2024 AMT Reform Canada: Who Actually Pays the Higher AMT Now

The Alternative Minimum Tax has been on Canada's books since 1986. For most of those years it caught a relatively narrow group — taxpayers with very large capital gains, oversized donation strategies, or aggressive use of certain deductions. The 2024 reform changed that. Starting with the 2024 tax year, the AMT rate is higher, the base is broader, and the donation tax credit is halved for AMT purposes — a change that pushed a meaningful number of high-income philanthropic households over the AMT line for the first time. By the 2025 filing season (the first one fully under the new rules), reviewing AMT exposure has become a year-of-event obligation for almost every high-income return.

Key takeaways

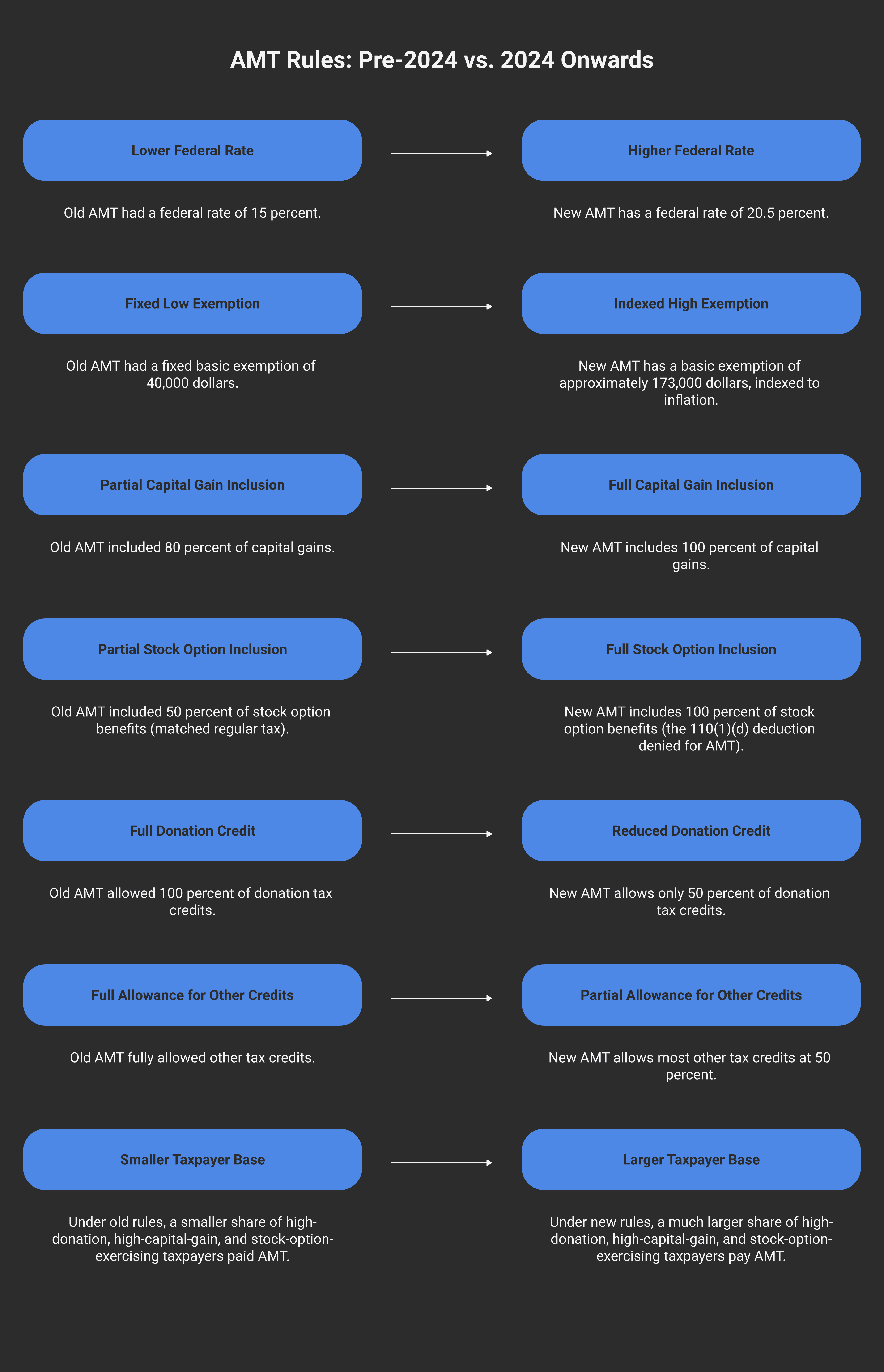

The 2024 AMT reform raised the federal rate from 15% to 20.5% and raised the basic exemption from $40,000 to approximately $173,000, indexed to the bottom of the fourth federal bracket.

Capital gains are now included at 100% for AMT (vs 50% regular), stock option benefits at 100% (vs 50% via paragraph 110(1)(d)), and 80% of the donation tax credit applies.

AMT is the greater of regular tax and the AMT calculation — any excess becomes a carry-forward against regular tax in the next seven years, but only if future regular tax exceeds future AMT.

The three events most likely to trigger AMT under the new rules are a large capital gain (especially LCGE-claimed QSBC sales), a large in-kind donation of appreciated securities, and a stock option exercise with a significant taxable benefit.

This post is about what changed, who actually pays AMT now, the mechanics of the federal AMT calculation under section 127.5 of the Income Tax Act, and the three main events that trigger it — large capital gains, large donations of publicly traded securities, and stock option exercises.

The rule, in one sentence

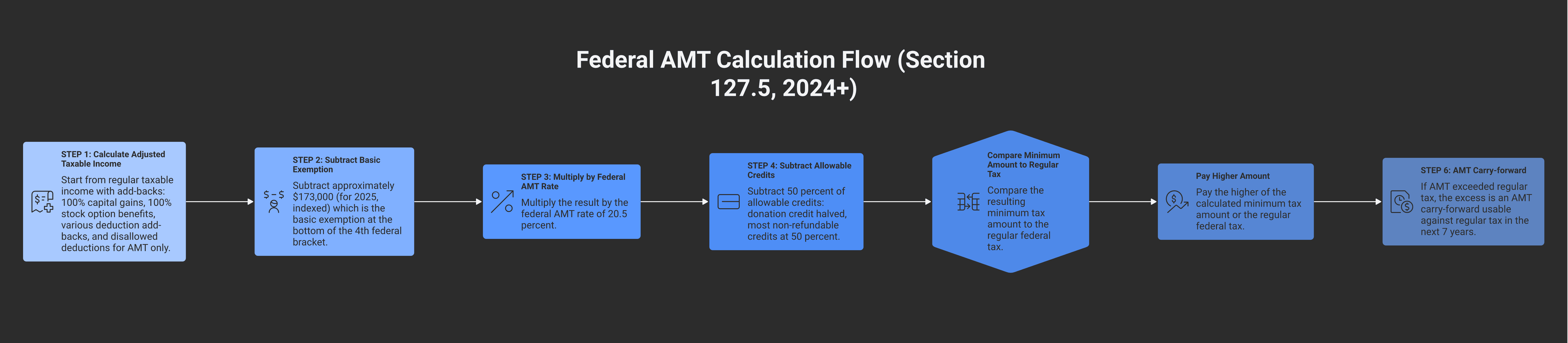

Under section 127.5 of the Income Tax Act, every individual taxpayer in Canada calculates regular federal tax and a parallel "minimum amount" — federal AMT at 20.5% × (Adjusted Taxable Income − the basic exemption) less 50% of most personal credits — and pays the higher of the two; the AMT was rewritten effective the 2024 tax year to broaden the adjusted-taxable-income base (100% capital gain inclusion, 80% of the donation tax credit allowed, full stock option benefit) in exchange for a higher exemption ($173K vs the prior $40K).

The shift in the donation rule is the change most often missed. Pre-2024, the full donation credit applied for AMT. Post-2024, only 80% applies — meaning a high-income individual making a $500,000 donation can trigger AMT despite the donation credit zeroing out the regular tax. The shape of the trap is exactly that.

How AMT actually works — the simplified calculation

The 2024 federal AMT calculation, schematically:

Start with regular taxable income

Add back AMT-only inclusions:

100% of capital gains (vs the 50% included in regular taxable income → add back the other 50%)

100% of stock option benefits (vs the 50% paragraph 110(1)(d) deduction → denied for AMT)

Limited-partnership losses, employee home relocation, northern residents, certain interest expense

Subtract the basic exemption — approximately $173,000 (indexed annually; tied to the bottom of the fourth federal bracket)

Multiply by 20.5% — the federal AMT rate

Subtract 50% of most non-refundable credits — donation credit allowed at 80%, dividend tax credit fully disallowed, most personal credits at 50%

Result is the federal "minimum amount"

Pay the greater of regular federal tax and the minimum amount

Provinces with their own AMT (notably Ontario) calculate their AMT on top of this; British Columbia and several other provinces don't have a stand-alone provincial AMT but apply provincial rates to the AMT base by extension.

What changed — old vs new AMT side by side

The narrative reasons for each shift:

Higher rate (20.5% vs 15%) reflects an intent to materially close the gap between AMT and the regular-tax marginal rates the system was designed to backstop.

Higher exemption ($173K vs $40K) removes most middle-bracket taxpayers from AMT entirely — the new rules aim more squarely at high earners.

100% capital gain inclusion closes the gap with the regular tax base; if the regular capital-gain inclusion ever rises (the saga around the 2024 capital gains rate change), the AMT base already reflects the higher inclusion.

The donation credit haircut (only 80% of the credit is allowed for AMT) is a deliberate limit on the tax-efficiency of large donations, especially those funded with appreciated publicly traded securities under section 38(a.1) (which zeros out the capital gain on donated public securities for regular tax — but the gain is still included at 30% for AMT, and the credit is allowed at 80%).

100% stock option benefit inclusion treats the option benefit as ordinary employment income for AMT, denying the paragraph 110(1)(d) 50% deduction that softens the regular-tax hit.

Who pays AMT now — three event clusters

The new AMT rules can be summarised by who they catch:

Event 1: Large capital gains, especially LCGE-claiming sales

The single most common AMT trigger under the new rules is a sale of qualified small business corporation shares claiming the Lifetime Capital Gains Exemption. The LCGE reduces or eliminates the capital gain for regular tax. For AMT, however:

The full capital gain (not the 50% taxable portion) flows to Adjusted Taxable Income

The LCGE deduction is significantly restricted in the AMT calculation

The result is that a major QSBC sale at the LCGE limit can generate substantial AMT even when regular tax is near zero

The same structure catches:

Real estate sales where the principal residence exemption is being claimed

Large investment portfolio rebalancing

Estate planning gains realised on a deemed disposition at death

The mechanic: even if regular tax on the gain is small, AMT on the gross-up can be material — and the AMT carry-forward only helps if the next 7 years have high regular tax (which retirees and estates often don't).

Event 2: Large donations, especially of appreciated public securities

Under section 38(a.1), donating publicly traded securities in-kind to a registered charity produces a zero capital gain inclusion for regular tax purposes (the gain is treated as 0%, not the normal 50%). Combined with the full donation tax credit at the top marginal rate, this has long been one of the cleanest philanthropic strategies in Canada.

The 2024 AMT changes hit this strategy directly:

The capital gain on the donated security is included at 30% for AMT (the zero-inclusion under paragraph 38(a.1) is overridden to a 30% inclusion for AMT purposes)

The donation tax credit is only 50% allowed for AMT

The combination can push the donor over the AMT line even when regular tax is reduced to nearly zero by the donation credit

A $1 million in-kind donation of appreciated securities now requires year-of-event AMT modelling. The trap is most acute for one-time large donations (estate-related, business sale-related); regular smaller-scale donors are usually below the threshold.

Event 3: Stock option exercises

For employees of public companies (and certain employees of CCPCs after the 2020 stock option changes), exercising stock options generates an employment benefit equal to the FMV at exercise minus the exercise price. Paragraph 110(1)(d) of the Act allows a 50% deduction from that benefit for regular tax — effectively giving the option exercise capital-gain-like treatment.

The 2024 AMT reform denies the paragraph 110(1)(d) deduction for AMT purposes. The result:

For regular tax: 50% of the option benefit is taxable

For AMT: 100% of the option benefit is in the Adjusted Taxable Income base

The personal-tax rate the employee pays on a large option exercise can effectively rise from the regular blended rate (~26-27% on the deductible portion at the top BC bracket) to the AMT rate (~20.5% federal + provincial on the 100% inclusion)

The intent is to bring stock option exercises closer to ordinary-income tax treatment for AMT. Year-of-exercise planning — vesting timing, partial exercises, sell-to-cover sequences — becomes a real AMT lever.

The AMT carry-forward

AMT paid in a year is not simply lost. The excess of AMT over regular tax becomes an AMT carry-forward under section 120.2(3), usable against regular tax in any of the next seven taxation years — but only to the extent that regular tax in the future year exceeds AMT in that future year.

In other words: AMT is essentially a timing tax, not a permanent tax, provided the taxpayer has sufficient future regular tax to absorb the carry-forward. In practice:

For working-age taxpayers with continuing high income, the carry-forward usually gets used up within a few years — AMT functions as a deferral, not a true extra tax

For retirees, estates, and one-time-event taxpayers whose future income is materially lower, the carry-forward may expire unused — AMT becomes a permanent extra tax

For estates triggering AMT on a deemed disposition at death, the carry-forward dies with the taxpayer (cannot transfer to beneficiaries)

The retiree/estate scenario is where the AMT reform causes the most real cost: the carry-forward mechanism that softens the blow for working-age earners doesn't help someone whose future regular tax is going to be small.

Planning around the new AMT

Year-of-event modelling is now standard for any high-income return with one of the three trigger events. Specific levers:

Spread events across years. A $2 million capital gain split across two tax years often produces lower combined AMT than the same gain in one year, because the basic exemption applies each year.

Time donations to match high-income years. Donations in years with substantial regular tax absorb their credits efficiently. Donations in low-income years (post-retirement, sabbatical) may trigger AMT.

Stage option exercises. A large stock option grant exercised in tranches over several years often produces lower combined AMT than a single-year exercise.

Use the AMT carry-forward strategically. Concentrating regular-tax income in years following an AMT event can absorb the carry-forward before it expires.

Reconsider donation timing for one-time large gifts. A planned-giving structure (charitable remainder trust, donor-advised fund) may smooth the credit across multiple years more efficiently than a single-year donation under the new rules.

These decisions hinge on multi-year tax modelling. They are not back-of-envelope calculations under the new rules.

When AMT modelling lands on Modern Axis

Modern Axis CPA runs AMT projections as part of any planning engagement involving a likely trigger event — a planned business sale claiming the LCGE, a one-time large charitable gift, a stock option exercise, or any major capital realisation. The Tax Planning & Compliance service covers the annual review; multi-year AMT modelling for one-time events is its own scoped engagement. For US persons in Canada, AMT interacts with the foreign tax credit calculation in non-trivial ways — running US tax and Canadian AMT together is the only way to know the true net cost.

Frequently asked questions

What changed with the 2024 AMT reform in Canada?

The federal AMT rate rose from 15% to 20.5%. The basic exemption rose from $40,000 to approximately $173,000 (indexed to the bottom of the fourth federal bracket). The AMT base broadened to include 100% of capital gains (vs 50% regular), 100% of stock option benefits (vs the 50% paragraph 110(1)(d) deduction), and 80% of the donation tax credit (vs the full credit pre-reform). The intent was to focus AMT more squarely on high-income taxpayers using credit-driven strategies.

Who actually pays the new AMT?

Mainly three groups: high-income individuals with large capital gains (especially QSBC sales claiming the Lifetime Capital Gains Exemption), high-income philanthropic donors making large gifts of appreciated publicly traded securities, and employees exercising stock options with significant taxable benefits. Middle-income taxpayers are largely below the new ~$173K threshold and rarely trigger AMT. The reform was deliberately calibrated to land on top-bracket, event-driven taxpayers.

Is AMT permanent or recoverable in future years?

It depends. For taxpayers with sustained high regular-tax income, the excess of AMT over regular tax becomes a carry-forward applied against regular tax in the next seven years. For retirees, estates, and one-time-event taxpayers whose future regular tax is materially smaller, the carry-forward may expire unused, making AMT a permanent extra tax. Modelling future income before the triggering event is critical for knowing which group you're in.

How does the 2024 AMT affect charitable donations?

80% of the donation tax credit is allowed for AMT purposes — the full credit still applies for regular tax. The practical effect: a large in-kind donation of appreciated publicly traded securities (which under paragraph 38(a.1) has zero capital gain for regular tax) can still trigger AMT because the gain is included at 30% for AMT and the credit that would otherwise wipe out the tax is allowed at only 80%. Donors should model AMT before pledging.

Does AMT apply to corporations in Canada?

No. AMT applies only to individuals — including individuals filing as sole proprietors, trustees, and certain trusts under specific conditions. Corporations are not subject to AMT in Canada. Owner-managers concerned about AMT need only model it on the personal side, though it can flow through if a corporation distributes a triggering item (capital gain, stock option benefit) to the individual via a dividend or share sale.

How does AMT interact with the Lifetime Capital Gains Exemption?

The LCGE deduction is significantly restricted for AMT purposes. A QSBC sale claiming the full LCGE generates very little or no regular tax — but for AMT, the full capital gain flows to Adjusted Taxable Income with limited LCGE relief, and the AMT bill can be substantial. Sellers planning a QSBC exit should model AMT alongside regular tax before the sale, ideally early enough to consider spreading the disposition or accelerating other deductions.