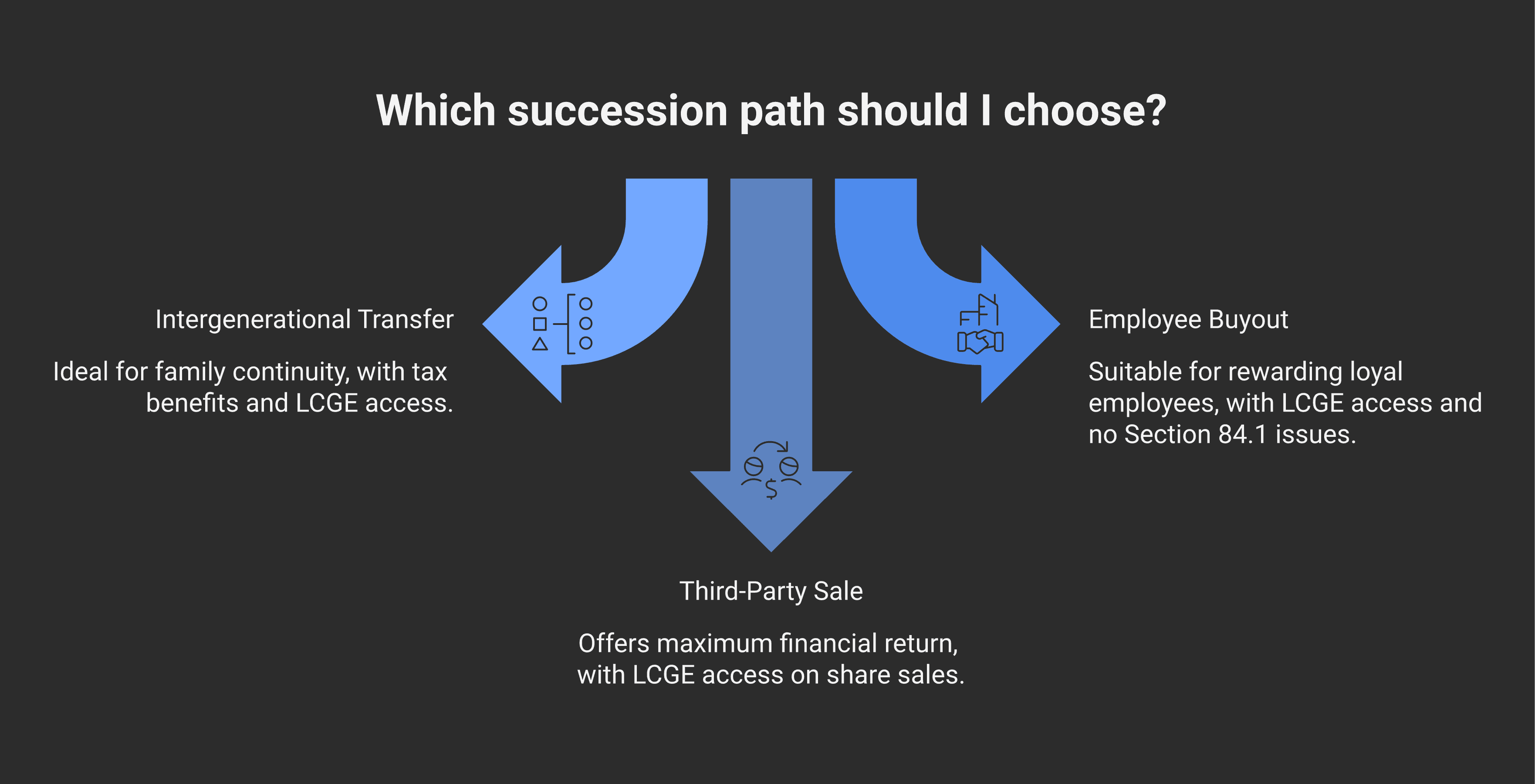

Three main succession paths: (1) intergenerational transfer to family, (2) employee/management buyout, and (3) third-party sale. Each has fundamentally different tax mechanics under the Income Tax Act.

The intergenerational business transfer exception to section 84.1 — originally introduced by Bill C-208 (2021) and amended by Bill C-59 effective January 1, 2024 — lets a parent sell QSBC shares to a corporation controlled by an adult child while still accessing the LCGE and capital gains treatment.

For 2026, the LCGE is $1,275,000 under section 110.6 of the Income Tax Act. At top combined provincial-plus-federal rates, this shelters approximately $341,000 of capital gains tax per individual.

LCGE multiplication via a family trust: a discretionary family trust holding QSBC shares can allocate gain on a sale to multiple Canadian-resident family members, each accessing their own LCGE — multiplying the total sheltered gain. See our family trusts post.

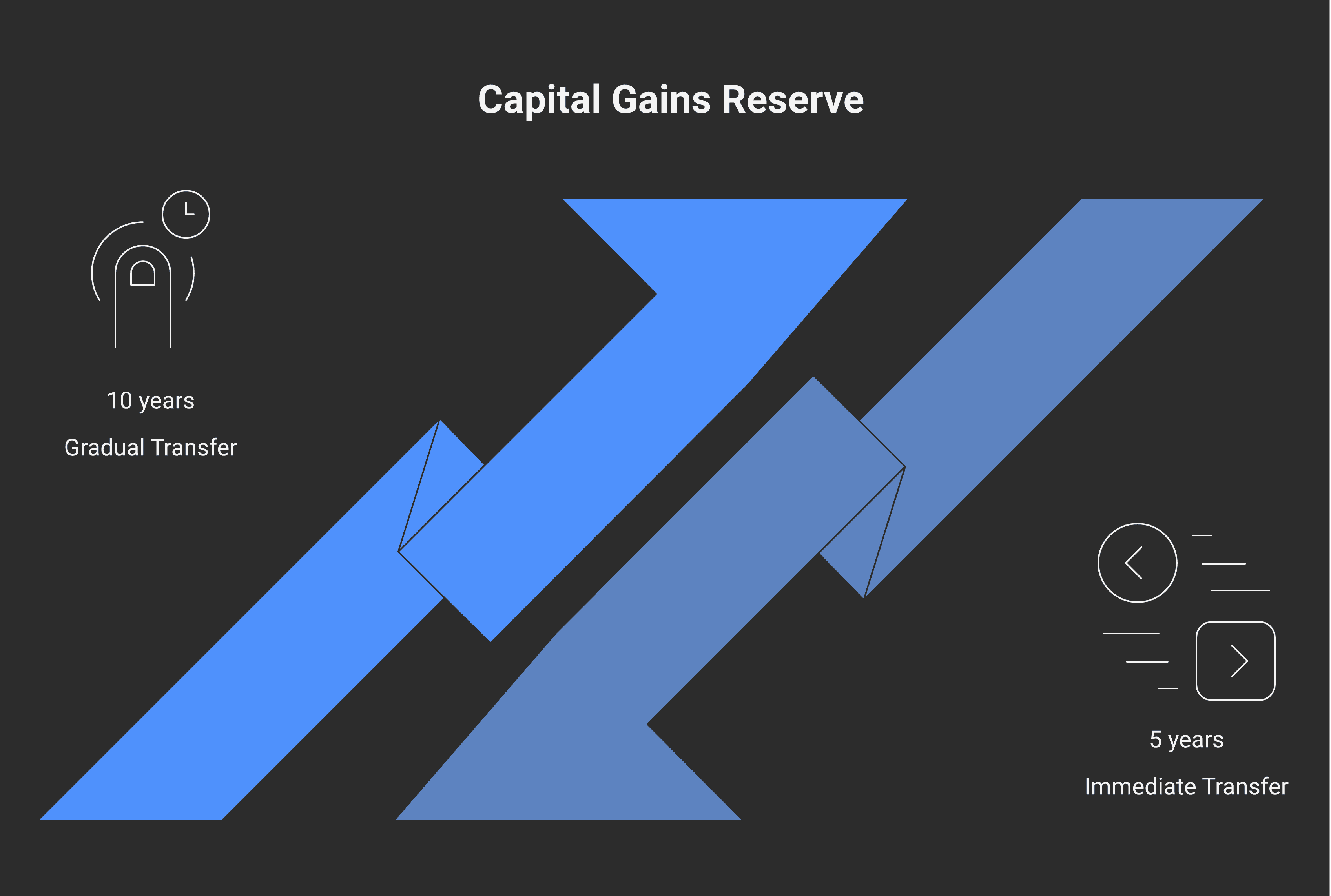

Two intergenerational transfer paths under Bill C-59 (effective Jan 1, 2024): an immediate transfer (3-year compliance window) or a gradual transfer (5-10 year window). The 2024 amendments are stricter on parent's surrender of control and child's active involvement than the original Bill C-208.

The three succession paths

Most Canadian business owners eventually exit through one of three structures, each with distinct tax mechanics:

Path 1: Intergenerational transfer to family. The owner sells their QSBC or family-farm/fishing-corporation (FFFC) shares to a corporation controlled by their adult child (or grandchild, or — since January 1, 2024 — adult niece/nephew or grandniece/grandnephew). Without the Bill C-208 / Bill C-59 carve-out, this would trigger section 84.1 of the Income Tax Act and recharacterise the disposition as a fully taxable dividend instead of a capital gain — eliminating LCGE access. The carve-out lets it qualify as a capital gain transaction.

Path 2: Employee or management buyout. The owner sells to a key employee or to a management team that purchases through a newly-incorporated holding company. Typically structured as an asset sale or share sale depending on the parties' tax positions. Owner can usually access the LCGE if the corporation qualifies as QSBC.

Path 3: Third-party sale. The owner sells to a strategic buyer or financial buyer (private equity, etc.). Tax mechanics depend on whether the deal is structured as an asset sale (buyer-favourable, seller absorbs taxes on the corporate-level gains) or share sale (seller-favourable, LCGE access).

Each path has different timing, valuation, and post-transaction control implications. The right answer depends on the owner's goals, the family situation, the business's marketability, and tax-optimisation considerations.

Section 84.1 — the rule that almost always bites

Without an exception, section 84.1 of the Income Tax Act prevents what tax practitioners call "surplus stripping" — converting what would be a taxable dividend into a more lightly-taxed capital gain by selling shares to a non-arm's-length corporation. The mechanic:

A shareholder sells shares of Corp A to Corp B (a corporation they or a related person controls)

Corp B's "paid-up capital" (PUC) on the shares received is reduced under section 84.1

The shareholder is deemed to have received a dividend equal to the excess of the proceeds over the lower of the original ACB and the (now-reduced) PUC

The practical effect: the shareholder gets a deemed dividend (taxed at full personal rates with dividend gross-up + DTC) instead of a capital gain (50% inclusion + LCGE access). The differential can be 20+ percentage points of total tax.

Section 84.1 was originally designed to block exactly the abuse it sounds like — a parent "selling" their company to their own holdco and accessing capital gains treatment. But it also catches genuine family business transfers, where a child legitimately buys the family business through their newly-incorporated holdco. Bill C-208 (2021) and Bill C-59 (2024) created the carve-out for genuine intergenerational transfers.

We cover the section 84.1 mechanics in detail in our dedicated post.

The intergenerational transfer carve-out — what changed

Bill C-208 (June 29, 2021) introduced the original carve-out: section 84.1 doesn't apply when the shares being transferred are QSBC or FFFC shares, the purchaser corporation is controlled by one or more of the vendor's adult children or grandchildren, and the purchaser corporation doesn't dispose of the shares within 60 months.

The original Bill C-208 was widely criticised by Finance as being too loose — it allowed taxpayers to access the carve-out with essentially no requirement that the transfer be genuine. Bill C-59 amendments effective January 1, 2024 tightened the rules into two structured paths.

Path A: Immediate intergenerational business transfer

A faster path with stricter timing requirements:

Condition | Requirement |

|---|---|

Parent's control surrender | Parent must give up legal control of the corporation immediately at the time of sale |

Parent's economic interest reduction | Within 36 months, parent must own no shares of the corporation other than non-voting preferred shares (i.e. fully divest their common-equity interest) |

Adult child's active involvement | Adult child must take active involvement in the business immediately |

Completion window | All conditions must be met within 3 years |

Capital gains reserve | Extended 10-year reserve available (same as the gradual path, under ITA 40(1.2) and 84.1(2.31)) |

Path B: Gradual intergenerational business transfer

A slower path with more flexibility on timing:

Condition | Requirement |

|---|---|

Parent's control surrender | Parent must give up legal control of the corporation within 36 months |

Parent's economic interest reduction | Parent must reduce economic interest to no more than 30% (preferred shares) within 10 years |

Adult child's active involvement | Adult child must take active involvement in the business within 60 months |

Completion window | Within 5 to 10 years |

Capital gains reserve | Extended 10-year reserve is available |

Eligible family members under Bill C-59 (effective Jan 1, 2024): adult children, grandchildren, AND adult nieces/nephews/grandnieces/grandnephews (newly added in 2024). The transferee corporation must be controlled by one or more of these eligible family members.

Joint liability. If CRA later determines that the transfer was not a genuine intergenerational business transfer, both the parent and the child(ren) are jointly liable for the additional tax that would have applied without the carve-out (i.e., section 84.1 dividend treatment instead of capital gains treatment).

LCGE multiplication via family trust

The Lifetime Capital Gains Exemption shelters up to $1,275,000 of capital gains on QSBC or FFFC dispositions per individual under section 110.6 of the Income Tax Act. For a single owner, that's roughly $341,000 of tax sheltered at top combined provincial-plus-federal rates.

A family trust holding QSBC shares can allocate the capital gain on a sale to multiple Canadian-resident family members (the trust's beneficiaries) — each of whom can access their own LCGE. The mechanic:

The owner-shareholder transfers QSBC shares to a family trust (typically via an estate freeze — see post 16 below)

The trust's beneficiaries are typically the owner's spouse, children, and possibly grandchildren and other relatives

On a future sale, the trust distributes the capital gain to multiple beneficiaries

Each beneficiary uses their own LCGE to shelter their allocated portion of the gain

A family trust with five Canadian-resident beneficiaries can theoretically shelter 5 × $1,275,000 = $6,375,000 of capital gains via LCGE multiplication. The Tax on Split Income (TOSI) rules under section 120.4 limit the practical scope (capital gains from QSBC sales generally remain TOSI-exempt for adult beneficiaries with sufficient excluded-share status, but pre-LCGE planning needs careful analysis). See our family trusts post for the trust mechanics.

Asset sale vs share sale

For non-family exits (employee buyout, third-party sale), the choice between asset sale and share sale is one of the largest deal-structuring decisions:

Asset sale (buyer's preference):

Buyer receives stepped-up cost base for purchased assets

Buyer can cherry-pick which liabilities to assume

Seller pays corporate-level tax on each asset's deemed gain

Seller can take after-tax proceeds out via dividend or capital dividend (using CDA from any capital gains)

LCGE generally not available (LCGE is for QSBC share sales, not asset sales)

Share sale (seller's preference):

Seller pays one layer of capital gains tax personally

Seller can access LCGE if shares qualify as QSBC

Buyer inherits all corporate liabilities (including unknown future ones)

Buyer cost base is the share purchase price — no asset-level step-up

Typically meaningful price discount to compensate buyer

We work through the asset-vs-share trade-off, including the section 22 election (asset-sale debt treatment), section 14/13/CECRA (eligible capital property), and the ETA section 167 election (GST/HST), in our asset sale vs share sale guide.

QSBC purification

For a share sale to qualify for the LCGE, the corporation must meet the qualified small business corporation (QSBC) test under section 110.6 of the Income Tax Act at the time of sale. The tests:

At the time of sale: the corporation is a CCPC and 90%+ of the FMV of its assets are used in an active business carried on primarily in Canada (or are shares/debt of a "connected" CCPC meeting the same test).

Throughout the 24 months before sale: the corporation was a CCPC and at least 50% of the FMV of its assets were used in an active business.

Throughout the 24 months before sale: the shares were owned by the seller (or related person).

The "90% active business assets" test at the time of sale and the "50% active business assets" test for 24 months prior are the most common QSBC qualification issues. Many CCPCs accumulate cash, marketable securities, or other passive assets over time, which can disqualify them from QSBC status when the time comes to sell.

Purification is the process of removing passive assets before sale to re-qualify the corporation. Common purification techniques include:

Paying out accumulated cash and investments as dividends to shareholders (depleting passive assets)

Transferring passive investments to a sister or holding corporation (separating active from passive)

Investing accumulated surplus into active business assets (operating equipment, inventory, etc.)

Purification typically requires a multi-year horizon — the 24-month asset test means the cleansing must be substantially complete two years before the planned sale.

Valuation considerations

Succession planning involves valuation at multiple points:

The sale price itself — the consideration the buyer pays

The cost base for capital gains calculation — typically the seller's original investment plus any subsequent capital additions

The QSBC valuation — the FMV of the shares being sold (drives the 90% active-business-asset test)

The family-trust valuation — when the trust acquired the shares (drives the trust's cost base)

For sales to family members or to corporations controlled by related persons, the transaction must occur at FMV under section 69 of the Income Tax Act. Selling at less than FMV doesn't reduce the deemed proceeds for tax purposes — the seller still pays tax based on FMV — but the buyer doesn't get a stepped-up cost base for the excess.

A professional business valuation is typically required for any sale to a non-arm's-length party. The valuation report becomes the documentation for tax filings and is what CRA reviews if the transaction is audited.

Common timeline

A typical Canadian business succession plan spans 5-10 years before the planned exit:

T-7 to T-5 years: Initial assessment — owner's goals, family situation, business marketability, current value, target exit value. Open conversation with successor candidates (if family or employee).

T-5 to T-3 years: Structural setup. Estate freeze (if not yet done) to cap owner's value at current FMV. Family trust establishment (if multi-beneficiary LCGE planning). QSBC purification begins (removing passive assets to qualify the corporation).

T-3 to T-1 years: Implementation. Continue purification. Establish key successor in business operations. Begin negotiating sale terms (price, structure, timing).

T-0 (Sale year): Transaction closes. LCGE claims made on individual tax returns. Capital gains reserve elected if proceeds spread over multiple years. Bill C-59 conditions begin to be tracked for intergenerational transfers.

T+1 to T+10 years: Ongoing compliance with intergenerational transfer conditions (control surrender, economic interest reduction, child's active involvement). Capital gains reserve recognition over the reserve period.

The single biggest planning mistake we see is starting too late. A business sale 12 months out leaves no time for QSBC purification, no time to establish a family trust if one isn't already in place, and no flexibility on Bill C-59 path selection. The five-year horizon is realistic; the ten-year horizon is ideal.

For Modern Axis client engagements on owner-manager succession, the analysis typically starts with a strategic review of the three paths against the owner's goals, then proceeds to implementation work — estate freeze, family trust setup, QSBC purification, and pre-sale due diligence.

Frequently asked questions

What is business succession planning in Canada?

Business succession planning is the tax-and-legal process of transferring ownership and control of a Canadian business to the next set of owners — typically family members, employees, or a third-party buyer. The Canadian tax system imposes meaningful constraints on each path under sections 84.1, 110.6, and 245 of the Income Tax Act. The 2021 Bill C-208 and 2024 Bill C-59 reforms reshaped the intergenerational-transfer path; the LCGE indexation has increased the tax shelter on QSBC sales; and the asset-vs-share-sale dynamics continue to drive third-party sale structuring.

What is the lifetime capital gains exemption for 2026?

The LCGE for 2026 is $1,275,000 under section 110.6 of the Income Tax Act, indexed from the $1.25M established by Budget 2024 effective June 25, 2024. The LCGE applies to qualifying small business corporation (QSBC) shares and qualifying farm and fishing property (QFFP). At top combined federal-plus-provincial rates, the full LCGE shelters approximately $341,000 of capital gains tax per individual.

What is the intergenerational business transfer exception?

The intergenerational business transfer (IBT) exception to section 84.1 of the Income Tax Act allows a parent to sell QSBC or FFFC shares to a corporation controlled by their adult child (grandchild, niece/nephew, or grandniece/grandnephew under post-2024 rules) while still accessing capital gains treatment and the LCGE — instead of having section 84.1 recharacterise the disposition as a fully taxable dividend. Originally introduced by Bill C-208 (June 29, 2021), the exception was tightened by Bill C-59 effective January 1, 2024 into two structured paths: an Immediate Transfer (3-year window) and a Gradual Transfer (5-10 year window).

What's the difference between the immediate and gradual transfer paths under Bill C-59?

The Immediate Transfer path has stricter timing — parent must give up legal control at the time of sale, fully divest its common-equity interest (own only non-voting preferred shares) within 36 months, and the child must be actively involved immediately. All conditions must be met within 3 years; standard 5-year capital gains reserve applies. The Gradual Transfer path allows control to transfer within 36 months, economic interest reduction to ≤30% within 10 years, and child's active involvement within 60 months. The Gradual path also has access to the extended 10-year capital gains reserve.

How can a family trust multiply the LCGE?

A discretionary family trust holding QSBC shares can allocate the capital gain on a future sale to multiple Canadian-resident beneficiaries (typically the owner's spouse, adult children, and grandchildren). Each beneficiary uses their own LCGE to shelter their allocated portion of the gain. A trust with five Canadian-resident beneficiaries can theoretically shelter 5 × $1,275,000 = $6,375,000 of capital gains. The Tax on Split Income (TOSI) rules under section 120.4 of the Income Tax Act apply complex constraints — most QSBC capital gains for adult beneficiaries with excluded-share status remain exempt, but the analysis requires careful pre-sale planning.

What is QSBC purification?

QSBC purification is the process of removing passive assets from a corporation so it meets the qualified small business corporation tests under section 110.6 of the Income Tax Act at the time of sale (90% active business assets in Canada) and throughout the 24 months before sale (50% threshold). Common techniques include paying out accumulated cash and investments as dividends, transferring passive assets to a sister/holding corporation, and investing accumulated surplus into active business assets. Purification typically requires a multi-year horizon because of the 24-month asset test.

How long should I plan for business succession?

A typical Canadian business succession plan spans 5-10 years before the planned exit. The most common planning mistake is starting too late — a 12-month timeline leaves no time for QSBC purification, family trust establishment, or Bill C-59 path selection. The five-year horizon is realistic; the ten-year horizon is ideal. Family-transfer planning especially benefits from time to coordinate the parent's control transition and the child's active involvement requirements under Bill C-59.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA