Asset Sale vs Share Sale: Selling a Canadian Business

The single biggest deal-structuring choice in selling a Canadian business is whether the transaction is structured as an asset sale or a share sale. Buyers strongly prefer asset sales; sellers strongly prefer share sales. The negotiation typically lands somewhere in the middle, with the parties trading the structural advantage against price, holdback, indemnity terms, and other deal mechanics.

The tax differential is large. A vendor selling QSBC shares can shelter up to $1,275,000 of capital gains with the LCGE in 2026; the same vendor selling assets generally cannot. A buyer purchasing assets gets a stepped-up cost base for depreciation; a share purchaser inherits the existing low ACB. For a $5M deal, the after-tax differential between the two structures can be $300K-$500K — and the entire negotiation often turns on who absorbs that.

This guide walks through the two structures, the tax mechanics on each side, the typical hybrid solutions, and the elections (section 22, ETA section 167, etc.) that smooth the rough edges.

Key takeaways

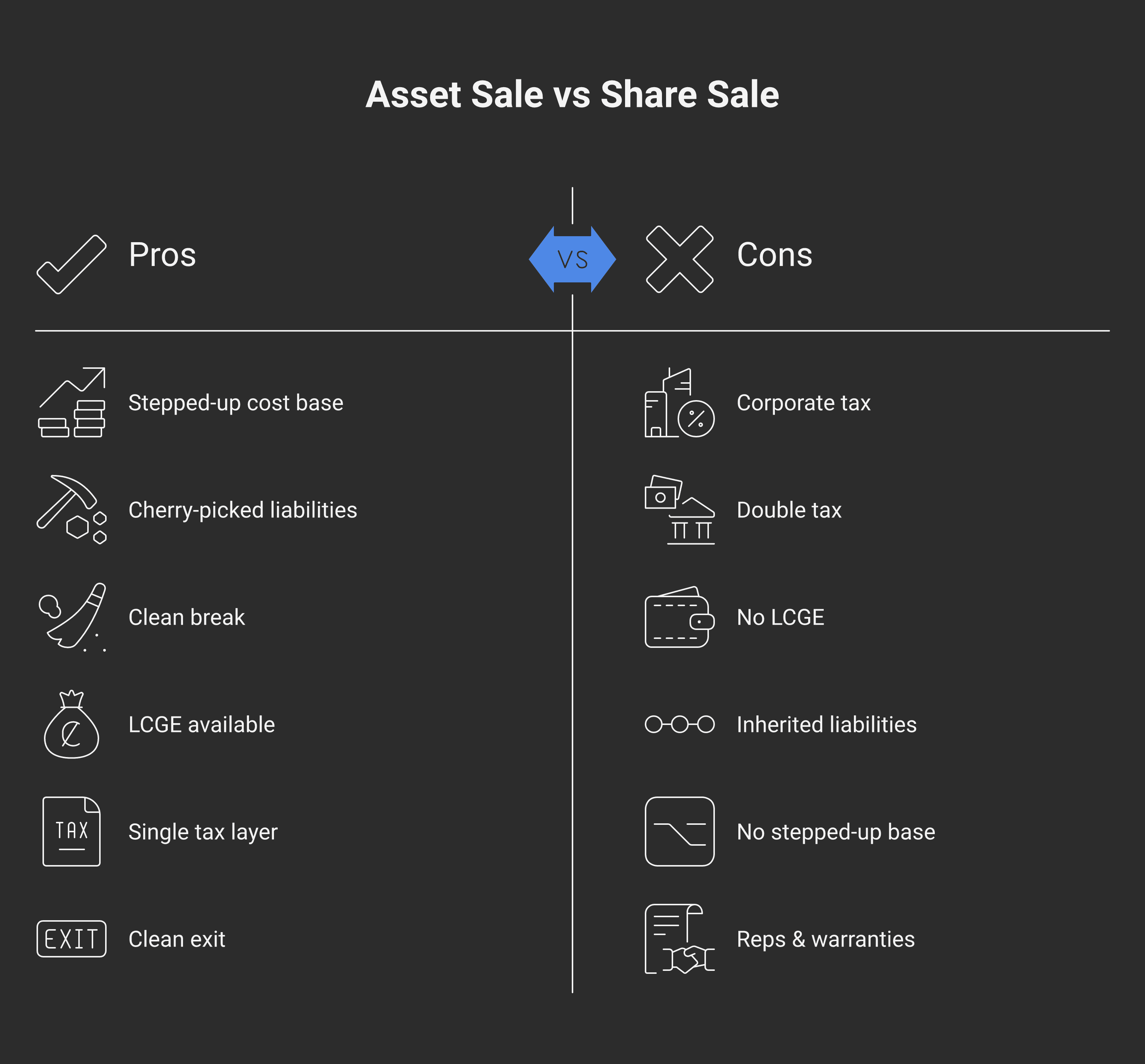

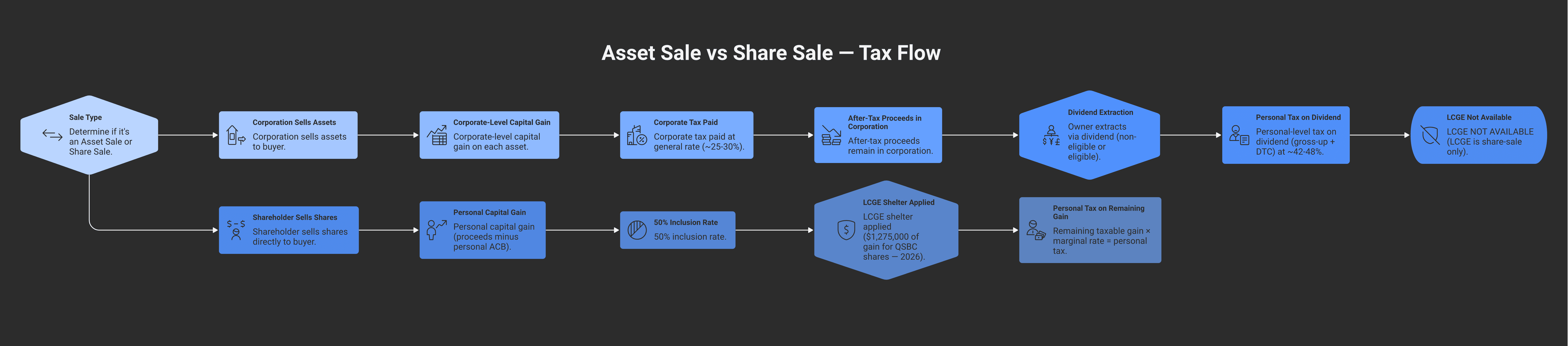

Asset sale (buyer's preference): the corporation sells its assets to the buyer; the corporation pays corporate-level tax on each asset's gain; the seller then extracts after-tax proceeds via dividend or capital dividend. Buyer gets stepped-up cost base for depreciation. LCGE generally not available to the seller (LCGE is for QSBC share sales).

Share sale (seller's preference): the seller sells corporate shares directly to the buyer (or to a buyer's holding corporation). Seller pays one layer of capital gains tax personally and can access the LCGE if shares qualify as QSBC under section 110.6 of the Income Tax Act. Buyer inherits all corporate liabilities — including unknown future ones.

Hybrid structures are common: a section 22 election lets accounts receivable transfer as asset-sale; the parties negotiate which assets, which liabilities, and which structures apply by category. For deals over $1M-$2M, hybrid is the norm rather than the exception.

The GST/HST election under section 167 of the Excise Tax Act lets the sale of all (or substantially all) of a business's assets transfer GST/HST-free if both parties are registrants — avoiding the cash flow drag of seller collecting and buyer recovering GST/HST on millions of dollars of asset value.

Reps & warranties insurance has become common in mid-market Canadian deals as a way to bridge buyer's risk concerns on share sales — letting sellers preserve LCGE access without taking on multi-year indemnity exposure.

Why buyers prefer asset sales

From the buyer's perspective:

1. Stepped-up cost base for assets purchased. The buyer pays $X for asset Y; the buyer's cost base for asset Y is $X. Depreciable assets (equipment, vehicles, building improvements) can be depreciated against future income at full cost. In contrast, a share purchaser inherits the corporation's pre-existing low ACB on the same assets and can only depreciate against that lower base.

2. Cherry-pick liabilities. The buyer chooses which liabilities to assume. Unknown liabilities (lawsuits being prepared, undisclosed warranty claims, environmental issues, tax reassessments for prior years) generally stay with the seller's corporation.

3. Cherry-pick assets. The buyer purchases only the assets it wants — leaving behind assets it doesn't (obsolete inventory, marginal product lines, unused real estate).

4. Clean break from corporate history. No multi-year tax reassessment risk hanging over the buyer (assuming the seller's corporation continues to exist post-sale to absorb its own historical exposure).

5. Simpler customer/supplier contracts. Contracts typically need to be reassigned regardless, but asset sale allows the buyer to renegotiate terms with key parties.

Why sellers prefer share sales

From the seller's perspective:

1. Lifetime Capital Gains Exemption (LCGE). Under section 110.6 of the Income Tax Act, QSBC share sale gains up to $1,275,000 per individual (2026) are exempt from capital gains tax. At top combined federal-plus-provincial rates, that shelters approximately $341,000 of tax per individual. LCGE is not available on asset sales.

2. Single layer of tax. A share sale by the seller is a single capital gains event — 50% inclusion at the seller's marginal rate. An asset sale triggers corporate-level tax on each asset's gain, then a second layer when the seller extracts after-tax proceeds via dividend.

3. Clean exit. All corporate liabilities transfer to the buyer (or the buyer's holdco). The seller does not retain a non-active corporation full of legacy issues.

4. Speed. A share sale closes more cleanly because the corporation continues operating under new ownership — no need to transfer contracts, leases, licences, employees, or assets individually.

5. Higher buyer-side cost in many provinces. Many provinces impose a higher PTT or other transfer tax on real estate transfers; in a share sale, the real estate stays inside the corporation and doesn't trigger the transfer tax.

The math — why the differential is so large

A simplified illustration of the structural tax differential, using a generic Ontario CCPC example (all rates are 2026 estimates, framework-level only):

Hypothetical scenario: A CCPC has assets with FMV $5M, an ACB of $1M (so $4M of corporate-level gain on asset sale), and the owner has ACB of $100K in the shares. Owner is in the top Ontario bracket.

Asset sale outcome (corp pays first, then owner extracts):

Corporate gain $4M; corporate tax at general rate ~26.5% = $1.06M

After-tax corporate proceeds = $5M − $1.06M = $3.94M (less the original $1M cost base, which is also extractable but doesn't add to gain)

Owner extracts $3.94M post-corporate-tax as dividend → personal tax ~47% non-eligible = ~$1.85M

Net after-tax to owner ≈ $2.09M (out of $5M FMV)

Share sale outcome (LCGE access):

Personal capital gain $4.9M ($5M − $100K personal ACB)

LCGE shelter: $1.275M (50% taxable = $637,500 sheltered against personal tax)

Remaining taxable gain after LCGE: $3.625M × 50% inclusion × ~53.5% top combined rate = ~$970K of tax

Net after-tax to owner ≈ $4.03M (out of $5M FMV)

Share sale advantage: roughly $1.9M of additional after-tax proceeds on this hypothetical. Even with a price discount the buyer typically demands in a share sale, the differential is large enough that share sale is dramatically preferred from the seller's side.

(Note: this is a simplified framework illustration. Actual outcomes depend on multiple factors — purification status, family-trust availability for LCGE multiplication, capital gains reserves, capital dividend account balance, depreciation recapture on asset sale, GST/HST treatment, real-estate transfer taxes, etc. Run with a qualified advisor before any decision.)

Hybrid structures and key elections

Real-world deals over $1M-$2M are almost never pure asset or share sales. A typical hybrid structure:

Section 22 election (eligible capital property and AR). Where the seller has accounts receivable, the section 22 election under the Income Tax Act lets the AR transfer as an asset-sale element while the rest of the deal is a share sale. The buyer gets the deduction when the AR is collected; the seller recognises the AR as ordinary income at the time of sale.

Section 167 GST/HST election (ETA). Under section 167 of the Excise Tax Act, an asset sale of all or substantially all of a business's assets transfers GST/HST-free if both parties are registrants and the election is filed. This avoids the buyer needing to pay millions of dollars of GST/HST upfront (refunded later via ITC) — a meaningful cash flow improvement on large deals.

Section 85 rollover. A section 85 rollover can be used pre-sale to transfer assets between the seller's corporation and a new acquirer or to spin off non-active assets pre-share-sale (the latter helps with QSBC purification).

Section 14 / depreciable property mechanics. When eligible capital property is sold (formerly section 14, now mostly under sections 13 and 38), the seller has recapture or terminal loss issues. The buyer claims new CCA starting from the purchased value.

Hybrid mechanic — share sale to buyer's holdco, then asset sale to operating sub. Common in mid-market deals: the buyer acquires the target's shares via a new holdco, then on closing day the target's assets are sold (intercompany) to the buyer's operating company. This allows LCGE access for the seller and asset-sale tax treatment for the buyer's operating company (via the new ACB-bumped acquisition).

The reps & warranties trade-off

In a share sale, the buyer inherits all corporate liabilities — including future tax reassessments for pre-closing periods, unknown environmental issues, undisclosed lawsuits, etc. The buyer protects itself via:

Reps & warranties from the seller. The seller makes representations that no undisclosed issues exist; if a rep is breached, the buyer claims damages.

Indemnification cap and period. Typically 10-25% of deal value, 12-36 months indemnity period.

Holdback / escrow. A portion of the purchase price held back to satisfy potential indemnity claims.

Reps & warranties insurance. A third-party insurer underwrites the rep & warranty exposure, allowing the seller to walk away cleanly. Premium typically 2-4% of insured limit; deductible 0.5-1% of deal value. Common in mid-market Canadian deals.

The reps & warranties insurance market in Canada has matured significantly. For a $5M-$50M deal, R&W insurance has become close to standard — letting sellers preserve LCGE and clean-exit benefits without taking on multi-year personal indemnity exposure.

Working capital and earn-outs

Two adjustment mechanisms that affect both structures:

Working capital adjustment. The deal price is calibrated based on a "normalized" working capital level (cash, AR, inventory, less AP). At closing, working capital is measured against the normalized level — excess or shortfall adjusts the purchase price.

Earn-outs. A portion of the purchase price contingent on future business performance (revenue, EBITDA, customer retention, etc.) over 1-3 years post-close. Earn-out payments are typically taxed as additional capital gains to the seller (subject to specific contract terms) — but a poorly-drafted earn-out can be recharacterised as ordinary income.

Practical timeline

A typical share-sale (or hybrid) closing follows a multi-month timeline:

Pre-closing (T-3 to T-6 months):

QSBC purification audit and adjustments

Family trust review (if any) for LCGE multiplication

Reps & warranties drafting

Buyer due diligence

Tax opinion preparation

Closing (T-0):

Share purchase agreement signed

Purchase price paid (less holdback/escrow)

Section 167 GST/HST election filed (if applicable)

Section 22 election filed (if applicable)

Section 85 rollover documentation finalised (if pre-closing freeze used)

Post-closing (T+1 to T+36 months):

Indemnity period runs (typically 12-24 months for general reps; 36-72 months for tax reps)

Earn-out periods run (if any)

Capital gains reserve elected by seller if proceeds spread over multiple years

R&W insurance claim period (if policy in place)

For Modern Axis client engagements on business sales, the structuring conversation typically begins 6-12 months before closing — covering the asset-vs-share decision, the hybrid structures and key elections, and the QSBC purification status. The cost of getting it right is small relative to the after-tax differential.

Frequently asked questions

What is the difference between an asset sale and a share sale in Canada?

An asset sale is when the corporation sells its assets to the buyer — the corporation continues to exist (typically winding up post-sale), pays corporate tax on each asset's gain, and the seller extracts after-tax proceeds via dividend. A share sale is when the shareholder sells the shares of the corporation directly to the buyer — the corporation continues with new ownership, the seller pays one layer of capital gains tax personally, and the buyer inherits all corporate liabilities. Buyers strongly prefer asset sales; sellers strongly prefer share sales because of LCGE access and the single layer of tax.

Can I claim the Lifetime Capital Gains Exemption on an asset sale?

Generally no. The LCGE under section 110.6 of the Income Tax Act applies specifically to dispositions of qualified small business corporation (QSBC) shares and qualifying farm/fishing property (QFFP). An asset sale by the corporation doesn't qualify — the gain is realized at the corporate level. There are limited indirect routes via post-asset-sale share dispositions, but the LCGE access is fundamentally tied to share sales.

What is a hybrid sale structure?

A hybrid sale combines elements of both asset and share sales. The most common version: the buyer acquires the seller's corporate shares (share sale, LCGE available to seller), then immediately on closing the target corporation's assets are sold (intercompany) to the buyer's newly-incorporated operating company. The seller gets capital gains treatment with LCGE; the buyer's operating company gets stepped-up cost base for asset depreciation. Section 22 (accounts receivable), Section 14 (depreciable property), and section 85 (rollover) elections smooth the asset-side mechanics.

What is the section 167 GST/HST election?

The election under section 167 of the Excise Tax Act lets the sale of all or substantially all of a business's assets transfer GST/HST-free between two GST/HST registrants. Without the election, the seller would charge GST/HST on the asset sale, the buyer would pay it upfront, and the buyer would recover it later via Input Tax Credit. The election avoids this cash flow drag. The election is filed on Form GST44 and must be joint between the parties.

What are reps and warranties insurance and why do sellers use it?

Reps & warranties insurance is a third-party insurance policy that underwrites the seller's contractual representations about the business at the time of sale. If a rep is breached, the buyer claims against the insurer rather than the seller. The premium is typically 2-4% of the insured limit, with a deductible of 0.5-1% of deal value. R&W insurance lets the seller walk away cleanly without multi-year indemnity exposure, while still giving the buyer protection. It has become close to standard for Canadian mid-market deals ($5M-$50M).

How does the working capital adjustment work?

The purchase price is calibrated based on a "normalized" working capital level (cash + AR + inventory − AP). At closing, actual working capital is measured against the normalized level — excess (the business has more working capital than normalized) is added to the purchase price; shortfall is subtracted. The adjustment is usually capped (e.g., ±$100K of normalized) to prevent disputes over small differences. Working capital adjustment language is one of the most contested provisions in deal documents.

What is an earn-out and how is it taxed?

An earn-out is a portion of the purchase price contingent on future business performance (revenue, EBITDA, customer retention, etc.) over a 1-3 year post-closing period. Earn-out payments to the seller are typically taxed as additional capital gains under the original sale's structure — but the contract drafting matters. A poorly-drafted earn-out tied to the seller's continued employment can be recharacterised as employment income (taxed at the seller's full ordinary rate). The structure and documentation need careful review at deal closing.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA